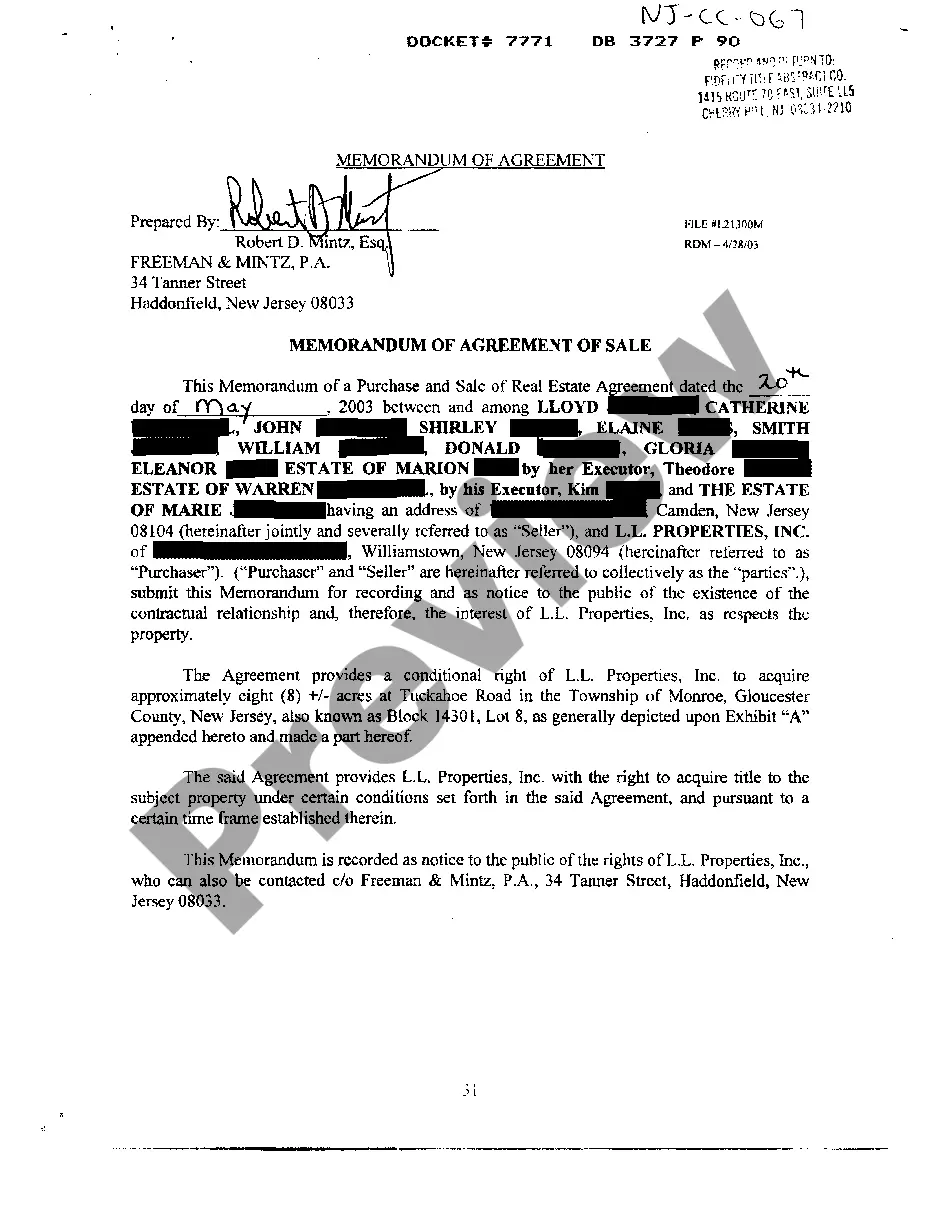

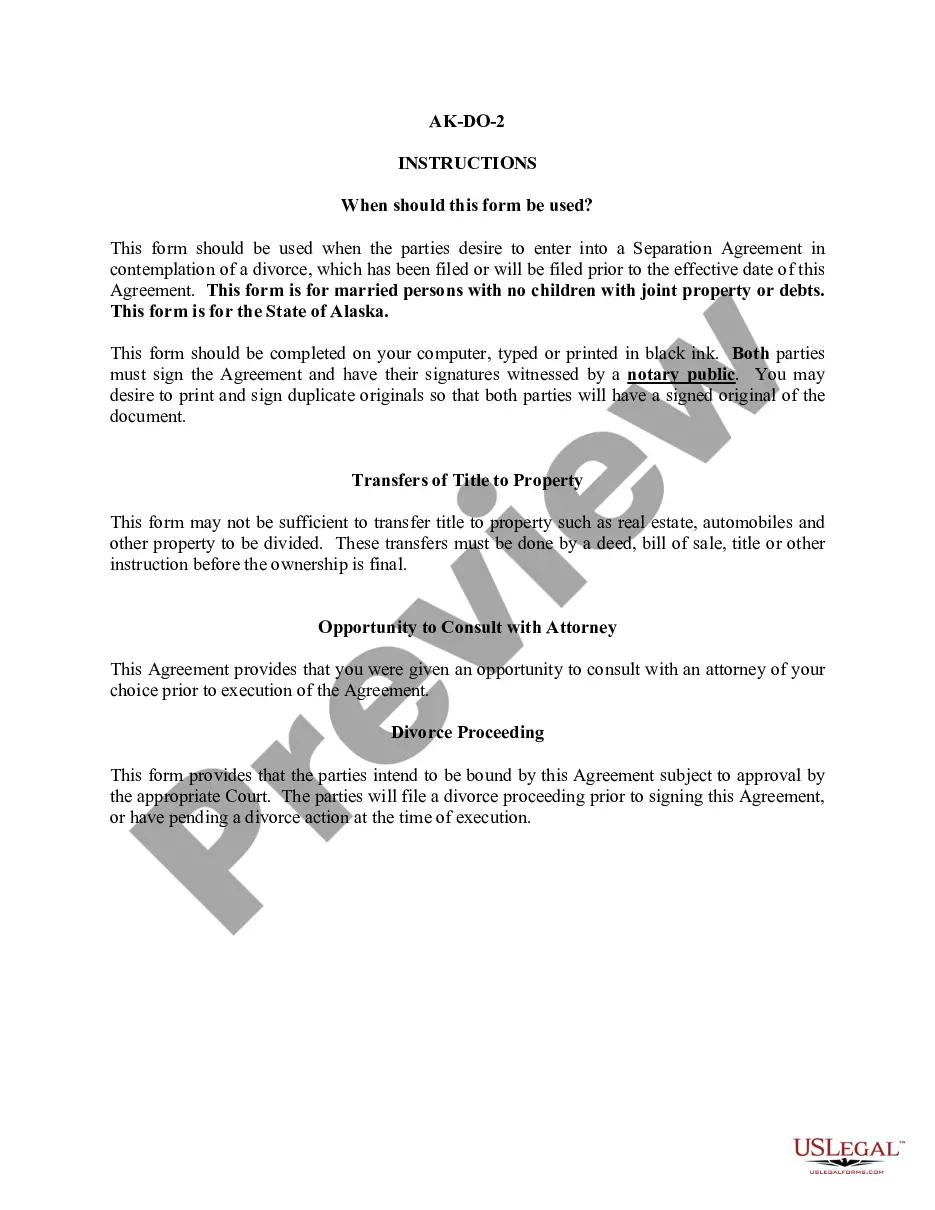

Sample Purchase Home For Elderly

Description

How to fill out Sample Agreement Of Purchase And Sale By Park - Ohio Industries, Inc., PO Acquisition Company, Inc., Kay Home Products, Inc., And Edward F. Crawford?

It’s common knowledge that you cannot transform into a legal practitioner instantly, nor can you swiftly learn how to draft Sample Purchase Home For Elderly without possessing a specialized skill set.

Compiling legal documents is an extensive endeavor that demands specific training and expertise. So, why not entrust the creation of the Sample Purchase Home For Elderly to the experts.

With US Legal Forms, one of the most thorough collections of legal templates, you can discover everything from court documents to templates for internal corporate correspondence.

You can regain access to your forms from the My documents tab anytime. If you are a current client, just Log In, and find and download the template from the same tab.

Regardless of your documents’ aim—whether financial, legal, or personal—our platform has you covered. Experience US Legal Forms today!

- Understand the form you require by utilizing the search feature at the top of the page.

- View it (if this option is available) and review the accompanying description to determine if Sample Purchase Home For Elderly is what you seek.

- Restart your search if you require a different template.

- Create a complimentary account and choose a subscription plan to acquire the form.

- Select Buy now. Once the payment is processed, you can download the Sample Purchase Home For Elderly, complete it, print it, and send or mail it to the necessary parties or organizations.

Form popularity

FAQ

Yes, a 70-year-old can apply for a 30-year mortgage, but lenders will evaluate their financial stability and credit history. While age alone does not disqualify someone from obtaining a long-term mortgage, factors like income, assets, and repayment ability play a significant role. When looking at a sample purchase home for elderly individuals, it's important to consult with a mortgage specialist to explore suitable options based on their unique circumstances.

When you consider a sample purchase home for elderly parents, start by assessing their needs. Determine the type of home that suits their lifestyle, whether it's a single-story house or a community designed for seniors. Involve them in the decision-making process to ensure their preferences are met. Additionally, explore financing options that align with their financial situation, and consult a real estate agent experienced in working with elderly clients.

The 20 30 3 rule simplifies the home buying process, specifically for those looking at a sample purchase home for elderly. It suggests that you should make a 20% down payment, aim for a monthly mortgage payment not exceeding 30% of your income, and seek a home priced at no more than three times your annual salary. This rule helps you maintain financial stability while securing a home that meets your needs, especially as you plan for retirement or other lifestyle changes.

People transfer property for $1 for various reasons, often involving family members and financial considerations. This method can simplify the transfer process and may help in estate planning. Furthermore, using the 'sample purchase home for elderly' concept allows for smoother transitions and can protect the property from outside claims, making it a beneficial option in many cases.

Protecting an elderly parent's assets often involves careful financial planning and legal strategies. Some common methods include setting up trusts, gifting portions of the estate, or utilizing the 'sample purchase home for elderly' approach to keep the home within the family. Consulting with a knowledgeable attorney can help to ensure the right steps are taken to safeguard your parent's financial future.

Buying your mom's house for $1 is possible, but it typically requires more than a simple transaction. In many cases, this type of sale involves legal considerations, such as property appraisals, tax implications, and potential ramifications for Medicaid eligibility. If you're considering the 'sample purchase home for elderly' option, it’s wise to consult with a legal expert to ensure that all aspects are properly addressed.

Yes, you can buy a house and put the deed in another person's name such as your child's or parents' names. However, consider all the risks of buying a home and putting another name on the deed.

If your elderly parents want to move into a new home but can't obtain financing on their own, you might be able to help through a loan commonly known as the Family Opportunity Mortgage. The Family Opportunity Mortgage makes it easier for children to purchase or refinance a home for their parents.

Co-Sign On A Mortgage Co-signing a mortgage for your parents means you guarantee the loan for them. If you have a better credit score than them or a larger consistent income, this added protection makes it easier for the lender to grant them a loan they could not qualify for on their own.

Banks will generally not allow you to simply assume a mortgage title entirely so you'll need to apply for a new home loan and the old loan will need to be paid out.