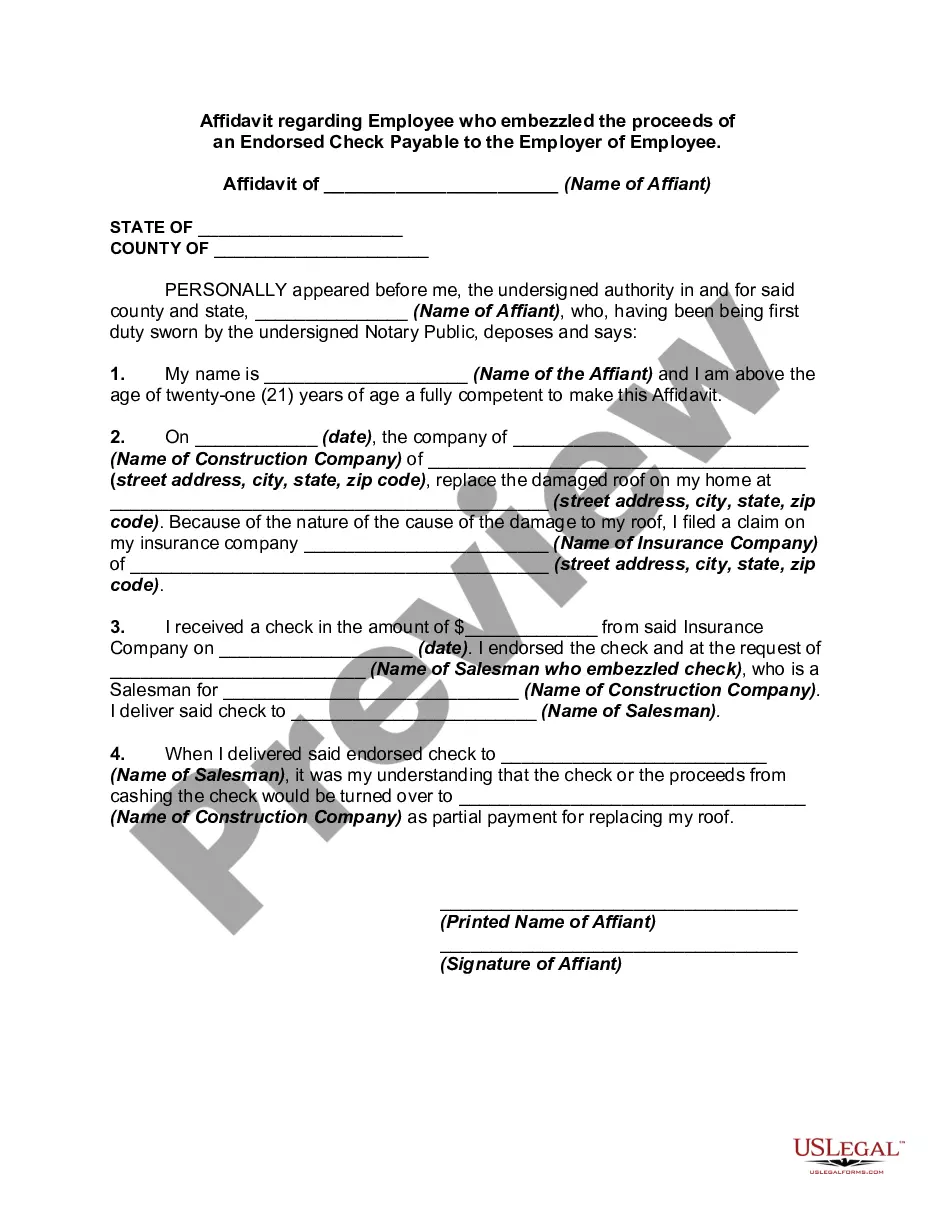

Property Theft Who Formed

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

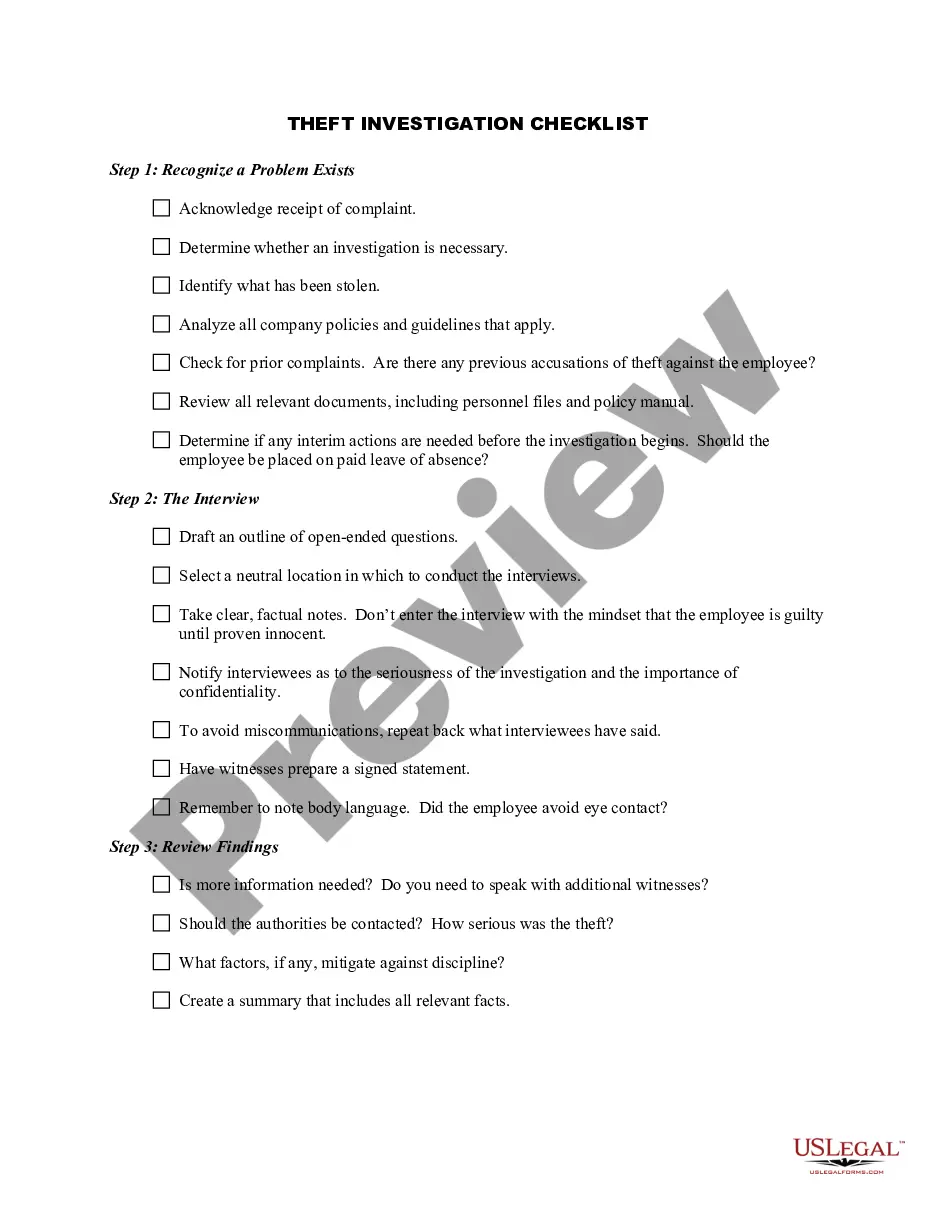

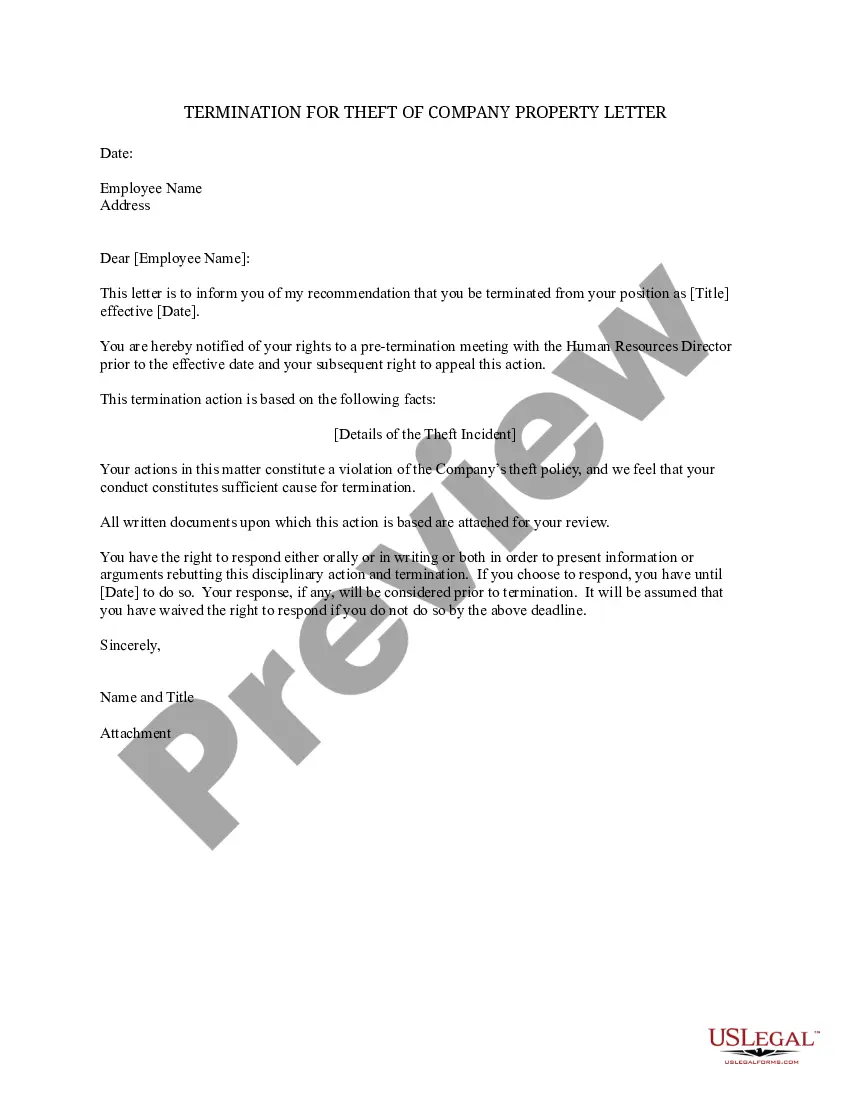

How to fill out Stolen Property Investigation Statement Checklist?

Managing legal documents can be daunting, even for the most adept experts.

When you are looking for a Property Theft Who Formed and can't dedicate time to find the right and current version, the tasks can become taxing.

US Legal Forms addresses all your needs, from personal to business paperwork, all in one location.

Utilize advanced features to complete and oversee your Property Theft Who Formed.

Here are the steps to follow after acquiring the form you need: Verify that this is the correct form by previewing it and reviewing its details. Ensure that the document is valid in your state or county. Click Buy Now when you are ready. Choose a monthly subscription option. Select the file format you desire, and Download, complete, eSign, print, and send your document. Make the most of the US Legal Forms online catalog, backed by 25 years of expertise and reliability. Enhance your daily document management into a seamless and user-friendly process today.

- Access a resource library of articles, guides, and materials pertinent to your situation and requirements.

- Conserve time and effort in finding the documents you require, and make use of US Legal Forms' sophisticated search and Review feature to locate and obtain Property Theft Who Formed.

- For those with a monthly subscription, Log Into your US Legal Forms account, search for the form, and get it.

- Check the My documents tab to see the documents you've previously saved and to organize your folders as necessary.

- If this is your first experience with US Legal Forms, set up a free account and gain unlimited access to all the library's advantages.

- A comprehensive online form directory can be a game changer for anyone aiming to handle these circumstances effectively.

- US Legal Forms is a leader in online legal forms, with more than 85,000 state-specific legal documents accessible to you at any time.

- With US Legal Forms, you can access documents tailored to your state or county.

Form popularity

FAQ

You will still use Form 4684 to figure your losses and report them on Form 1040, Schedule A. For tax years prior to 2018 and after 2025, you can only deduct casualty losses not reimbursed or reimbursable by insurance or other means. You'll need to subtract $100 from each casualty loss of personal property.

You must use a separate Form 4684 (through line 12) for each casualty or theft event involving personal-use property. If reporting a qualified disaster loss, see the instructions for special rules that apply before completing this section.) number assigned by FEMA.

What Is Form 4684: Casualties and Thefts? Form 4684 is an Internal Revenue Service (IRS) form for reporting gains or losses from casualties and thefts which may be deductible for taxpayers who itemize deductions. Casualty losses can be the result of fires, floods, and other disasters.

To elect to deduct the loss as a casualty loss, complete Form 4684 as follows: On line 1, enter the name of the financial institution and "Insolvent Financial Institution." Skip lines 2 through 9. Enter the amount of the loss on line 10, and complete the rest of Section A.

Of course, not all types of interest are deductible. Specifically, the IRS does not allow you to deduct personal interest, such as: The interest you pay on a loan to buy a car for personal use. Credit card and installment loan interest on personal expenses.