Mortgage Right Fort Mill

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

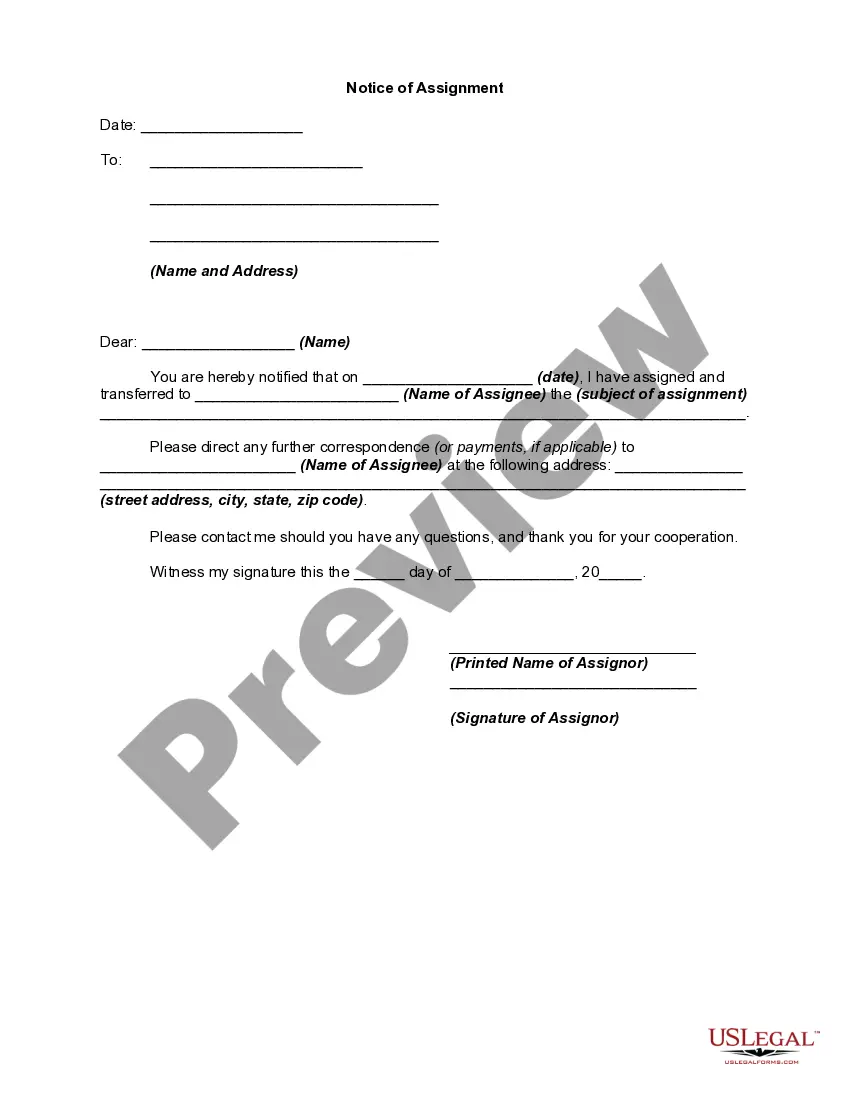

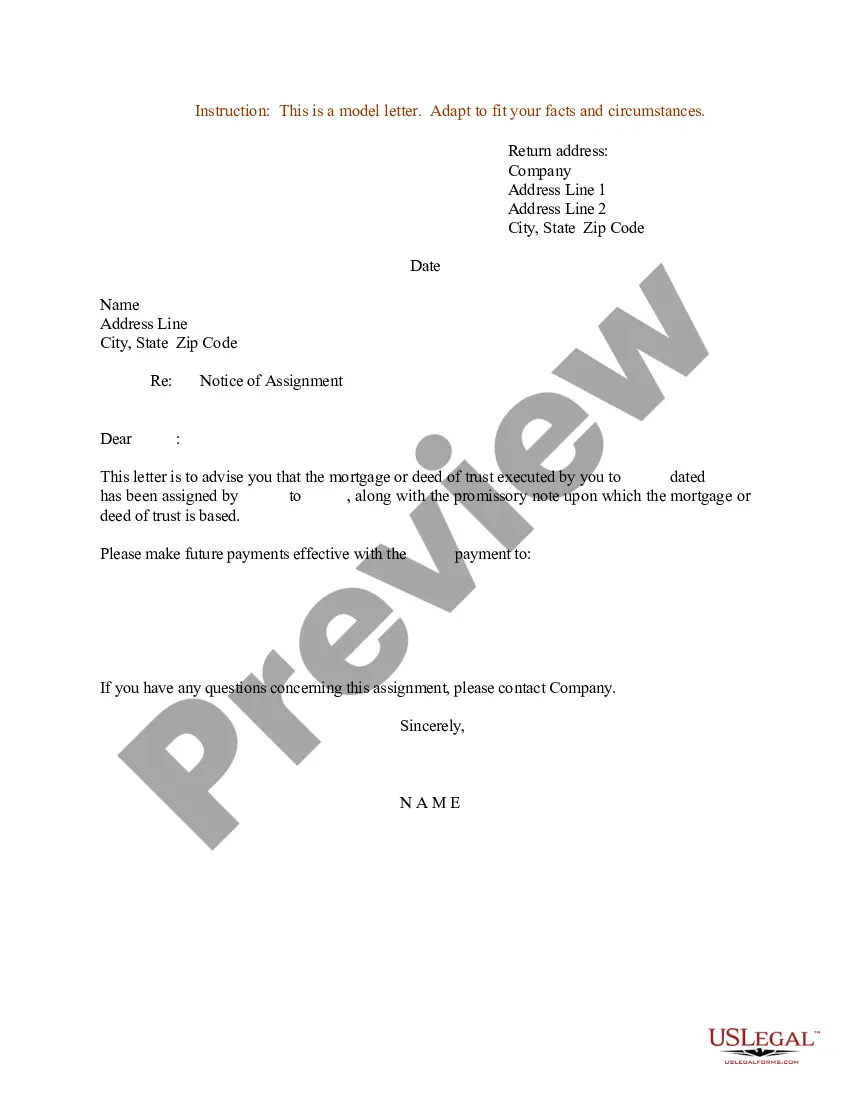

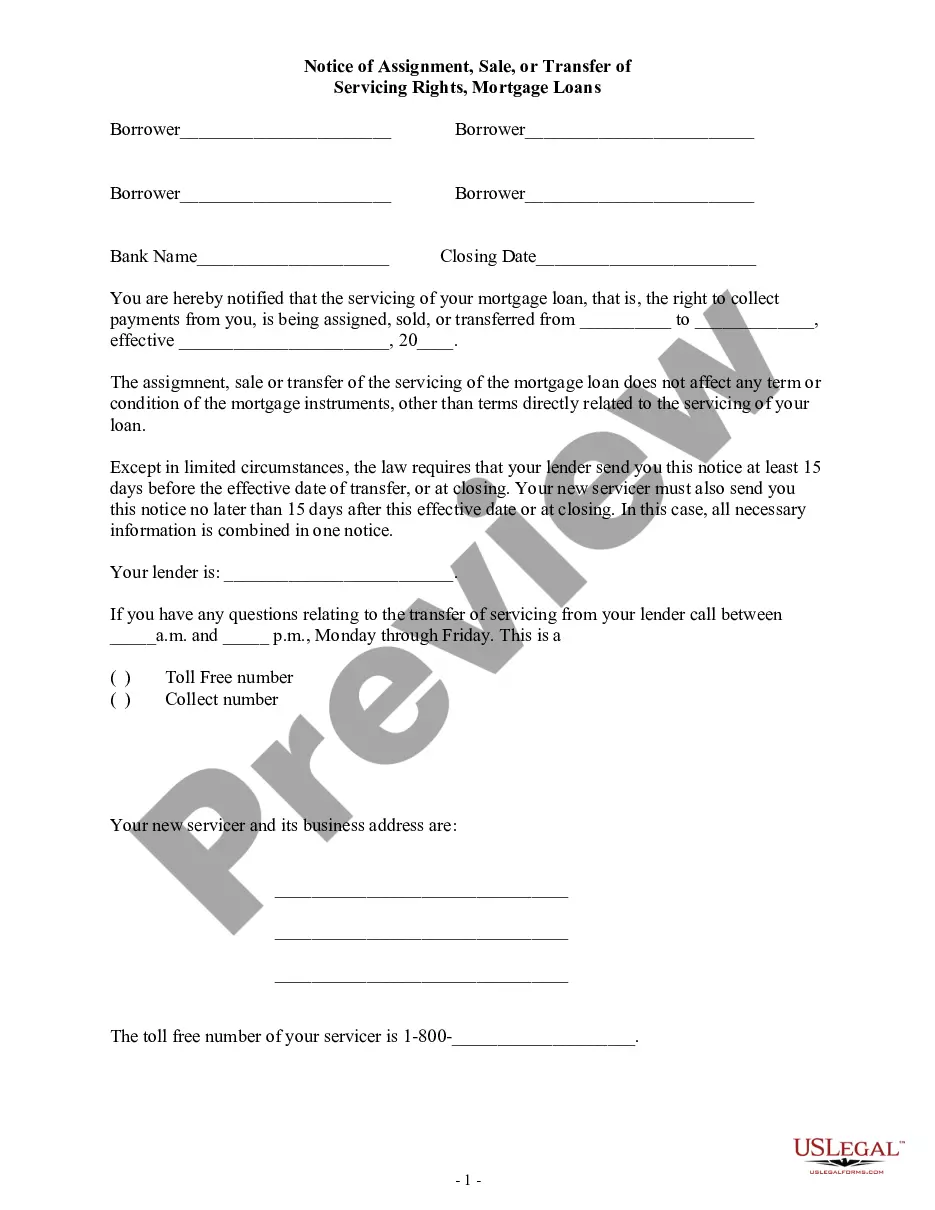

How to fill out Notice Of Assignment, Sale, Or Transfer Of Servicing Rights, Mortgage Loans?

Whether for commercial reasons or for individual matters, everyone must deal with legal issues at some stage in their life.

Filling out legal documents requires meticulous care, starting from selecting the correct form template.

Once downloaded, you can fill out the form using editing software or print it and complete it by hand. With an extensive US Legal Forms catalog available, you will never have to waste time searching for the suitable template online. Take advantage of the library’s user-friendly navigation to obtain the right form for any scenario.

- Obtain the template you require using the search bar or catalog navigation.

- Review the form’s description to ensure it matches your circumstances, state, and region.

- Click on the form’s preview to examine it.

- If it is the wrong document, return to the search tool to find the Mortgage Right Fort Mill template you need.

- Download the file if it satisfies your specifications.

- If you possess a US Legal Forms account, click Log in to access previously saved documents in My documents.

- If you do not have an account yet, you can acquire the form by clicking Buy now.

- Select the appropriate pricing option.

- Complete the account registration form.

- Choose your payment method: you can utilize a credit card or PayPal account.

- Select the desired file format and download the Mortgage Right Fort Mill.

Form popularity

FAQ

As a rule of thumb, experts often say refinancing isn't worth it unless you drop your interest rate by at least 0.5% to 1%. But that may not be true for everyone. Refinancing for a 0.25% lower rate could be worth it if: You are switching from an adjustable-rate mortgage to a fixed-rate mortgage.

Below are some downsides to refinancing you may consider before applying. You Might Not Break Even. ... The Savings Might Not Be Worth The Effort. ... Your Monthly Payment Could Increase. ... You Could Reduce The Equity In Your Home.

Securing a lower interest rate through a refinance reduces your cost of borrowing so you'll pay less on your personal loan overall. Refinancing to a longer loan term offers lower minimum monthly payments. You will likely pay more toward the loan overall by extending the repayment timeline due to interest charges.

More specifically, it's often a good idea to refinance if you can lower your interest rate by one-half to three-quarters of a percentage point, and if you plan to stay in your home long enough to recoup the refinance closing costs.

More specifically, it's often a good idea to refinance if you can lower your interest rate by one-half to three-quarters of a percentage point, and if you plan to stay in your home long enough to recoup the refinance closing costs.