Llc Form Companies File With S Corp

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

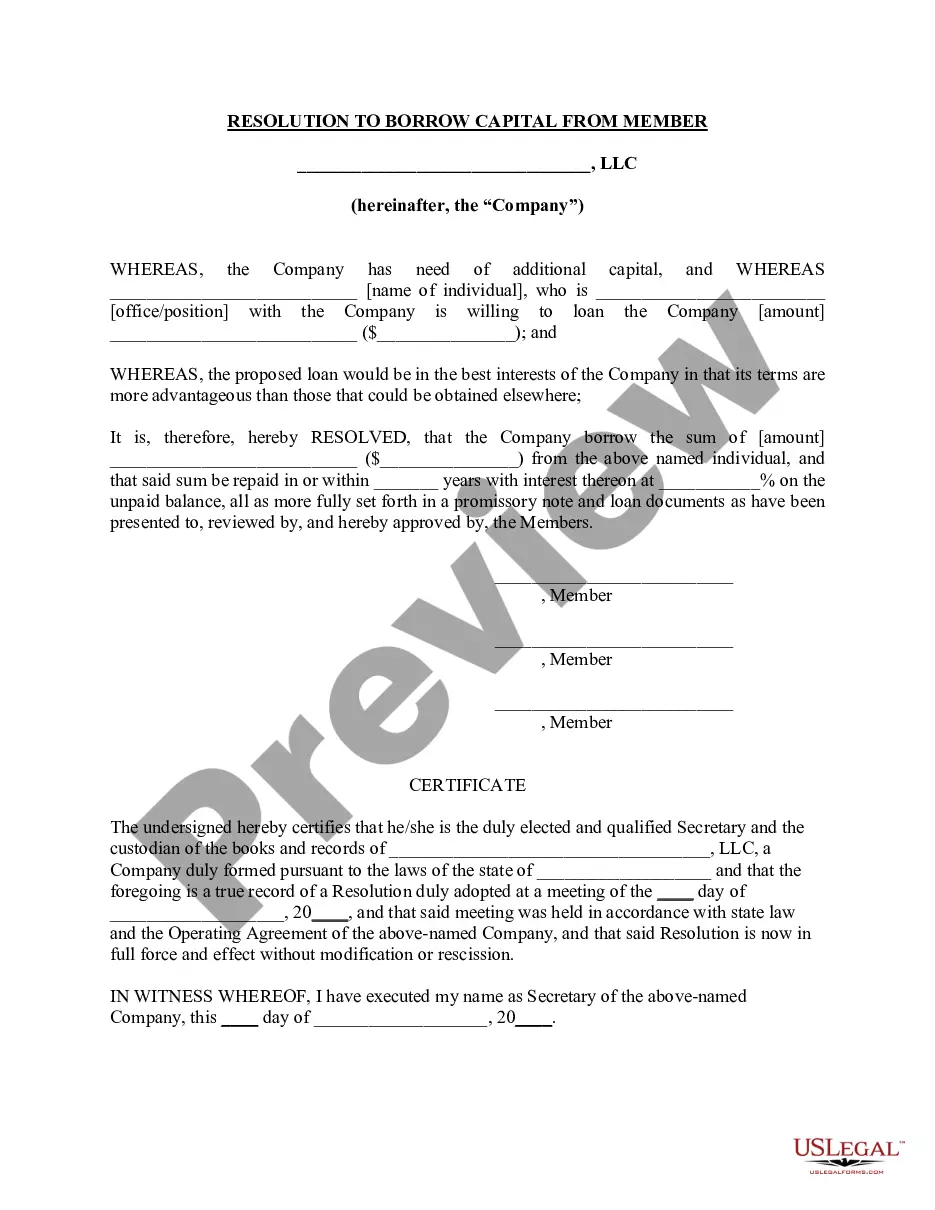

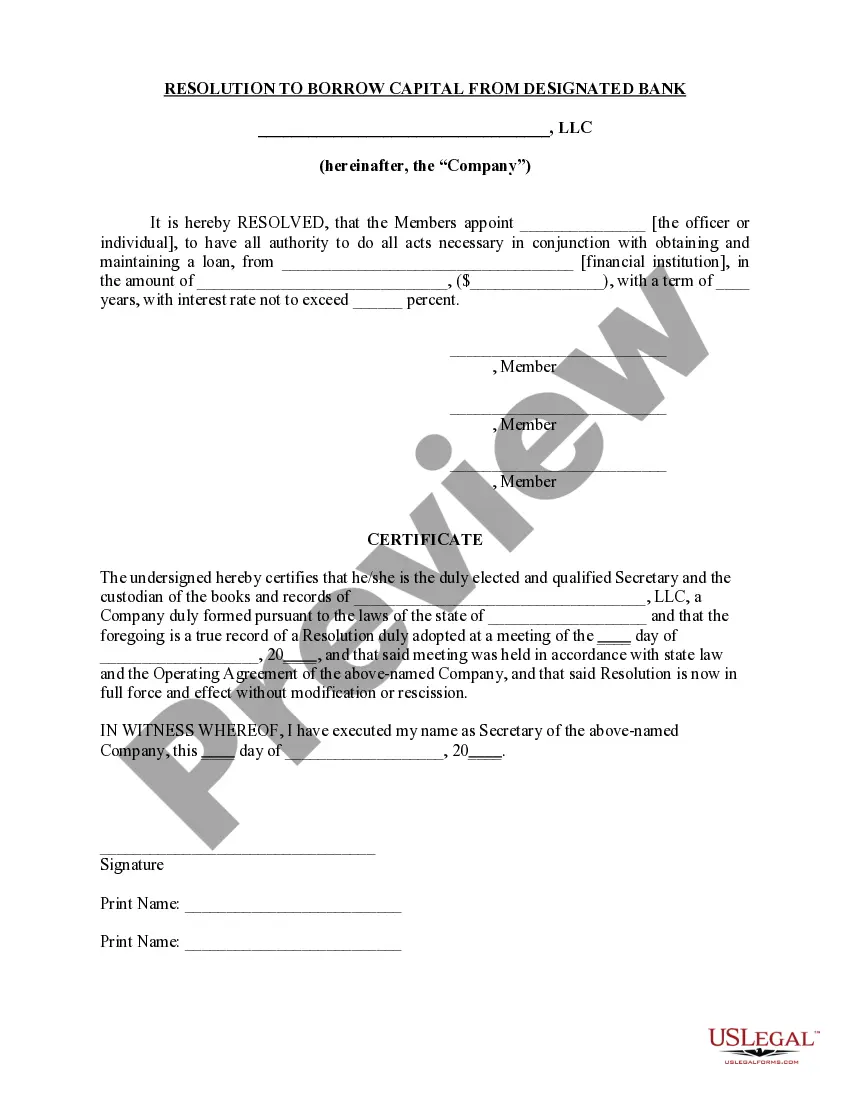

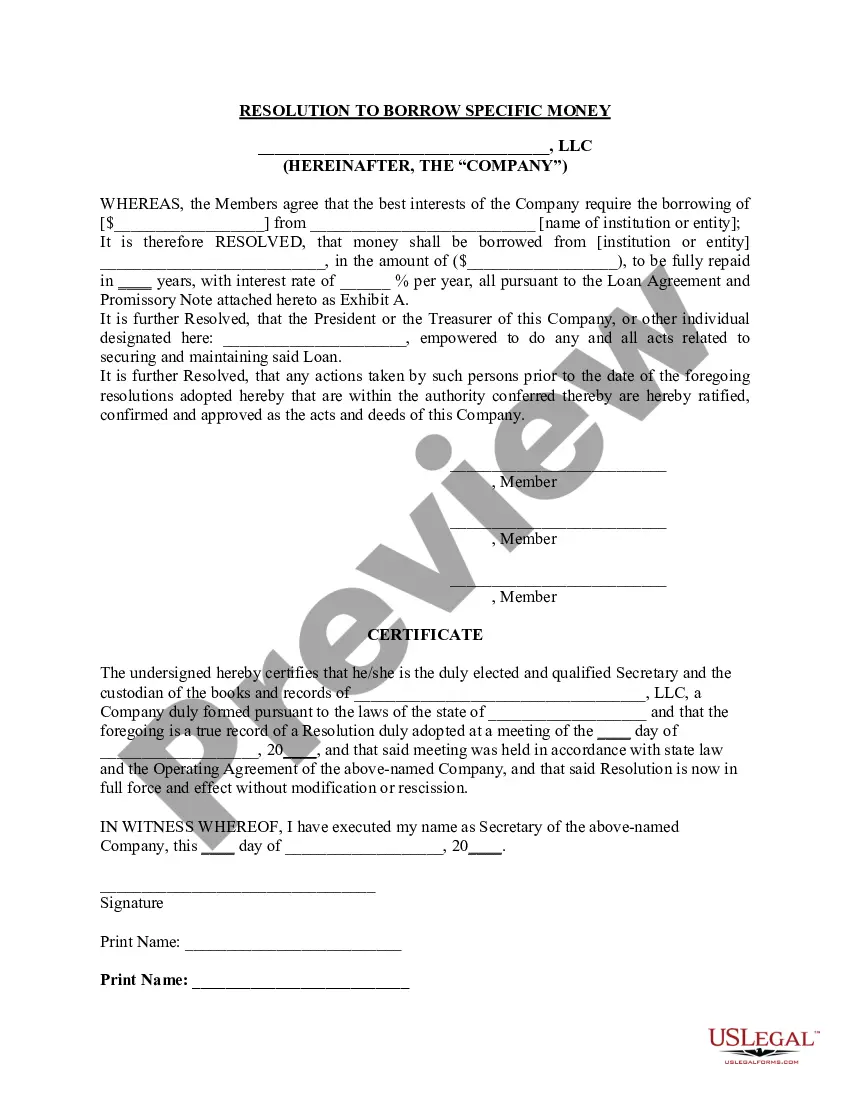

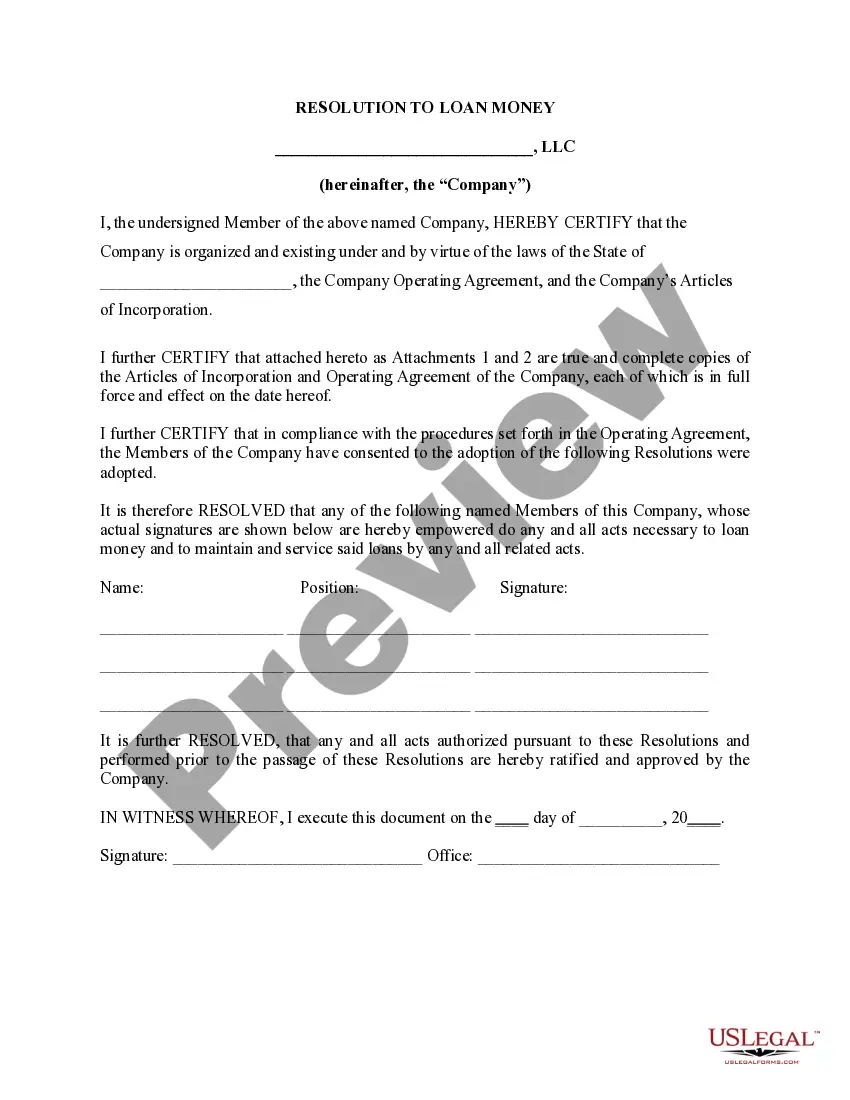

How to fill out Resolution Of Meeting Of LLC Members To Borrow Money?

- Start by visiting the US Legal Forms website and log into your account if you are a returning user. Ensure your subscription is active to access the necessary forms.

- For new users, browse the extensive library of legal forms. Use the Preview mode to review the details and confirm it matches your jurisdiction's requirements.

- If the selected form is not suitable, utilize the Search tab to find the correct template tailored to your needs.

- Once you've found the right document, click on the Buy Now button and select your preferred subscription plan. Registration is required to access the full library.

- After choosing your payment method, enter the necessary credit card information or use PayPal to complete your purchase.

- Finally, download your LLC form to your device. You can access and manage all your downloaded documents anytime in the My Forms section.

In conclusion, using US Legal Forms simplifies the process of filing LLC forms for companies choosing to file as S Corps. With an extensive library and support from legal experts, you can confidently prepare your documents.

Start your journey today by visiting US Legal Forms and explore the possibilities!

Form popularity

FAQ

LLCs typically file Form 8832 to elect their classification, but if an LLC wants to be taxed as an S Corporation, it should file Form 2553. This distinction is important because LLC form companies file with S Corp to optimize their tax obligations. Make sure to file Form 2553 on time to ensure that your S Corp election is accepted. Resources like US Legal Forms can simplify this process for you and help you stay compliant.

Yes, an LLC can elect to be treated as an S Corp by filing Form 2553. Many LLC form companies file with S Corp to take advantage of specific tax benefits, such as pass-through taxation. This flexibility allows LLCs to reduce their self-employment tax liability. If you are considering this option, check with a tax advisor or explore US Legal Forms for straightforward guidance.

To file for S Corporation status, you need to submit IRS Form 2553. This form allows LLC form companies to file with S Corp status and gain the tax benefits associated with it. Be sure to complete all sections of the form accurately to avoid delays. For additional support, consider using the resources available on US Legal Forms to guide you through the process.

To elect for your LLC to be treated as an S corp, you must file Form 2553 with the IRS, as previously mentioned. It's important to do this within 75 days of forming your LLC or to request the election before the tax deadline of the current year. This election can help your LLC gain special tax treatment, making it essential for your business planning.

Transforming your S corp into an LLC involves a few key steps. Start by dissolving your S corporation, which requires filing the appropriate paperwork with your state. Next, you will need to create a new LLC and submit the necessary formation documents. This conversion allows you to enjoy the benefits that an LLC offers, such as flexibility and simpler taxation.

To obtain S corp status for your LLC, you need to file Form 2553 with the IRS. Make sure that all members of your LLC consent to the S corp election. Additionally, confirm that your LLC meets the eligibility criteria set by the IRS. By choosing this structure, you can benefit from tax advantages that many businesses find appealing.

Yes, an LLC that elects S Corp status may need to issue Form 1099 to contractors or vendors who received payments over a specified threshold. This is essential for reporting non-employee compensation accurately. As your business grows and you LLC form companies file with S corp, understanding your reporting obligations including 1099s becomes crucial for compliance.

Electing S Corp status for your LLC can provide tax advantages such as avoiding double taxation and minimizing self-employment tax on distributions. However, this election comes with specific requirements and regulations. It’s crucial to evaluate your business structure and consult a professional to see if this choice aligns with your financial goals. If you LLC form companies file with S corp, you can maximize these benefits effectively.

Deciding between an LLC and an S corp depends on your business goals. An LLC offers flexibility and less formal structure, while an S corp can provide tax advantages, especially regarding self-employment taxes. You might consider forming an LLC and then electing S Corp status later. Thus, exploring how you LLC form companies file with S corp can guide you in making a strategic choice for your startup.

The primary tax loophole for S corps is the ability to avoid self-employment taxes on distributions. Unlike wages, distributions taken from an S corp are not subject to payroll taxes. This means that if you LLC form companies file with S corp status, you can potentially save a significant amount on taxes by taking a reasonable salary and then distributing profits as dividends.