Unsecured Creditors In Chapter 13

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

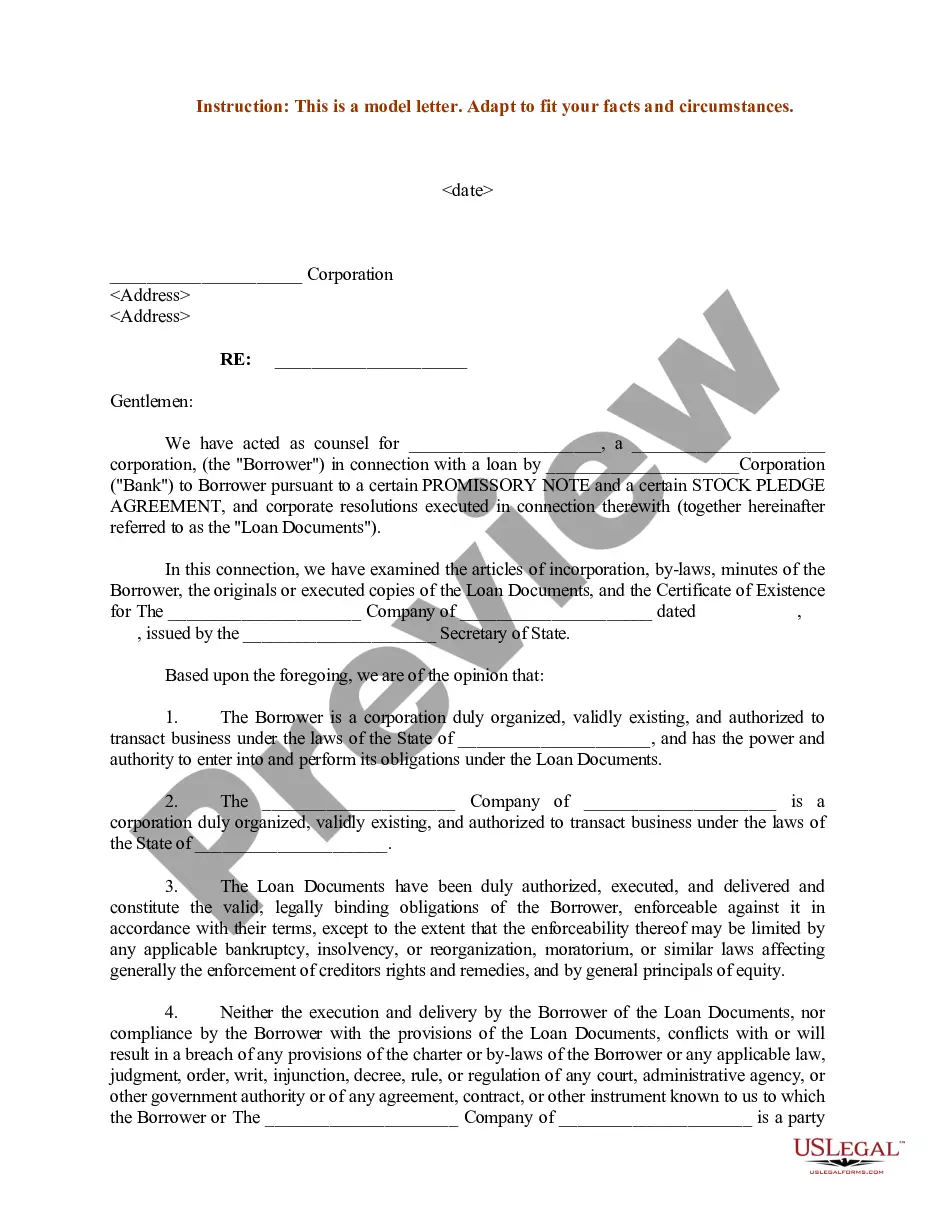

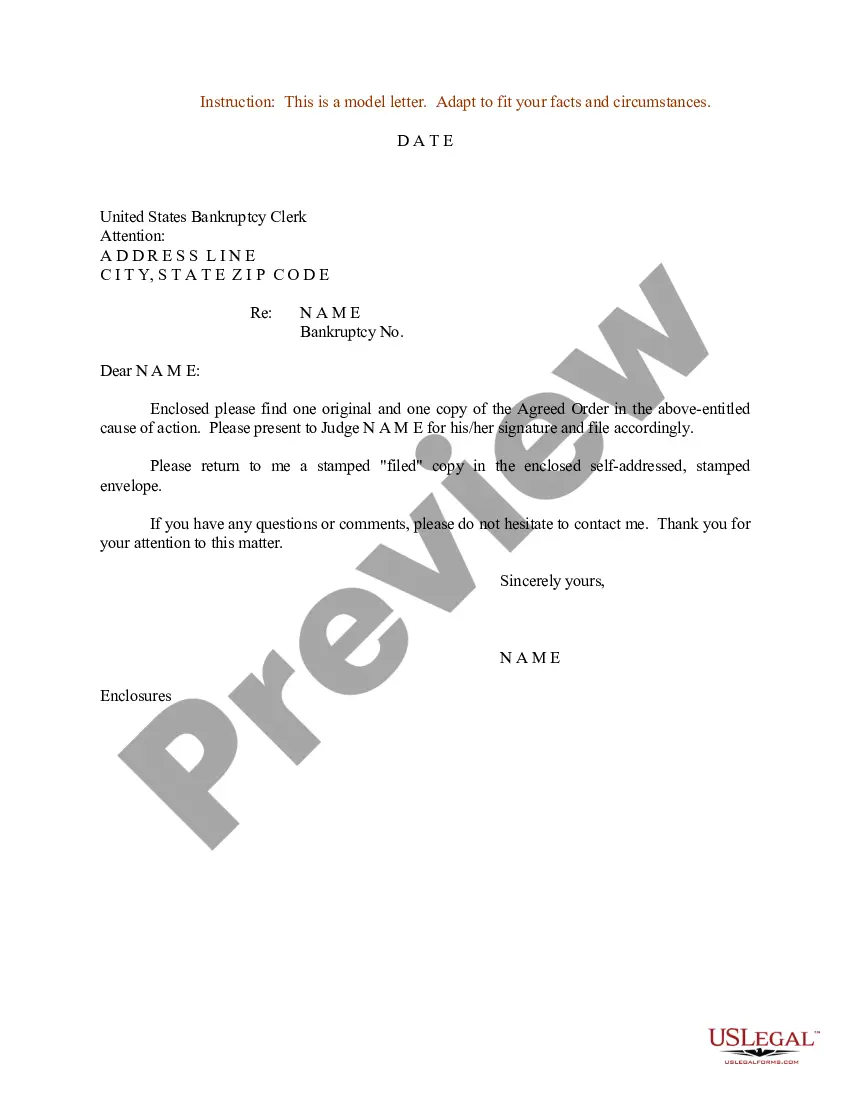

How to fill out Sample Letter For Application Of Unsecured Creditors For An Order Authorizing Employment Of Investment Banker?

Locating a reliable source to obtain the most up-to-date and suitable legal templates is a significant part of managing bureaucracy.

Acquiring the correct legal documents requires precision and meticulousness, which is why it is crucial to source Unsecured Creditors In Chapter 13 exclusively from trustworthy origins, such as US Legal Forms.

Eliminate the complications associated with your legal paperwork. Browse the extensive US Legal Forms database where you can find legal samples, assess their applicability to your scenario, and download them instantly.

- Use the library navigation or search bar to find your template.

- Check the form’s description to confirm it meets the criteria of your state and county.

- If available, view the form preview to ensure it is the template you need.

- If the Unsecured Creditors In Chapter 13 does not meet your criteria, return to the search to find the appropriate document.

- Once you are confident about the form’s applicability, download it.

- As an authorized customer, click Log in to verify your identity and access your chosen forms in My documents.

- If you haven’t created an account yet, click Buy now to acquire the template.

- Select the pricing option that suits your requirements.

- Proceed with registration to finalize your purchase.

- Complete your transaction by choosing a payment method (bank card or PayPal).

- Select the file format for downloading Unsecured Creditors In Chapter 13.

- After downloading the form to your device, you can modify it with the editor or print it for manual completion.

Form popularity

FAQ

Unsecured creditors are individuals or entities that provide loans or credit without securing the debt with collateral. In the context of bankruptcy, especially under chapter 13, these creditors do not have a legal claim to specific assets. Instead, they rely on the debtor's promise to repay the debt over time. Understanding how unsecured creditors in chapter 13 operate can help you navigate your financial obligations more effectively.

Unsecured debt. This type of debt, which includes credit card bills and medical debt, is usually fully dischargeable in bankruptcy. This means that, regardless of whether your creditor files a proof of claim, these debts will be forgiven at the end of the bankruptcy process.

Meanwhile, repayment to unsecured creditors is generally dependent on bankruptcy proceedings or successful litigation. An unsecured creditor must first file a legal complaint in court and obtain a judgment before proceeding with collection through wage garnishment and other types of liquidated borrower-owned assets.

In Chapter 13 bankruptcy, you must devote all of your "disposable income" to the repayment of your debts over the life of your Chapter 13 plan. Your disposable income first goes to your secured and priority creditors. Your unsecured creditors share any remaining amount.

The difference between the debtor's current monthly income and the debtor's expenses will be the monthly disposable income. This amount, multiplied by thirty-six months, will be the amount that must be paid to unsecured creditors in Chapter 13, for debtors below the median income.

You don't have to pay unsecured debts in full. Instead, you pay all your disposable income toward the debt during your three-year or five-year repayment plan. The unsecured creditors must receive as much as they would have if you'd filed Chapter 7.