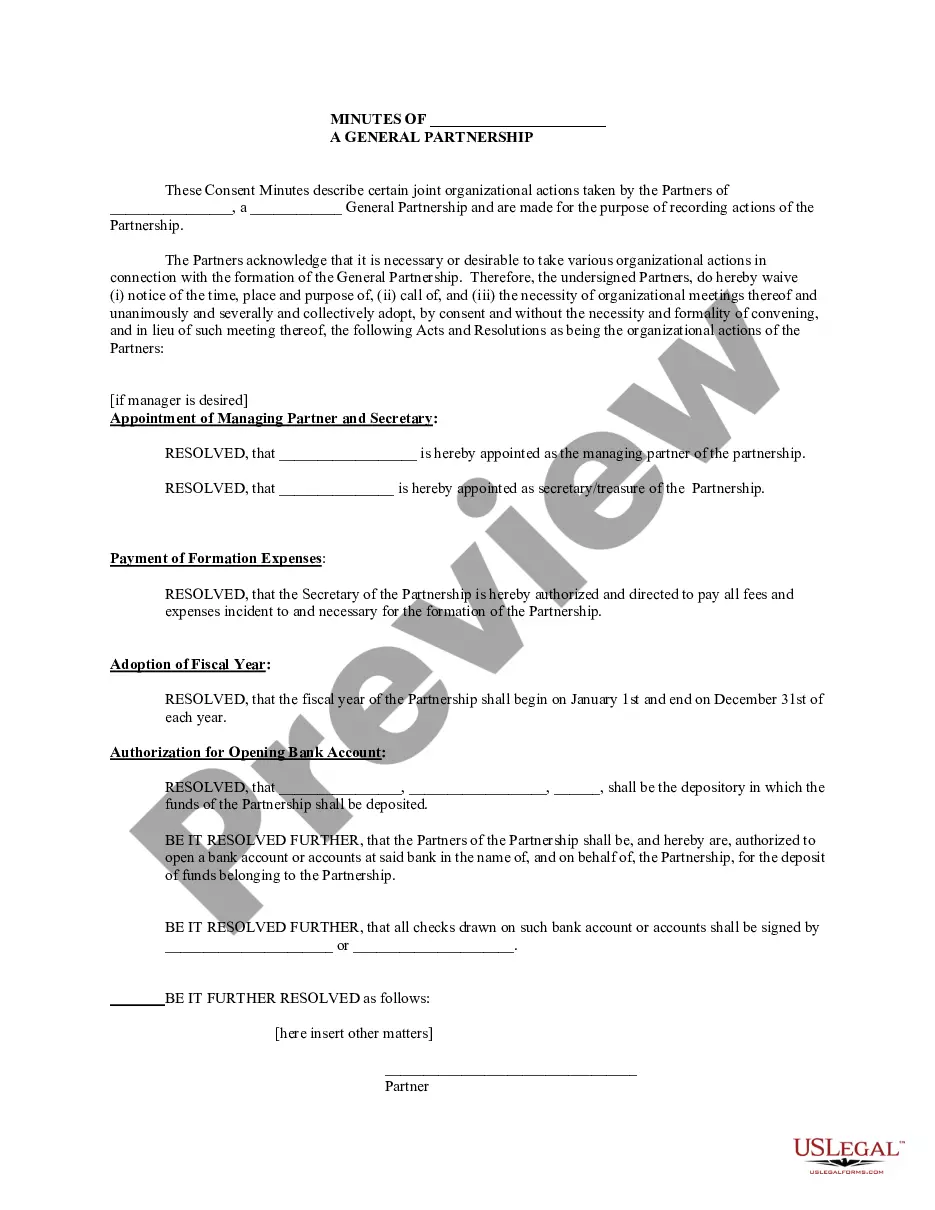

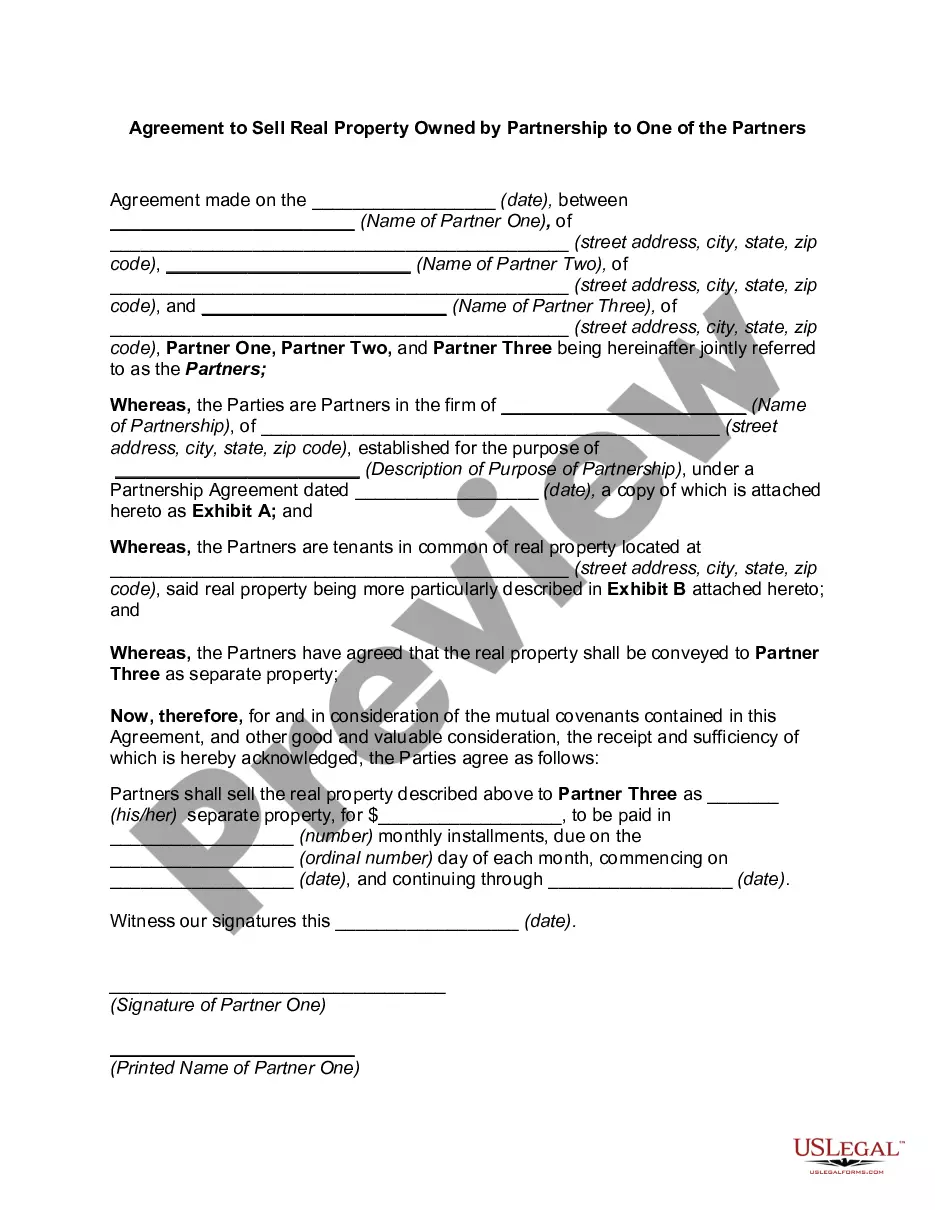

Partnership Resolution Form Withholding Tax

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Partnership Resolution To Sell Property?

Regardless of whether for corporate needs or personal issues, everyone encounters legal circumstances at some stage in their life. Completing legal documents requires meticulous attention, starting from selecting the appropriate form example. For example, if you choose an incorrect version of the Partnership Resolution Form Withholding Tax, it will be rejected upon submission. Thus, it is crucial to have a trustworthy source of legal documents like US Legal Forms.

If you need to acquire a Partnership Resolution Form Withholding Tax example, adhere to these straightforward steps: Find the template you require by utilizing the search bar or catalog navigation. Review the form’s details to ensure it aligns with your situation, state, and county. Click on the form’s preview to examine it. If it is the wrong document, return to the search feature to locate the Partnership Resolution Form Withholding Tax sample you need. Obtain the file when it fulfills your criteria. If you already possess a US Legal Forms account, click Log in to access previously saved templates in My documents. In case you do not yet have an account, you can acquire the form by clicking Buy now. Select the appropriate pricing option. Complete the account registration form. Choose your payment method: utilize a credit card or PayPal account. Select the file format you desire and download the Partnership Resolution Form Withholding Tax. Once it is saved, you can fill out the form using editing software or print it and complete it manually.

- With an extensive US Legal Forms catalog available, you never have to waste time searching for the correct template online.

- Make use of the library’s easy navigation to find the suitable template for any event.

Form popularity

FAQ

Generally, NRA withholding describes the withholding regime that requires 30% withholding on a payment of U.S. source income and the filing of Form 1042 and related Form 1042-S. Payments to all foreign persons, including nonresident alien individuals, foreign entities and governments, may be subject to NRA withholding.

A withholding foreign partnership (WP) is any foreign partnership that has entered into a WP withholding agreement with the IRS and is acting in that capacity.

A nonwithholding foreign partnership has three partners: a nonresident alien individual; a foreign corporation, and a U.S. citizen. You make a payment of U.S. source interest to the partnership. Assume that the payment is subject to Chapter 3 withholding but is not a withholdable payment.

Income Tax: Partnership firms are liable to pay income tax at a rate of 30% on their taxable income. Surcharges: If the taxable income of the partnership firm exceeds one crore rupees, a surcharge of 12% is applicable in addition to the income tax.

Under the law passed at the end of 2017, the purchaser of a partnership interest that is being sold by a foreign person is generally required to withhold 10% of the sales price of the partnership interest. This 10% withholding must be remitted to the Internal Revenue Service (IRS) no later than 20 days after closing.