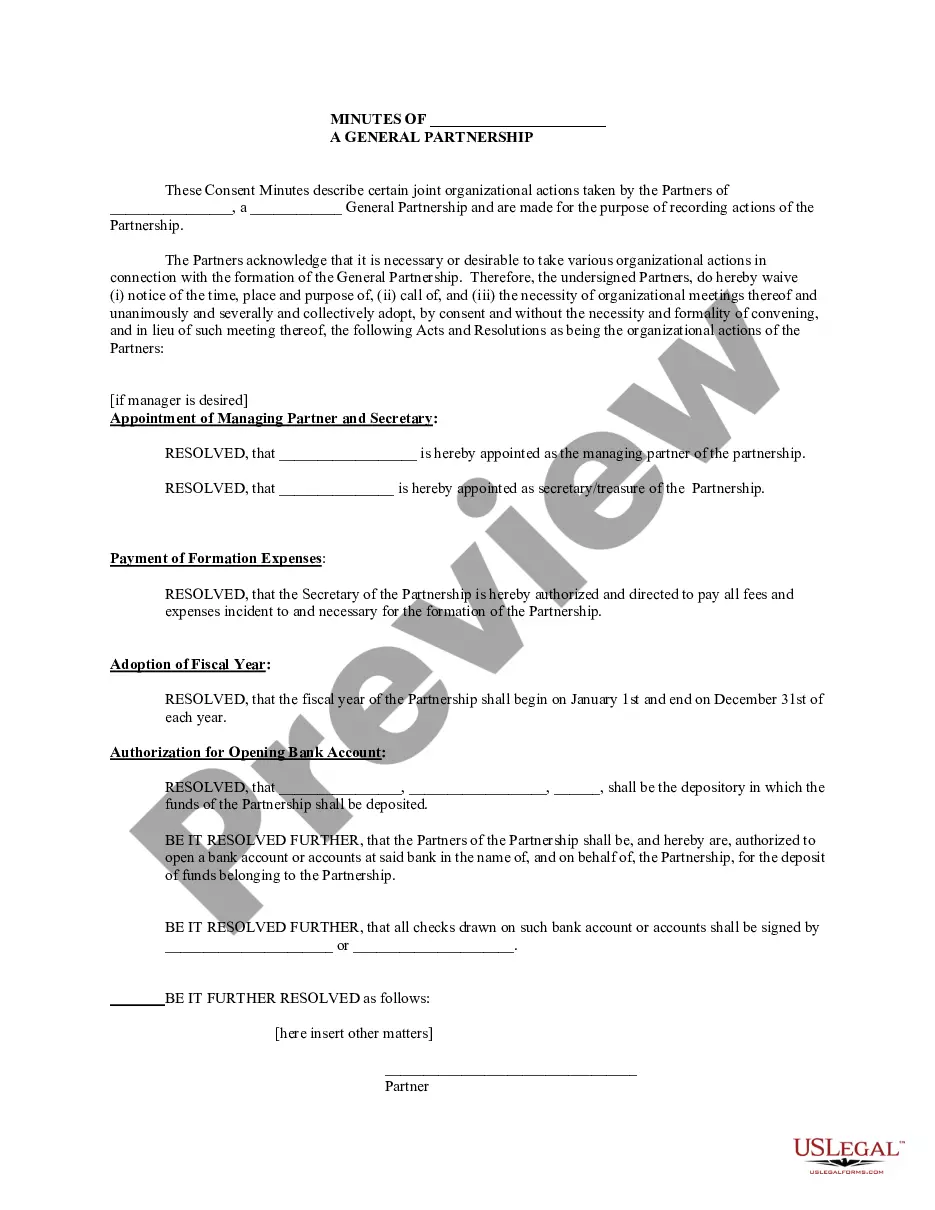

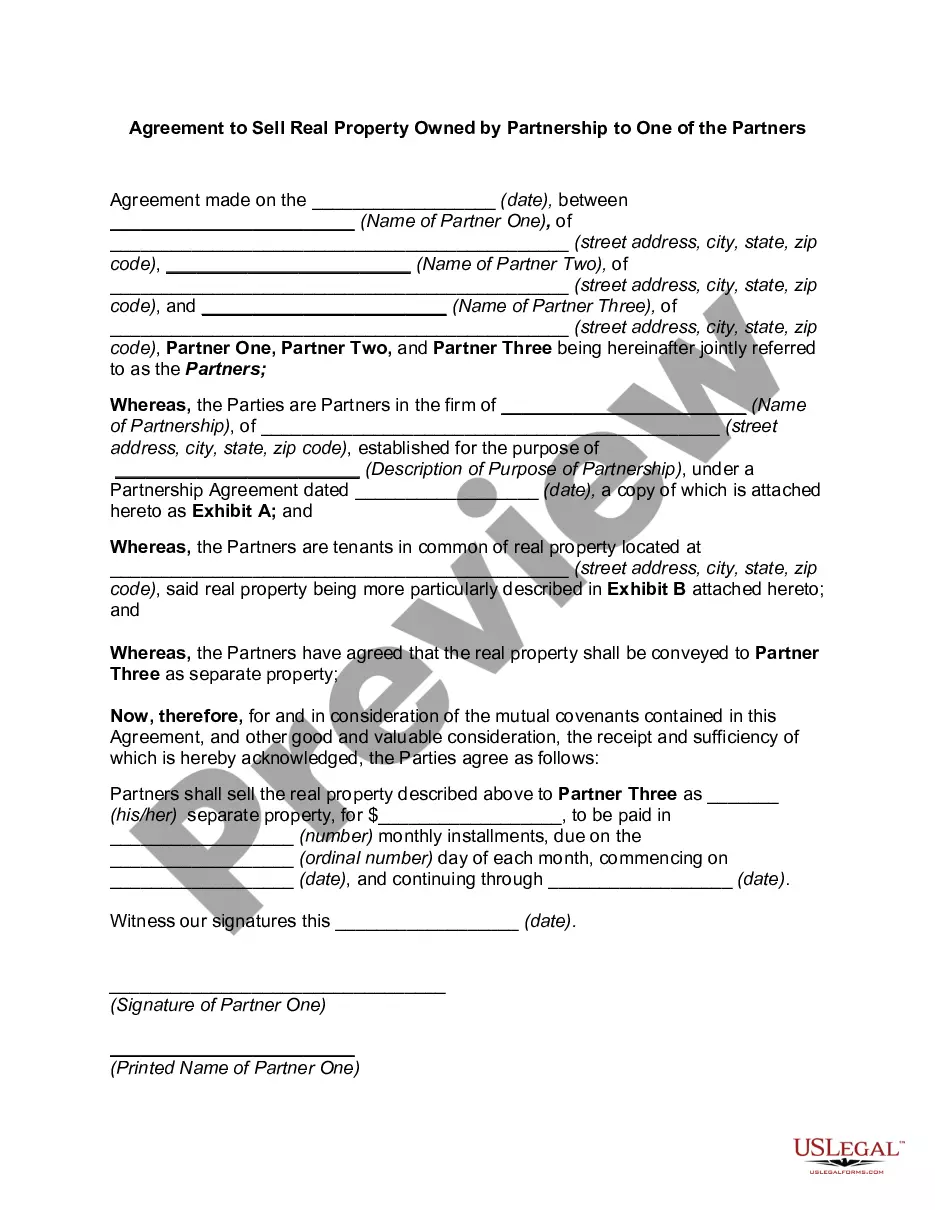

Partnership Resolution Form Withholding

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Partnership Resolution To Sell Property?

Legal administration can be perplexing, even for seasoned professionals.

When you are seeking a Partnership Resolution Form Withholding and lack the time to invest in locating the correct and current version, the procedures may be overwhelming.

US Legal Forms meets any needs you might have, from personal to business documents, all in one location.

Utilize advanced tools to complete and manage your Partnership Resolution Form Withholding.

Here are the steps to follow after accessing the form you desire: Confirm this is the correct form by previewing it and reviewing its description. Ensure that the template is accepted in your state or county. Click Buy Now when you are prepared. Choose a subscription plan. Select the file format you require, and Download, complete, sign, print, and send your document. Enjoy the US Legal Forms online library, backed by 25 years of experience and reliability. Transform your routine document management into a simple and user-friendly process today.

- Access a resource library of articles, guides, and manuals related to your situation and requirements.

- Save time and effort in searching for the documents you need, and utilize US Legal Forms’ advanced search and Preview feature to find Partnership Resolution Form Withholding and download it.

- If you possess a subscription, Log In to your US Legal Forms account, search for the form, and download it.

- Check your My documents tab to view the documents you previously saved and manage your folders as needed.

- If this is your first time with US Legal Forms, create a free account and enjoy unlimited access to all the platform's benefits.

- A robust online form repository could be transformative for anyone who wishes to navigate these matters efficiently.

- US Legal Forms is a frontrunner in digital legal forms, offering over 85,000 state-specific legal documents available to you at any moment.

- With US Legal Forms, you can access state- or county-specific legal and business forms.

Form popularity

FAQ

The partnership must withhold the full amount of each distribution to the transferee until it has withheld 10% of the amount realized on the transfer (reduced by any amounts withheld by the transferee) plus interest.

Understanding the New IRS Form W-4P - YouTube YouTube Start of suggested clip End of suggested clip And step five sign and date the form frequently asked questions why did the IRS change the w4p. FormMoreAnd step five sign and date the form frequently asked questions why did the IRS change the w4p. Form the IRS redesigned the w4p form to simplify your withholding.

Note: Currently, the withholding tax rate for effectively connected income allocable to non-corporate foreign partners is 37%, and 21% for corporate foreign partners. A publicly traded partnership must withhold tax on actual distributions of effectively connected income.

Other business structures ? including sole proprietorships, partnerships and S corporations ? are considered pass-through entities; their incomes are taxed at the owner's personal tax rate, which is between 10% to 37%. Limited liability companies (LLCs) may either pay taxes as a corporation or as a pass-through entity.

The withholding rate is California's highest tax rate for each partner's entity type. The current withholding rates are: Noncorporate partners - 12.3 percent. Corporate partners - 8.84 percent.