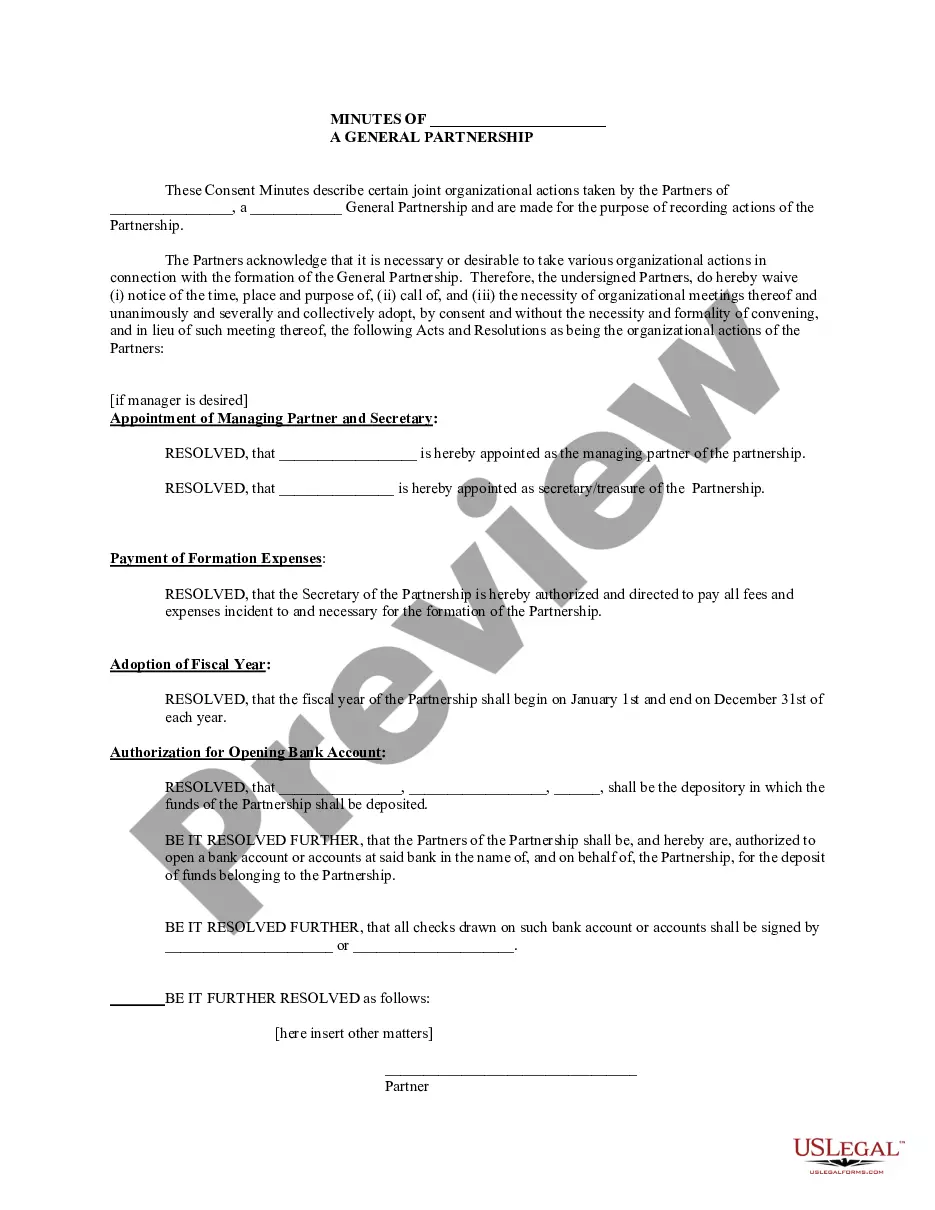

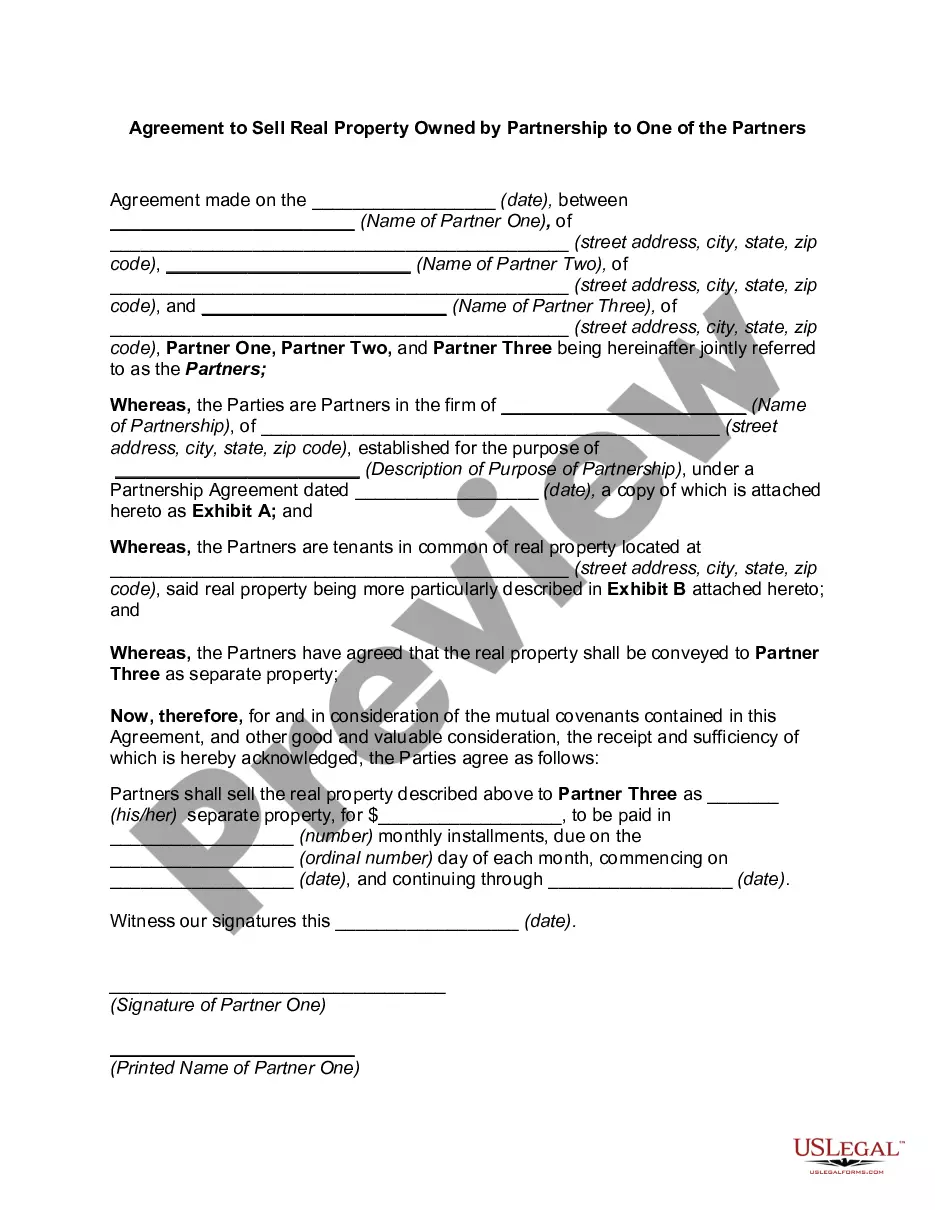

Partnership Formation Sample Problems

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Partnership Resolution To Sell Property?

The Partnership Formation Example Issues you observe on this site is a versatile official outline created by expert attorneys in accordance with federal and local regulations.

For over 25 years, US Legal Forms has delivered to individuals, businesses, and lawyers more than 85,000 authenticated, state-specific documents for any commercial and personal situation. It is the quickest, simplest, and most trustworthy method to acquire the paperwork you require, as the service assures the utmost level of data security and anti-malware defense.

Subscribe to US Legal Forms to have validated legal templates for all of life’s situations at your fingertips.

- Search for the document you require and review it.

- Browse the example you searched for and preview it or verify the form description to ensure it meets your requirements. If it doesn’t, use the search bar to find the suitable one. Click Buy Now when you have identified the template you need.

- Subscribe and sign in.

- Choose the pricing plan that fits you and create an account. Utilize PayPal or a credit card to process a quick payment. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the fillable template.

- Select the format you desire for your Partnership Formation Example Issues (PDF, DOCX, RTF) and download the example onto your device.

- Complete and endorse the documents.

- Print the template to finalize it manually. Alternatively, employ an online multifunctional PDF editor to efficiently and accurately fill out and endorse your form with a valid signature.

- Redownload your documents again.

- Reuse the same document whenever necessary. Access the My documents tab in your profile to redownload any previously acquired forms.

Form popularity

FAQ

How to form a partnership: 10 steps to success Choose your partners. ... Determine your type of partnership. ... Come up with a name for your partnership. ... Register the partnership. ... Determine tax obligations. ... Apply for an EIN and tax ID numbers. ... Establish a partnership agreement. ... Obtain licenses and permits, if applicable.

How to Prepare a Basic Balance Sheet Determine the Reporting Date and Period. ... Identify Your Assets. ... Identify Your Liabilities. ... Calculate Shareholders' Equity. ... Add Total Liabilities to Total Shareholders' Equity and Compare to Assets.

A partnership is a formal arrangement by two or more parties to manage and operate a business and share its profits. There are several types of partnership arrangements. In particular, in a partnership business, all partners share liabilities and profits equally, while in others, partners may have limited liability.

Partnership accounting is the same as accounting for a proprietorship except there are separate capital and drawing accounts for each partner. The fundamental accounting equation (Assets = Liabilities + Owner's Equity) remains unchanged except that total owners' equity is the sum of the partners' capital accounts.

The entries for a partnership are: Debit each revenue account and credit the income section account for total revenue. Credit each expense account and debit the income section account for total expenses.