Qualified Subchapter S Trust Form For New York

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Trust Which Is A Qualifying Subchapter-S Trust?

Whether for business purposes or for individual matters, everybody has to manage legal situations at some point in their life. Filling out legal papers demands careful attention, beginning from choosing the appropriate form template. For example, if you choose a wrong edition of the Qualified Subchapter S Trust Form For New York, it will be declined once you send it. It is therefore crucial to have a trustworthy source of legal files like US Legal Forms.

If you have to obtain a Qualified Subchapter S Trust Form For New York template, follow these simple steps:

- Get the template you need by utilizing the search field or catalog navigation.

- Check out the form’s information to make sure it fits your case, state, and county.

- Click on the form’s preview to see it.

- If it is the wrong form, return to the search function to find the Qualified Subchapter S Trust Form For New York sample you require.

- Download the file if it matches your requirements.

- If you already have a US Legal Forms profile, simply click Log in to access previously saved documents in My Forms.

- If you do not have an account yet, you may download the form by clicking Buy now.

- Choose the correct pricing option.

- Complete the profile registration form.

- Choose your transaction method: use a bank card or PayPal account.

- Choose the document format you want and download the Qualified Subchapter S Trust Form For New York.

- Once it is downloaded, you are able to complete the form with the help of editing applications or print it and complete it manually.

With a large US Legal Forms catalog at hand, you don’t have to spend time searching for the right template across the web. Make use of the library’s easy navigation to find the right template for any occasion.

Form popularity

FAQ

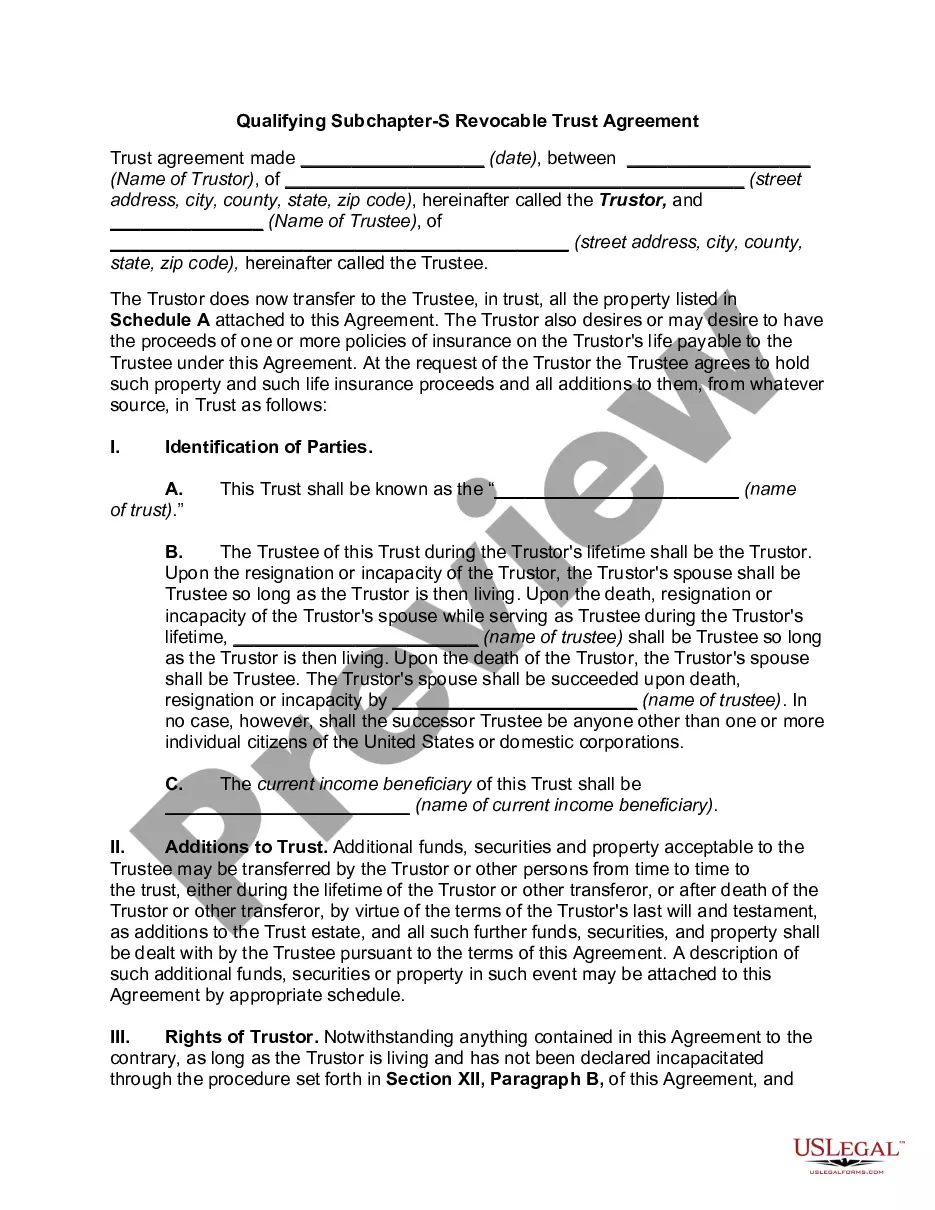

To qualify, the QSST income beneficiary must make a proper and timely election, and the trust must distribute all income to a single individual beneficiary who is a U.S. citizen or resident. If the trust also distributes corpus, it must be allocated to the same income beneficiary.

To qualify as a QSST, the trust must require that all of the net income be distributed to a single beneficiary. While principal of the QSST may also be distributed to the beneficiary in the discretion of the Trustee, the QSST cannot provide for multiple beneficiaries.

To qualify as a QSST, the trust must require that all of the net income be distributed to a single beneficiary. While principal of the QSST may also be distributed to the beneficiary in the discretion of the Trustee, the QSST cannot provide for multiple beneficiaries.

A QSST is a trust with a single income beneficiary who makes an election (which can only be revoked with IRS consent) to be treated as the deemed owner (Sec. 1361(d)(3)).

To form an S Corp in New York, your business must first be a domestic corporation, which means it must be incorporated within the state. It can't be an ineligible corporation, such as an investment company, insurance company, or financial institution that uses the reserve method of accounting for bad debts.