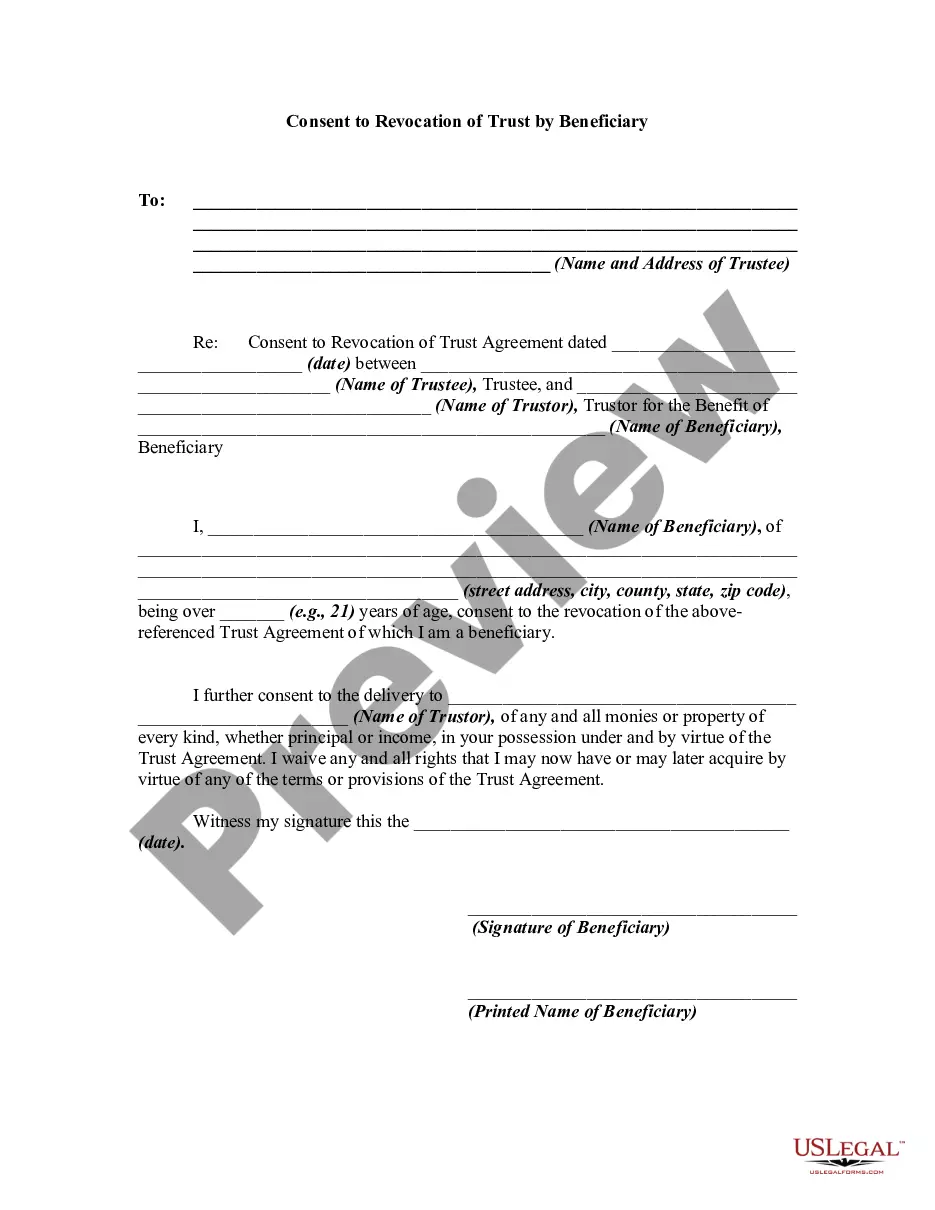

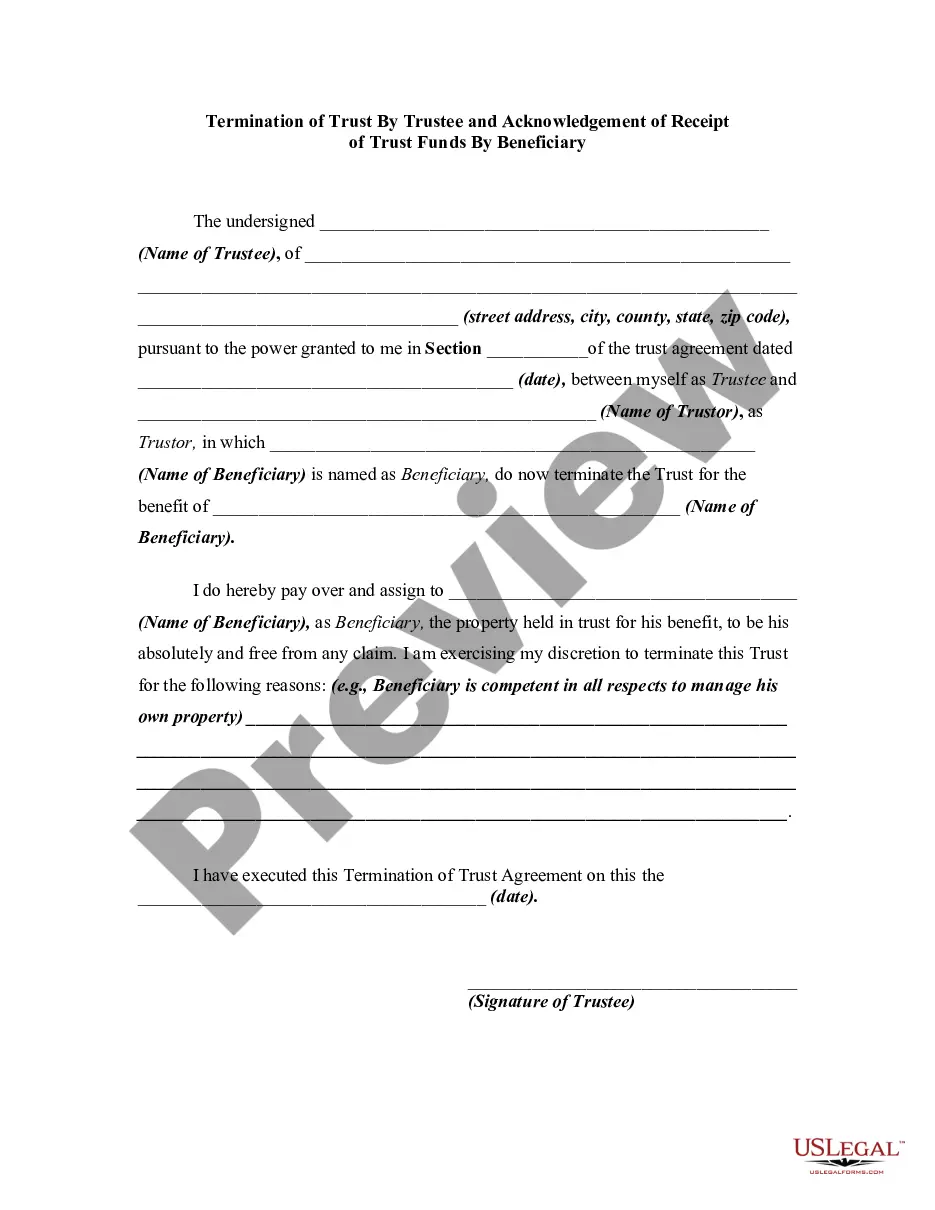

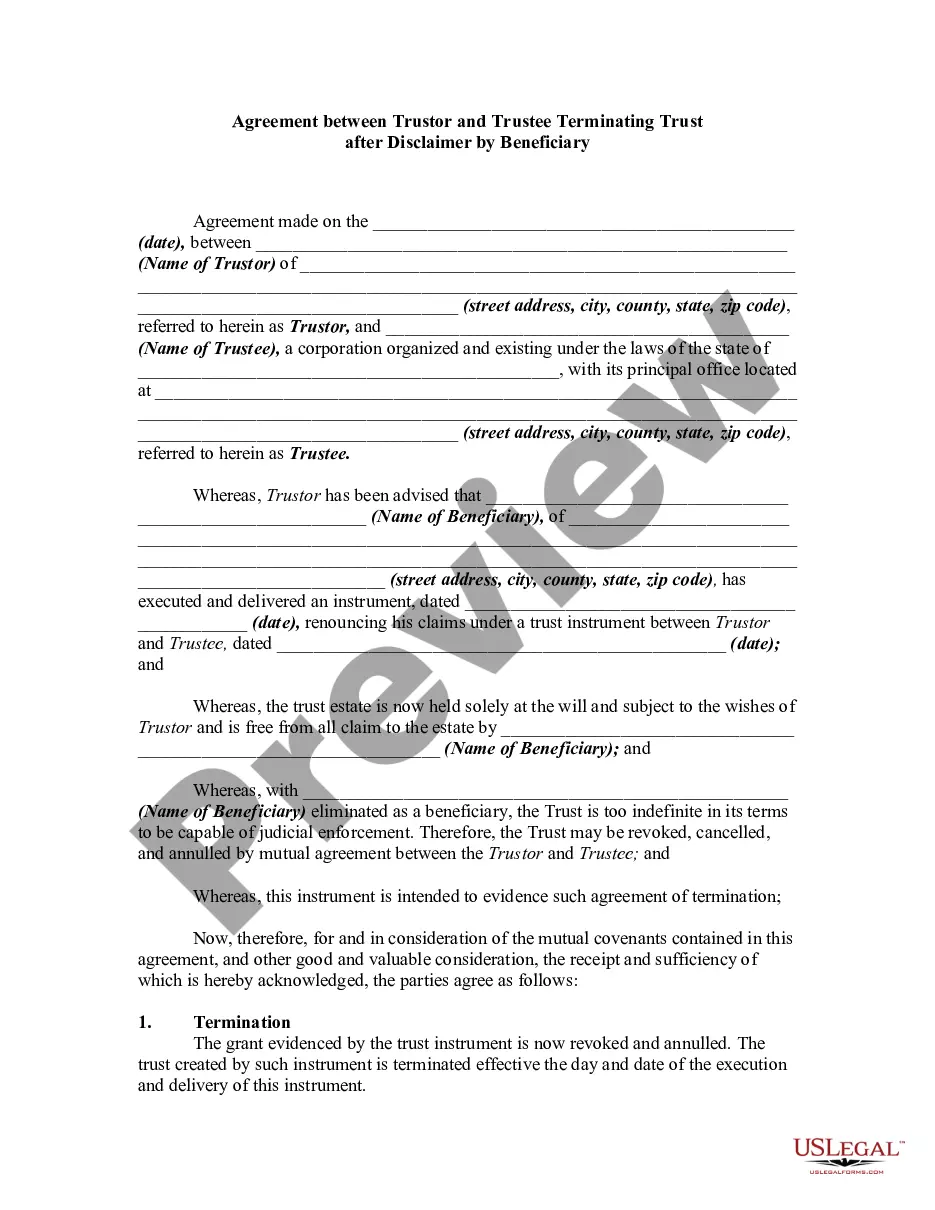

Beneficiary Trustee Trust For Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Termination Of Trust By Trustee?

- If you are already a member of US Legal Forms, simply log in to your account. Verify your subscription's validity and download the necessary form template by clicking the Download button.

- For first-time users, begin by checking the Preview mode and form description to guarantee you select the appropriate document for your needs.

- If the initial form does not meet your requirements, utilize the Search tab to explore other templates. Confirm the right match before proceeding.

- Purchase the form by clicking the Buy Now button and selecting a suitable subscription plan. You will need to create an account to access the full library.

- Complete your purchase by entering your credit card information or opting for PayPal for convenience.

- Download the document onto your device. You can always revisit your saved forms in the My Forms section of your profile.

US Legal Forms empowers individuals and attorneys with a robust selection of over 85,000 fillable legal forms, ensuring you find what you need without tedious searches.

By choosing US Legal Forms, you are taking a significant step toward legal readiness. Start your journey today and streamline your documentation process!

Form popularity

FAQ

The three common types of trust are revocable trusts, irrevocable trusts, and testamentary trusts. A revocable trust allows the grantor to maintain control over the assets and make changes as necessary, whereas an irrevocable trust cannot be easily altered once established. Testamentary trusts are created through a will and become effective upon the death of the grantor. Understanding the differences between these trusts can help you make informed decisions, especially when considering your beneficiary trustee trust for trust.

Yes, you can serve as both the trustee and beneficiary in a trust. This situation often occurs in revocable living trusts, where the grantor retains control over the trust assets while benefiting from them. However, it’s essential to understand the implications of this arrangement, particularly regarding tax liabilities and legal responsibilities. A beneficiary trustee trust for trust can provide flexibility, but it’s advisable to consult with a legal expert to ensure everything is structured correctly.

Form 1041 must be filed by the fiduciary of a trust or estate that meets the gross income threshold. If you have set up a beneficiary trustee trust for trust, the trustee is usually responsible for filing this form. It's essential to understand that even if your trust's income falls below the threshold, filing may still be advisable to keep proper records. Stay informed to make the best decisions regarding your trust obligations.

You are required to file Form 1041 if the estate or trust generates more than $600 in gross income. If you have established a beneficiary trustee trust for trust, this threshold applies to the income it produces. Keep track of all financial activity to ensure compliance with IRS requirements. Filing on time can prevent penalties and ensure smooth management of the trust.

For Form 1041, there is no specific exemption amount akin to estate tax exemptions when it comes to filing. However, a trust or estate must file if its gross income exceeds $600, regardless of any exemptions. If you utilize a beneficiary trustee trust for trust, understanding these income thresholds is essential to meet your tax responsibilities without issues. Your awareness of these details helps in efficient estate management.

The filing threshold for Form 1041 generally depends on the gross income of the estate or trust. For estates or trusts with a gross income that exceeds $600, you must file. If you created a beneficiary trustee trust for trust, you will need to monitor the income generated to ensure compliance. Always consider consulting with a tax professional to confirm your obligations.

An estate tax return is triggered when the total value of assets in an estate exceeds the federal estate tax exemption limit. If you set up a beneficiary trustee trust for trust, the assets within may also count toward this limit. Additionally, the IRS often requires an estate tax return if the decedent made substantial gifts during their lifetime. It's crucial to stay informed about current regulations to avoid surprises.

One of the biggest mistakes parents make when setting up a trust fund is failing to communicate their intentions clearly with their heirs. Without open discussions about the trust, beneficiaries may feel confused or misinformed about their roles. Additionally, not regularly reviewing or updating the trust can lead to outdated provisions. To ensure a smooth process, consider utilizing resources like uslegalforms for reliable guidance in your beneficiary trustee trust for trust.

Yes, it is entirely possible to be both a trustee and a beneficiary of a trust. This dual role can offer personal insight while managing the trust. However, it is vital to ensure transparency and fairness in the administration of the trust. When setting up your beneficiary trustee trust for trust, consider consulting experts to help navigate this structure.

Yes, you can serve as both trustee and beneficiary of a trust simultaneously. This arrangement can be practical if you are managing your own trust and wish to benefit from it as well. However, be mindful of potential conflicts of interest that may arise. Establishing a solid framework for management can help your beneficiary trustee trust for trust succeed.