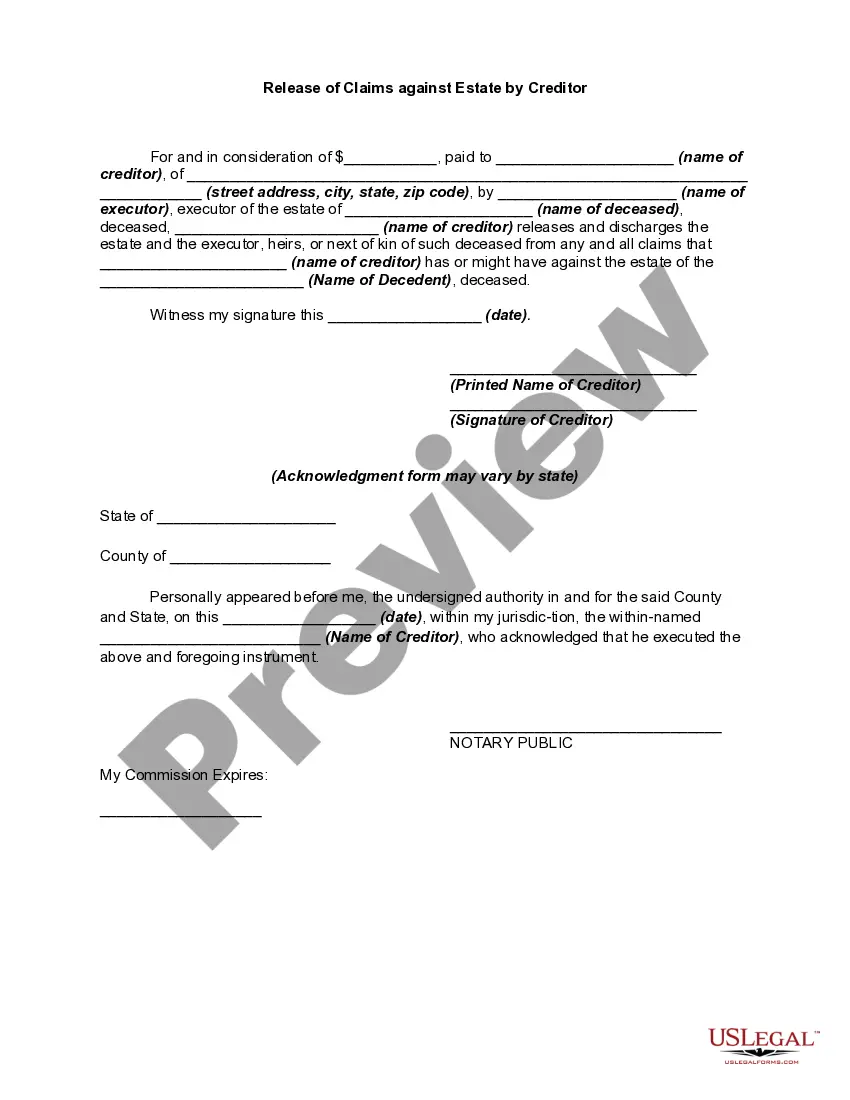

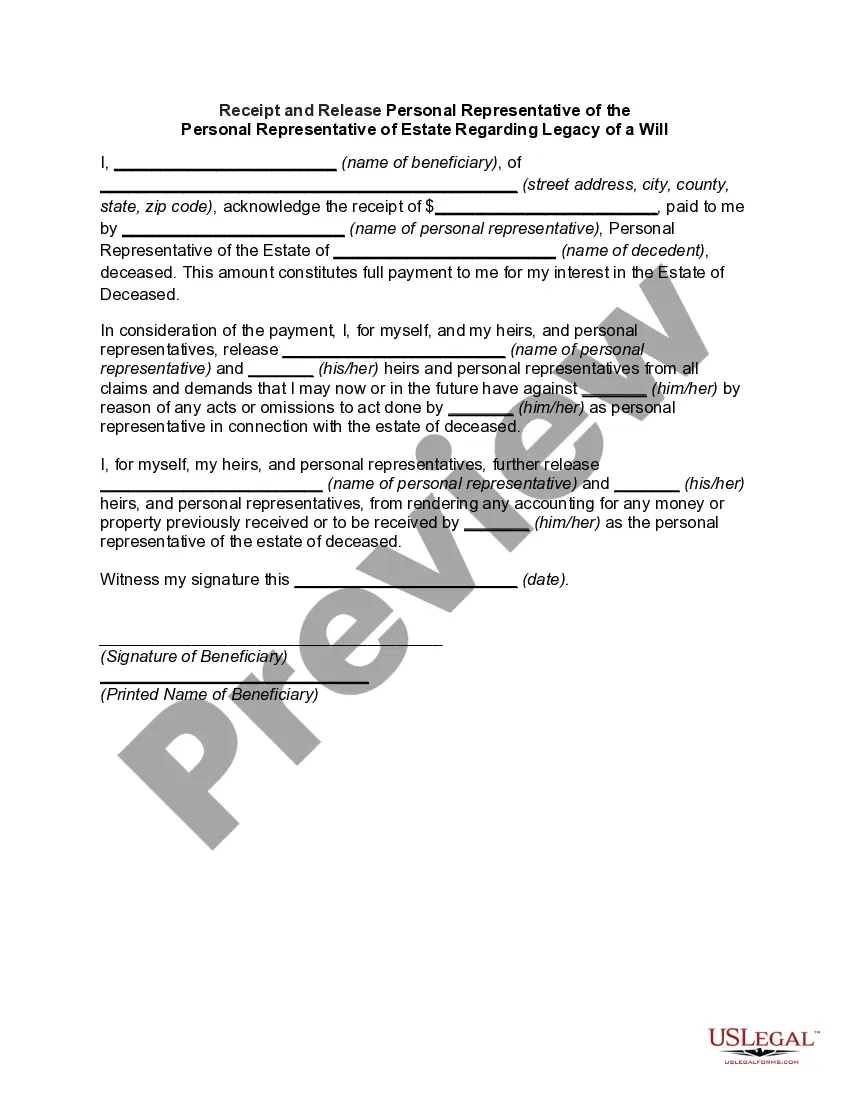

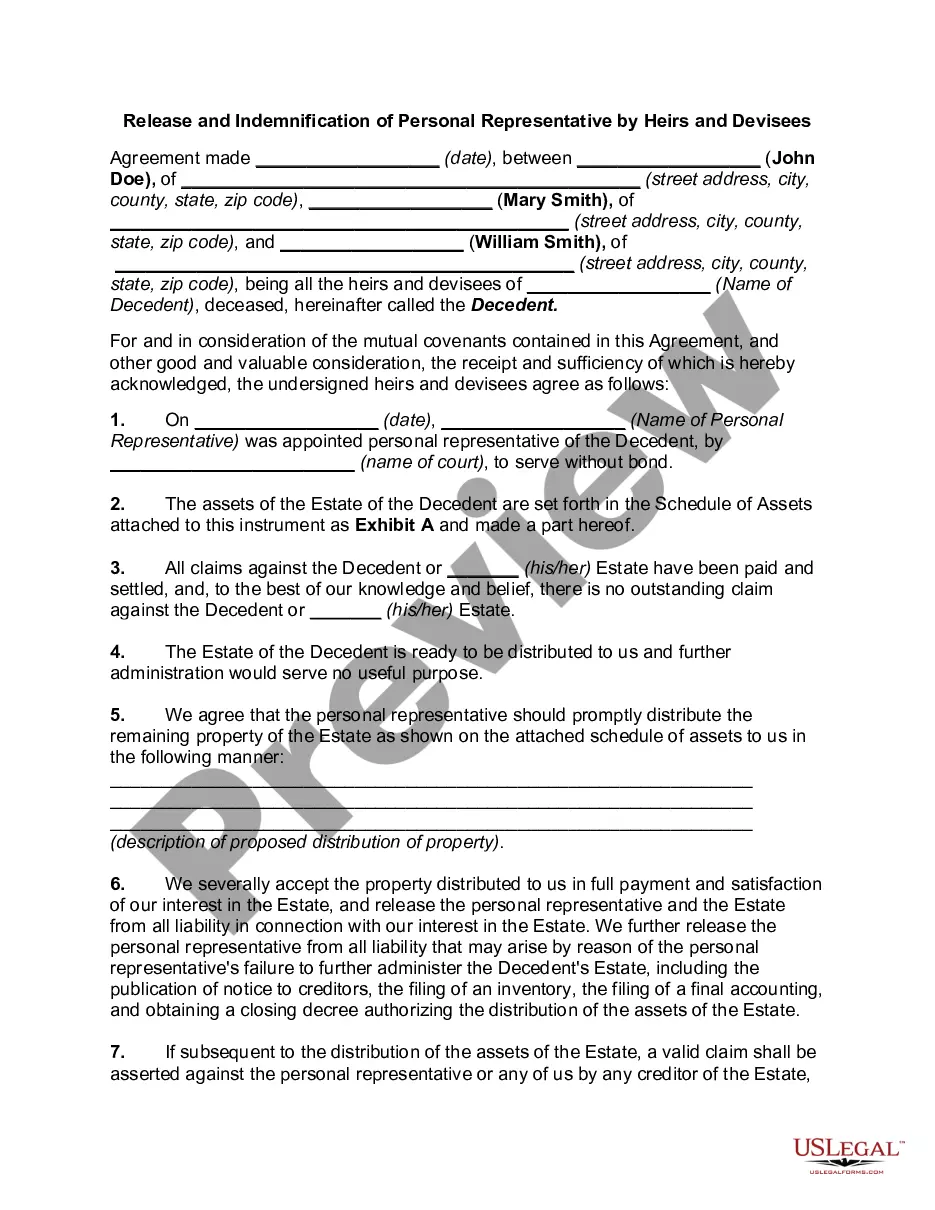

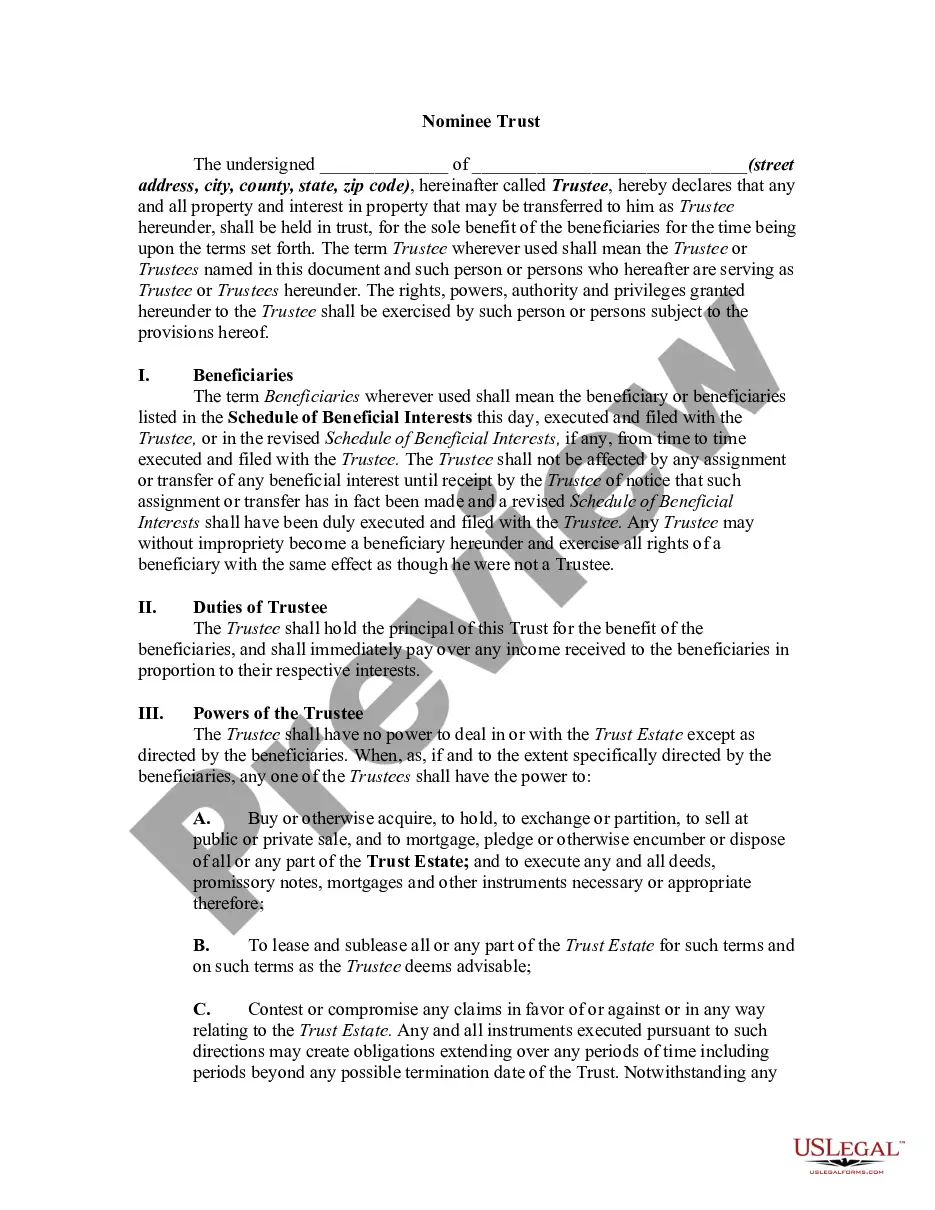

Name Executor Estate Without Bond

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Release And Exoneration Of Executor On Distribution To Beneficiary Of Will And Waiver Of Citation Of Final Settlement?

Locating a preferred location to obtain the most up-to-date and pertinent legal templates is a significant part of navigating bureaucracy.

Securing the appropriate legal documents requires accuracy and meticulousness, which is why it is crucial to acquire samples of Name Executor Estate Without Bond exclusively from reliable sources, such as US Legal Forms. An incorrect template could squander your time and prolong the matter at hand. With US Legal Forms, you have minimal concerns. You can access and review all the details regarding the document’s applicability and significance for your circumstances and in your jurisdiction.

Eliminate the difficulties that come with your legal documentation. Browse the extensive US Legal Forms collection to find legal templates, verify their relevance to your circumstances, and download them instantly.

- Utilize the catalog navigation or search option to locate your template.

- Examine the form’s description to ensure it aligns with the stipulations of your state and locale.

- Check the form preview, if available, to confirm that the document is indeed the one you seek.

- Return to the search to find the appropriate template if the Name Executor Estate Without Bond does not suit your requirements.

- Once confident about the form’s applicability, download it.

- If you are a registered user, click Log in to verify and access your selected templates in My documents.

- If you don't yet have an account, click Buy now to acquire the template.

- Select the pricing option that meets your needs.

- Proceed to the registration to finalize your purchase.

- Complete your purchase by selecting a payment method (credit card or PayPal).

- Choose the document format for downloading Name Executor Estate Without Bond.

- After obtaining the form on your device, you can modify it with the editor or print it and fill it out by hand.

Form popularity

FAQ

The 3-year clawback rule allows the IRS to reclaim certain gifts made by a deceased person within three years of their passing if the estate exceeds the exemption limit. If you are responsible for managing the estate as an executor, understanding this rule helps in effectively strategizing the estate's distribution. Proper guidance can ensure that you handle these matters smoothly, especially when naming an executor estate without bond.

An executor bond is a type of insurance that protects the estate’s assets from damage due to the executor's actions. This bond is often required by the court to ensure the executor acts in the best interest of the beneficiaries. If you want to name an executor for your estate without bond, you may consider the individual's integrity crucial.

Today's mortgage rates in Utah are 7.723% for a 30-year fixed, 6.784% for a 15-year fixed, and 8.126% for a 5-year adjustable-rate mortgage (ARM). Getting ready to buy a home? We'll find you a highly rated lender in just a few minutes. Enter your ZIP code to get started on a personalized lender match.

In Utah, the average cost of mortgage payments is $1,261 per month, but the actual cost for you can be different based on your circumstance.

Mortgage Lending in Utah Utah's mortgage regulation structure is complex because two different agencies regulate different activities. Brokering and retail origination of closed-end residential first mortgages are activities primarily regulated by the Utah Division of Real Estate (DRE).

How to Write a Mortgage Deed Step 1 ? Fill In the Effective Date. ... Step 2 ? Enter Borrower and Lender Details. ... Step 3 ? Write Loan Information. ... Step 4 ? Fill In Property Details. ... Step 5 ? Identify Assigned Rents. ... Step 6 ? Enter Acceleration Upon Default. ... Step 7 ? Choose the Power of Sale Option.

Utah is known as a Trust Deed and Promissory Note state. There are references to a foreclosure being allowed under the law, typically in a Contract for Deed transaction but this is certainly not the standard.

Utah home buyer stats Average Home Sale Price in Utah1$479,368Minimum Down Payment in Utah (3%)$14,38120% Down Payment in Utah$95,874Average Credit Score in Utah2730Maximum Utah Home Buyer Grant3UHC second mortgage: "borrow your entire minimum required down payment plus all or a portion of your closing costs"

Utah conventional mortgages: To qualify for a conventional mortgage, you'll need a minimum credit score of 620 and a debt-to-income (DTI) ratio no more than 45 percent. If you make a down payment of less than 20 percent, you'll need to pay private mortgage insurance (PMI) premiums, as well.