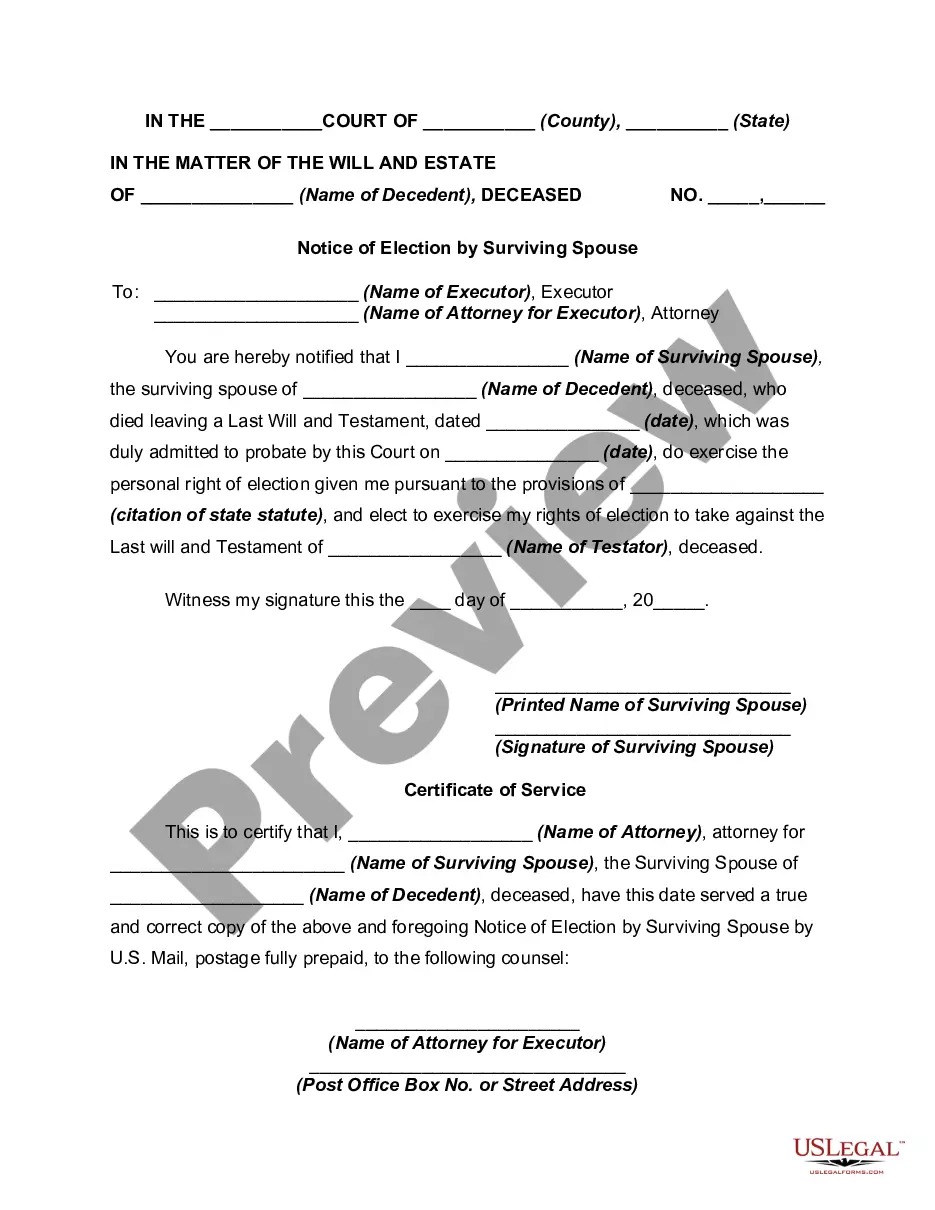

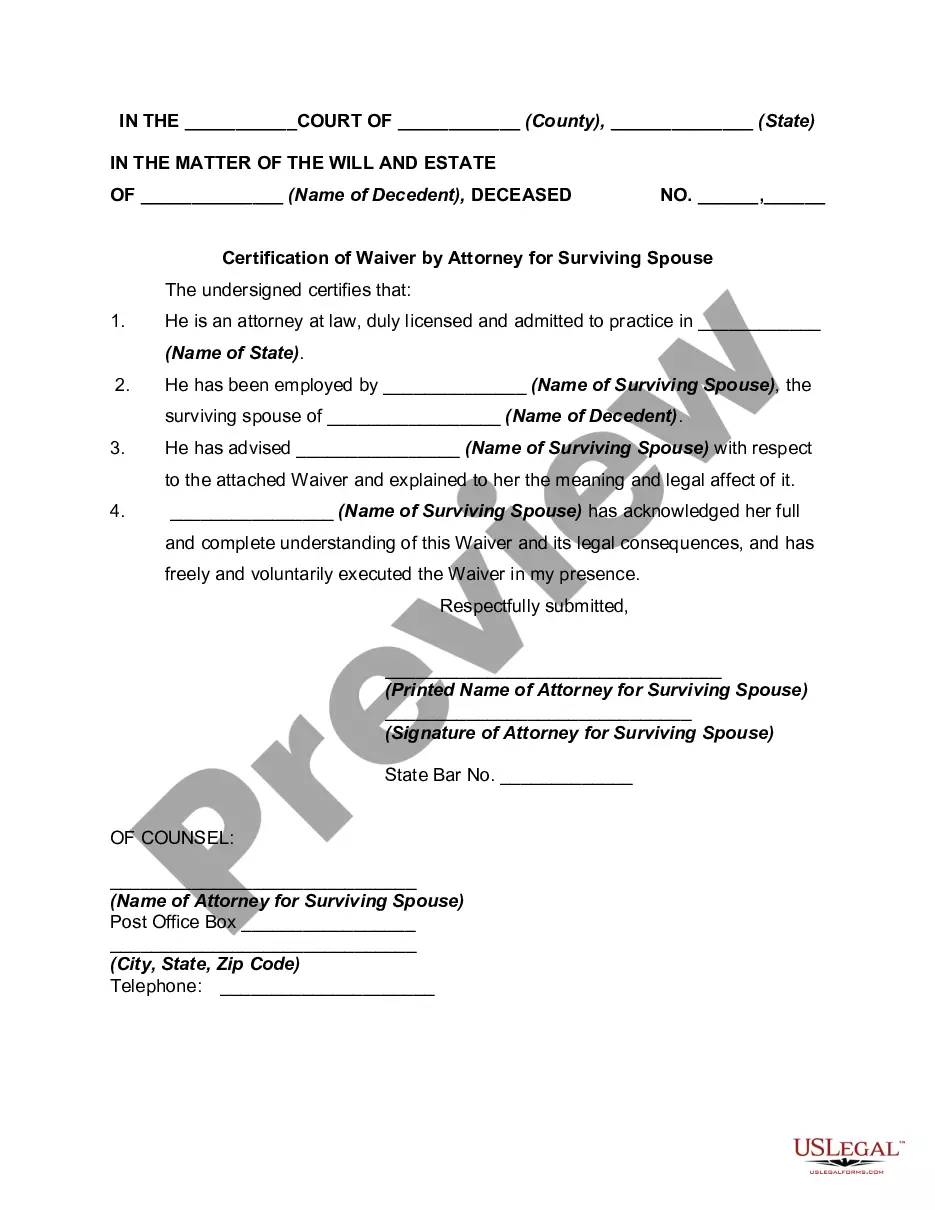

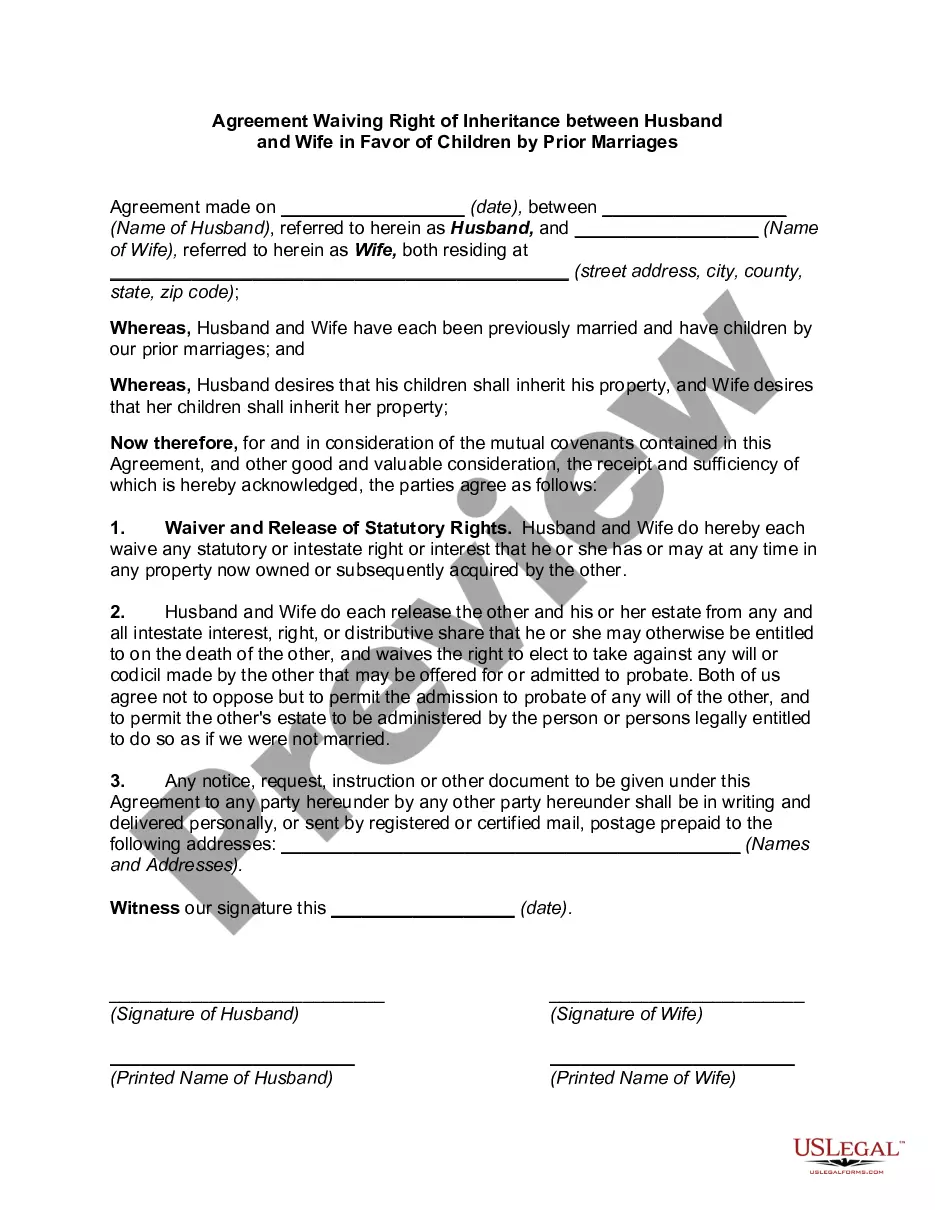

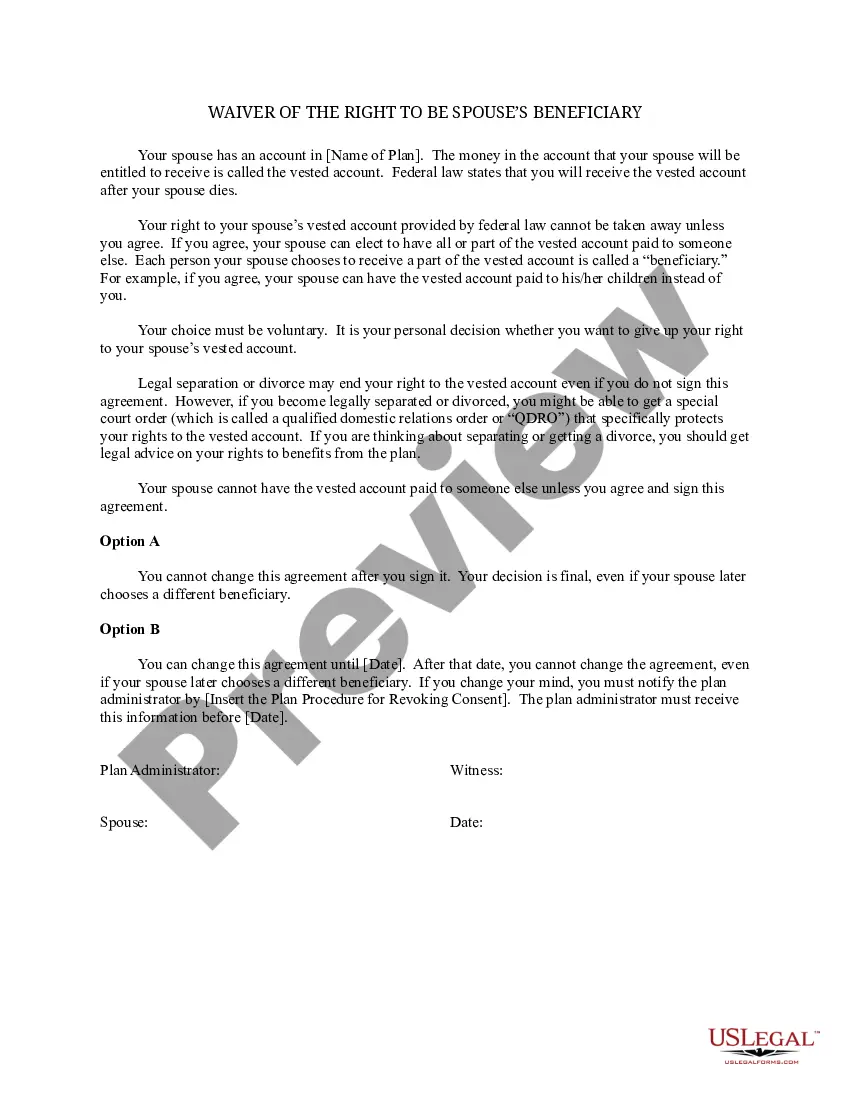

Spouse Surviving State For Tax Purposes

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Waiver Of Right To Election By Spouse?

The Surviving Spouse State For Tax Purposes you see on this page is a reusable legal template crafted by professional attorneys in accordance with federal and local statutes and regulations.

For over 25 years, US Legal Forms has supplied individuals, organizations, and legal professionals with more than 85,000 validated, state-specific documents for any business and personal circumstance. It’s the fastest, simplest, and most dependable method to acquire the paperwork you require, as the service assures the utmost level of data security and anti-malware safeguards.

Select the format you prefer for your Surviving Spouse State For Tax Purposes (PDF, Word, RTF) and store the sample on your device. Complete and sign the document. Print out the template to finish it by hand. Alternatively, use an online multifunctional PDF editor to swiftly and accurately fill out and sign your form with a legally-binding electronic signature. Download your paperwork again. Use the same document again whenever necessary. Access the My documents tab in your profile to redownload any previously saved forms. Enroll in US Legal Forms to have verified legal templates for all of life’s situations at your fingertips.

- Search for the document you need and examine it.

- Look through the file you searched and preview it or review the form description to confirm it fits your requirements. If it doesn’t, utilize the search option to find the correct one. Click Buy Now when you have identified the template you need.

- Subscribe and Log In.

- Select the pricing plan that works for you and create an account. Use PayPal or a credit card to make a quick payment. If you already have an account, Log In and verify your subscription to proceed.

- Obtain the fillable template.

Form popularity

FAQ

To qualify, you must meet these requirements: You qualified for married filing jointly with your spouse for the year he or she died. ... You didn't remarry before the close of the tax year in which your spouse died. You have a child, stepchild, or adopted child you claim as your dependent.

The IRS considers the surviving spouse married for the full year their spouse died if they don't remarry during that year. The surviving spouse is eligible to use filing status "married filing jointly" or "married filing separately." The same tax deadlines apply for final returns.

Using the qualified widow(er) status allows the surviving spouse to file taxes as if they were still married, despite the fact that their partner is deceased. You can file taxes as a qualified widow(er) for the year your spouse died, as well as two years following their death.

Qualifying widow(er) with dependent child The individual can use this option if they were able to file a joint return during the year their spouse died, they didn't remarry, they have a dependent child living in the house all year, and they paid more than half the cost of maintaining the home.

To file the state returns as separate, you will need a federal return prepared as filing married-separate. So, you will need two married-separate federal returns for each state return and then a married-joint return for the federal. You file the federal and both state returns separately.