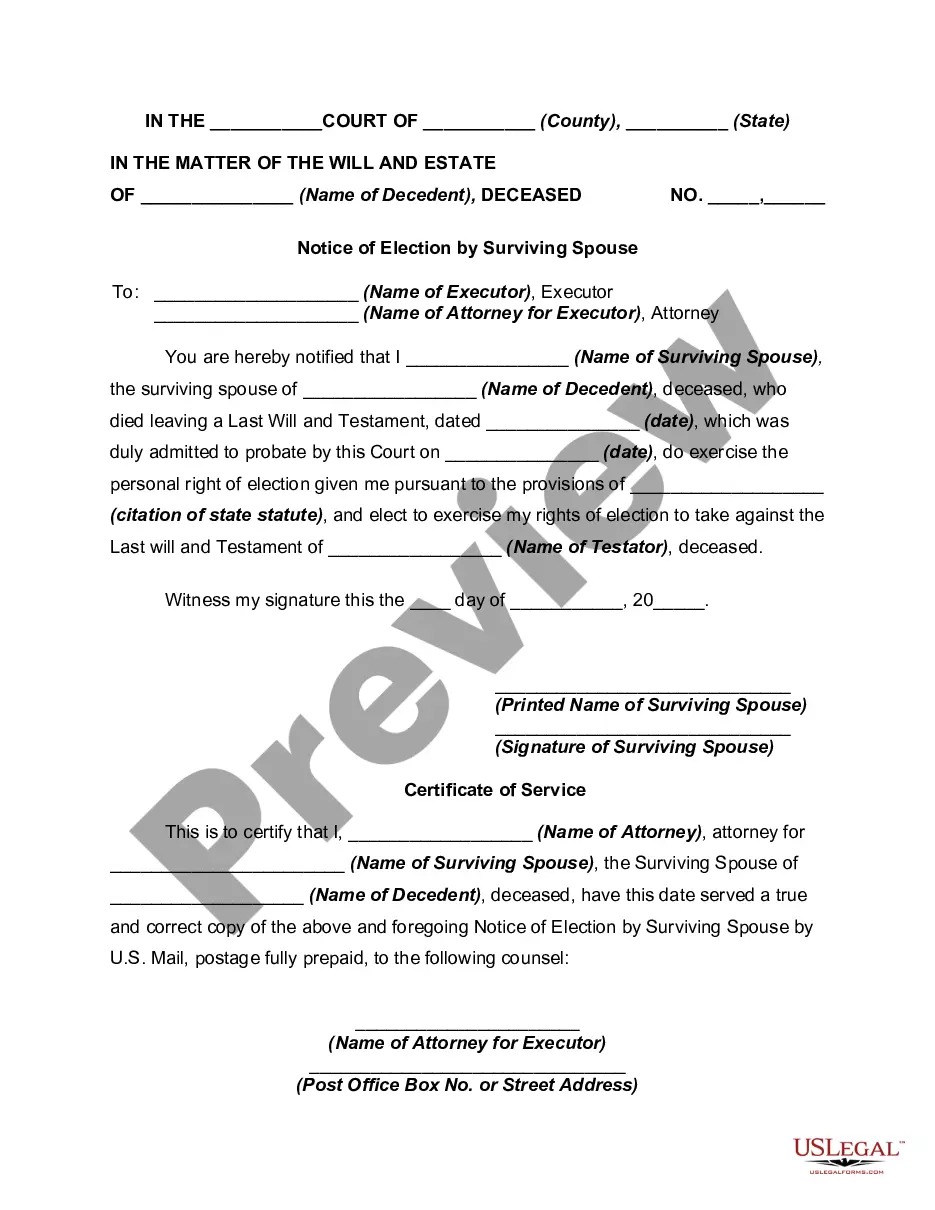

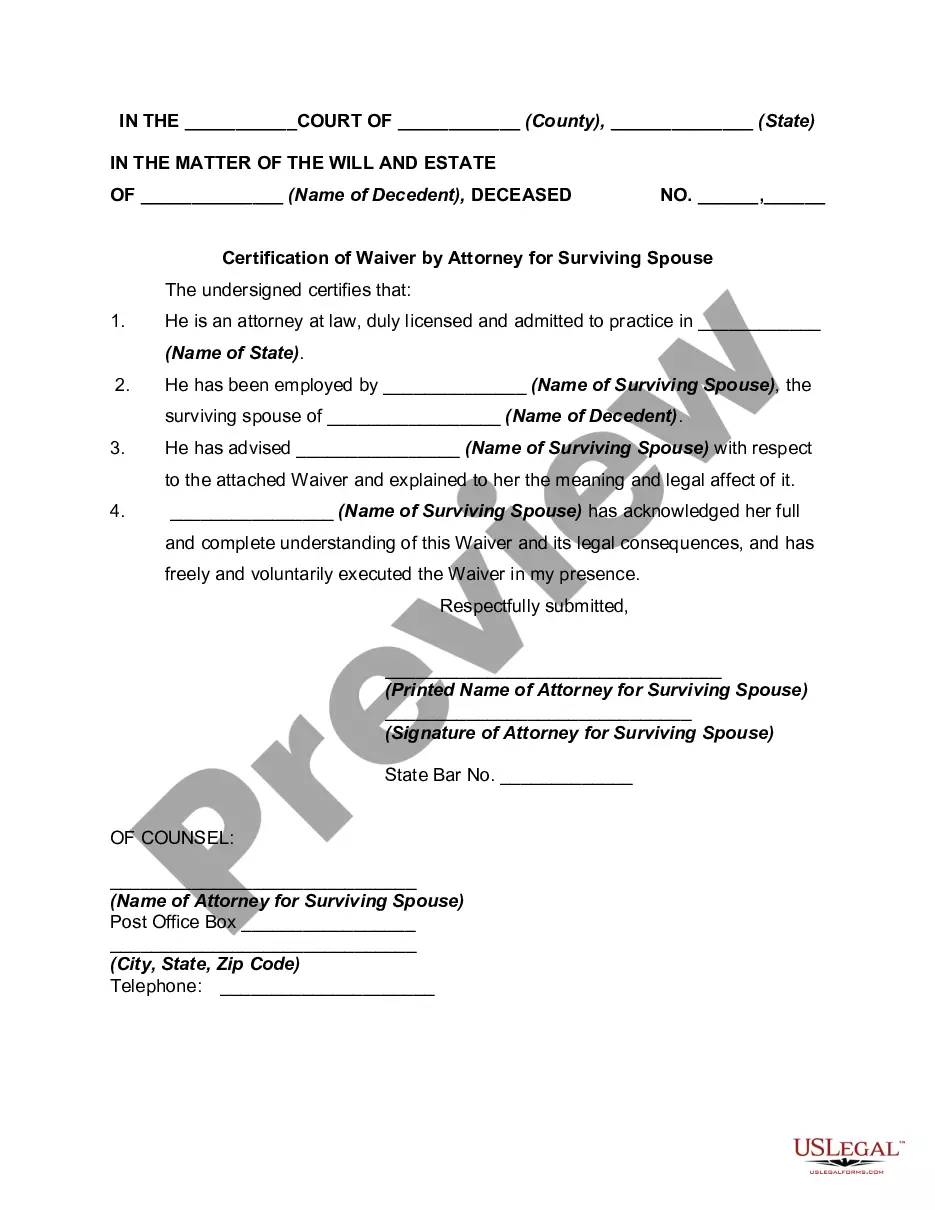

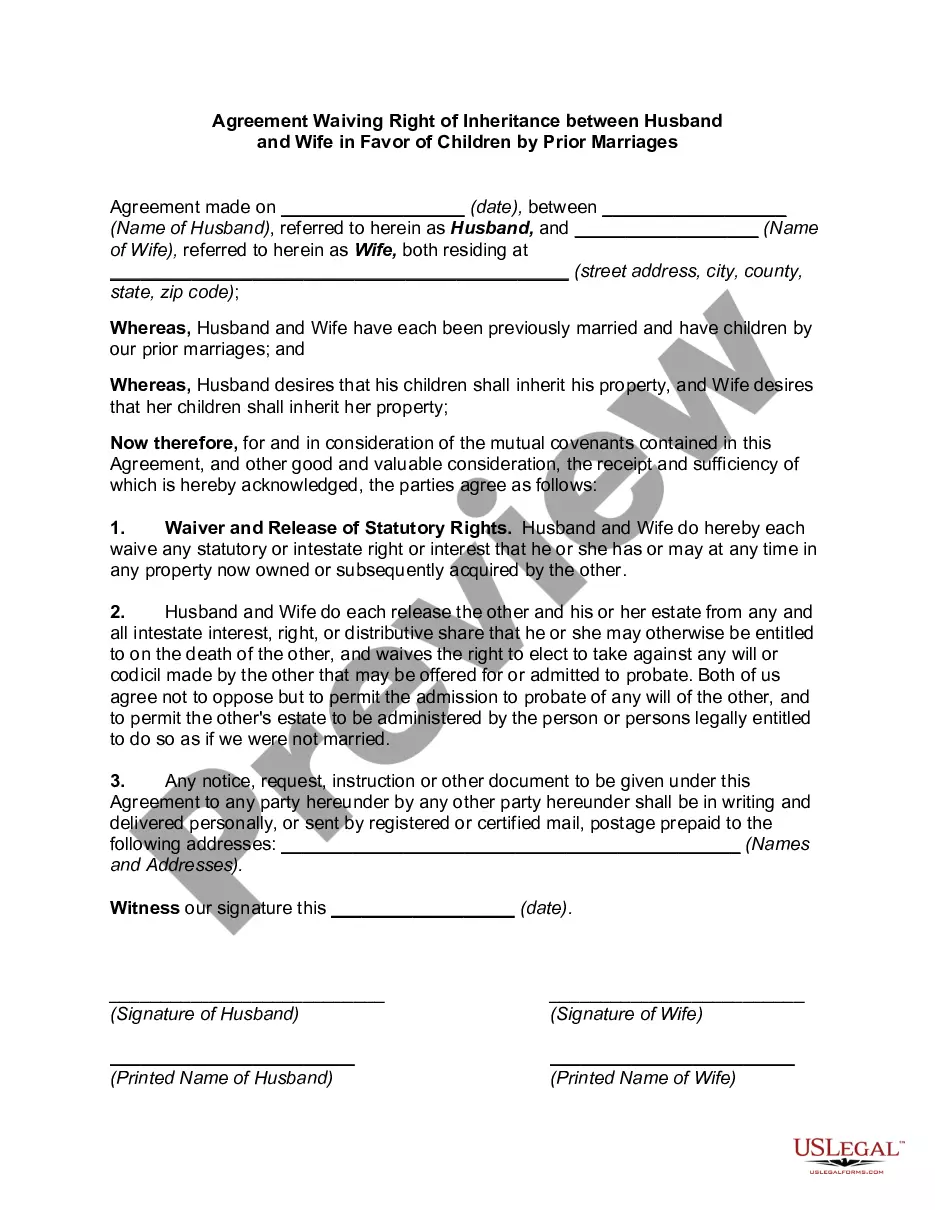

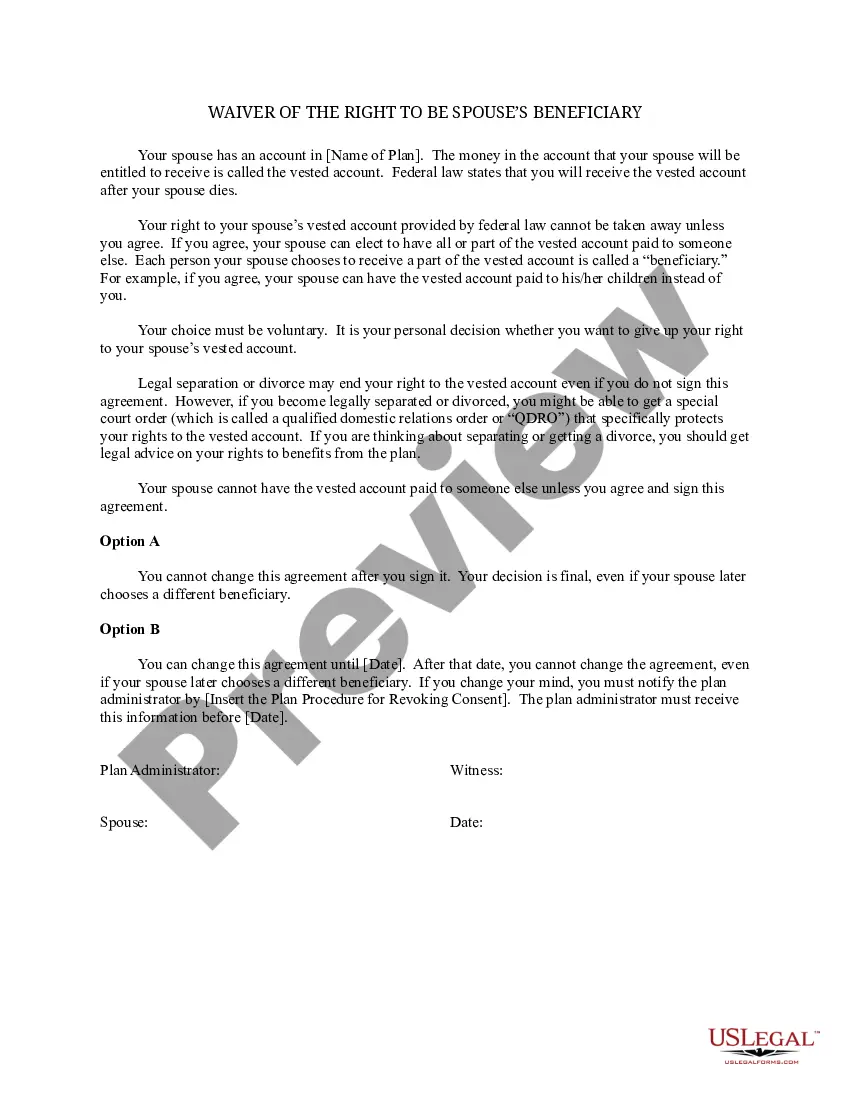

Spouse Elective Shares Foreign

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Waiver Of Right To Election By Spouse?

Handling legal documents can be daunting, even for experienced professionals.

If you're looking for Spouse Elective Shares Foreign and lack the time to find the right and current version, the process can be anxiety-inducing.

Tap into a valuable resource pool of articles, guides, handbooks, and tools relevant to your circumstances and demands.

Conserve time and effort in locating the documents you require, and utilize US Legal Forms’ sophisticated search and Preview feature to find Spouse Elective Shares Foreign and obtain it.

Leverage the US Legal Forms online library, supported by 25 years of expertise and reliability. Streamline your routine document management into a seamless and user-friendly experience today.

- If you have a membership, Log In to your US Legal Forms account, search for the document, and retrieve it.

- Check your My documents section to see the documents you've saved and organize your folders as needed.

- If this is your first time using US Legal Forms, create a free account to gain unlimited access to all the library's benefits.

- Follow these steps after acquiring the form you require.

- 1. Confirm it is the correct form by previewing it and examining its details.

- Access state- or county-specific legal and organizational forms.

- US Legal Forms meets any needs you may have, from personal to corporate documents, all in one location.

- Utilize advanced tools to complete and oversee your Spouse Elective Shares Foreign.

Form popularity

FAQ

In most states, the elective share is between one-third and one-half of all the property in the estate, although many states require the marriage to have lasted a certain number of years for the elective share to be claimed, or adjust the share based on the length of the marriage, and the presence of minor children.

It does not matter where the non-citizen spouse lives. Annual gifts to non-citizen spouse are limited to $175,000.00. But given the high federal exemption, the federal estate and gift tax only becomes an issue for US citizens if they leave more than $12.92 million in assets.

Tip: A non-citizen spouse can inherit from a U.S. citizen spouse free of estate tax if the U.S. citizen creates a special trust called a qualified domestic trust (QDOT). The U.S. citizen can leave property to the trust, instead of directly to the non-citizen spouse.

In addition to the withholding requirement, naming a beneficiary who resides in a foreign country may allow the foreign country to tax the property and accounts of the trust. In most cases, a foreign person is subject to US tax on its US source income.

Depending on the facts and circumstances, this would either be half or all of the probate estate. Unlike an elective share, the inheritance to a pretermitted spouse is made up exclusively of probate assets.