Distribution Estate Form For Real

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Petition For Partial And Early Distribution Of Estate?

The Distribution Estate Form For Real that you observe on this page is a versatile legal document created by expert attorneys in accordance with federal and local laws and regulations.

For over 25 years, US Legal Forms has supplied individuals, enterprises, and legal practitioners with more than 85,000 authenticated, state-specific forms for any business and personal circumstance. It’s the fastest, simplest, and most dependable method to acquire the documents you require, as the service ensures bank-level data security and anti-malware safeguards.

Select the format you prefer for your Distribution Estate Form For Real (PDF, Word, RTF) and save the document on your device. Fill out and sign the documentation. Print the template to fill it out by hand. Alternatively, use an online multifunctional PDF editor to quickly and accurately complete and sign your form with a legally-binding electronic signature. Download your documentation once more. Use the same document again whenever necessary. Access the My documents tab in your profile to redownload any previously acquired forms. Subscribe to US Legal Forms to have verified legal templates for all of life’s situations readily available.

- Look for the document you require and review it.

- Browse through the sample you searched and preview it or read the form description to ensure it meets your needs. If it doesn’t, utilize the search bar to find the correct one. Click Buy Now when you have found the template you need.

- Subscribe and Log In.

- Choose the pricing plan that best fits you and create an account. Use PayPal or a credit card for a swift payment. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the editable template.

Form popularity

FAQ

The administrator, executor, or beneficiary must: File a final tax return. File any past due returns. Pay any tax due.

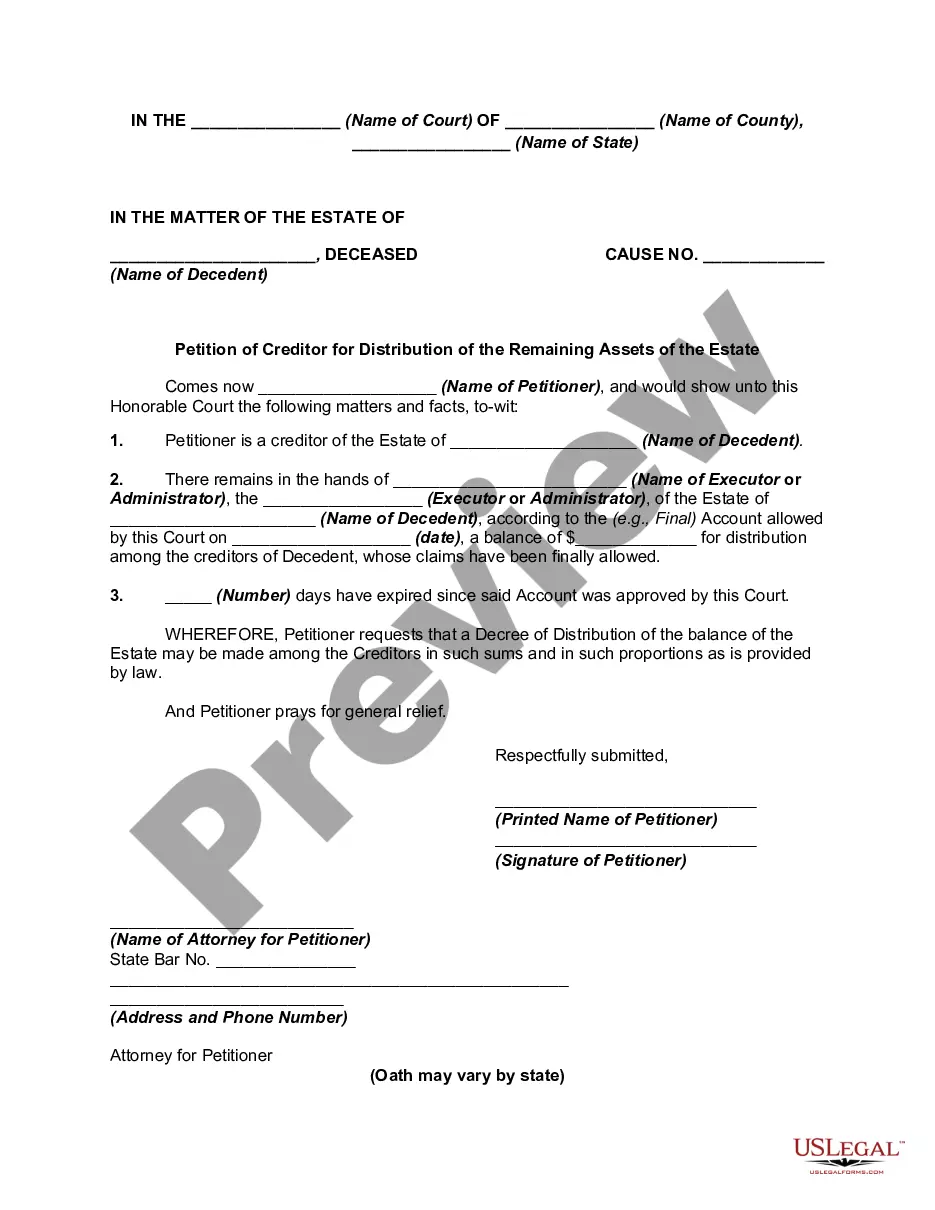

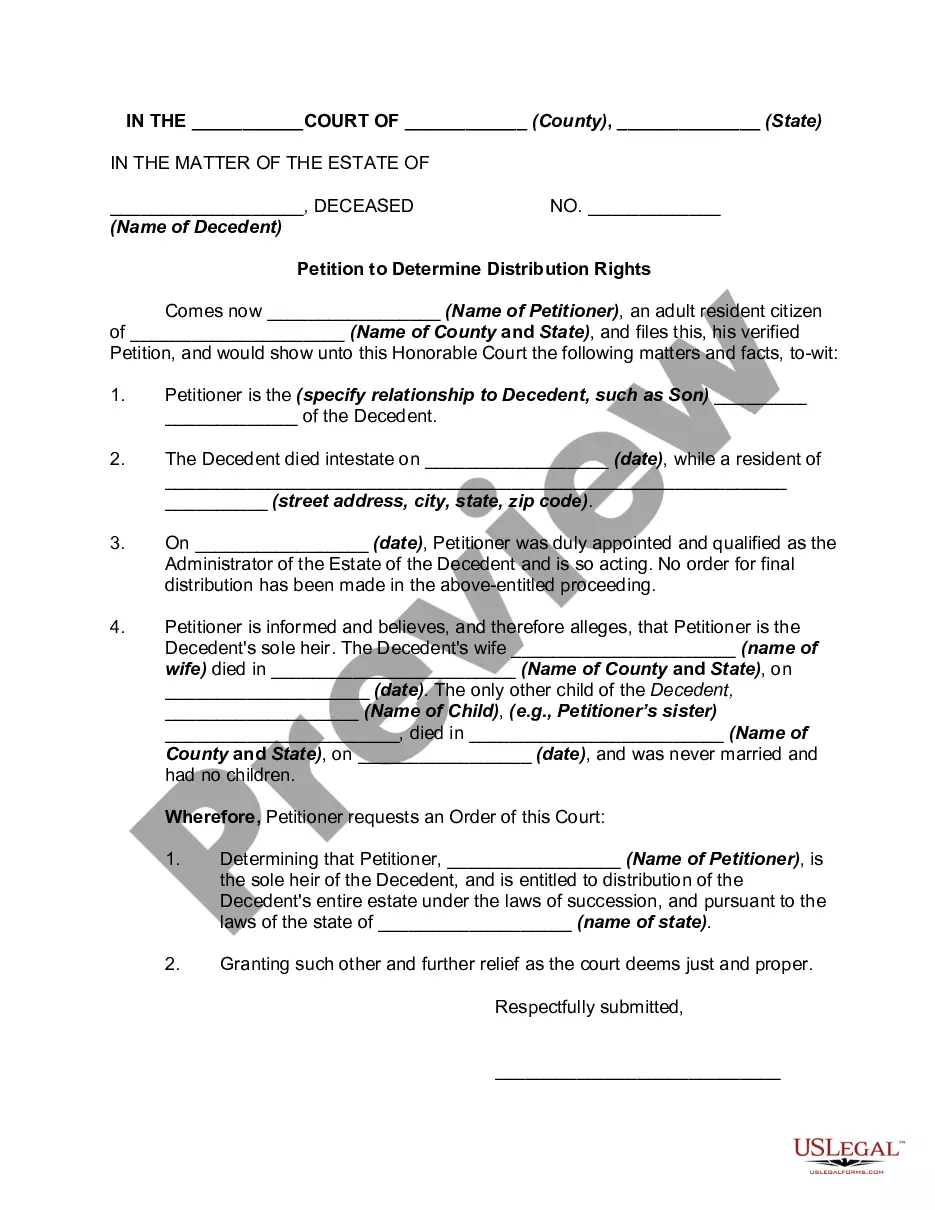

This is when courts transfer the ownership of assets to beneficiaries or heirs. The final distribution only occurs when the estate is settled, meaning all creditors and taxes have been paid, all disputes have been resolved, and the judge gives final approval.

When a portion of a beneficiary's distribution from a trust or the entirety of it originates from the trust's interest income, they generally will be required to pay income taxes on it, unless the trust has already paid the income tax.

Report income distributions to beneficiaries and to the IRS on Schedule K-1 (Form 1041). For calendar year estates and trusts, file Form 1041 and Schedule(s) K-1 on or before April 15 of the following year.

Income required to be distributed to the beneficiaries is taxable to them regardless if it is distributed during the year. The trust or estate receives a deduction for distributions of income made to the beneficiaries. The distribution deduction is limited to the distributable net income (DNI) of the trust or estate.