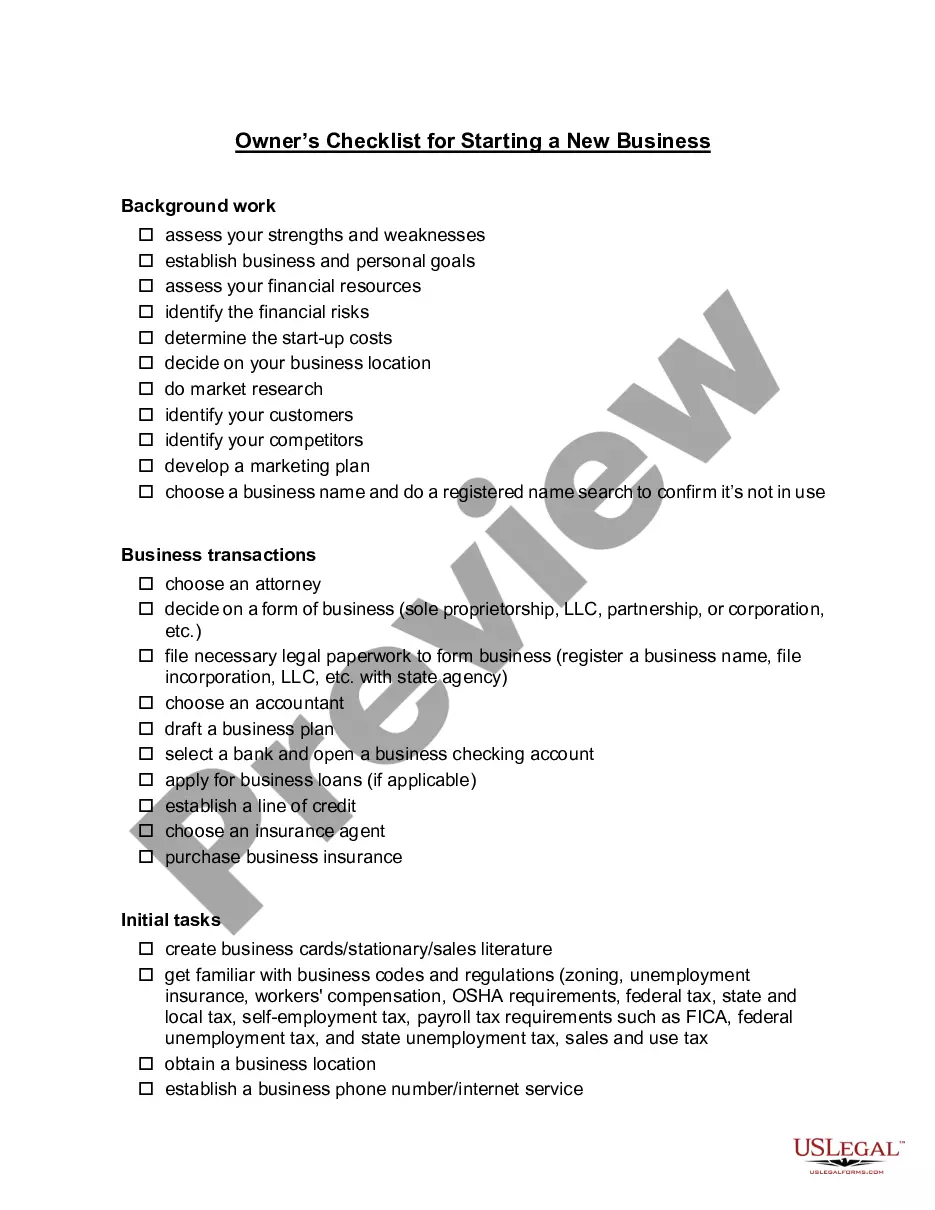

Business Checklist For Taxes

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Business Deductions Checklist?

Managing legal documents and procedures can be a lengthy addition to your schedule.

Business Checklist For Taxes and similar forms typically necessitate that you locate them and determine the optimal method to complete them accurately.

Consequently, whether you are attending to financial, legal, or personal issues, utilizing a thorough and user-friendly online directory of forms when required will greatly assist.

US Legal Forms is the leading online resource of legal templates, featuring over 85,000 state-specific forms and various tools that will aid you in finishing your documentation swiftly.

Simply Log In to your account, locate Business Checklist For Taxes, and get it immediately within the My documents tab. You may also access previously stored forms.

- Explore the collection of relevant documents accessible to you with just one click.

- US Legal Forms offers state- and county-specific forms available at any time for downloading.

- Protect your document management processes with a premium service that allows you to prepare any form in minutes without additional or hidden fees.

Form popularity

FAQ

In order to have a quitclaim deed admitted to record in Vermont, it should be signed by the party granting the real estate, acknowledged by the same, and recorded in the clerk's office in the town where the property is situated.

A Contract for Deed is a way to buy a house that doesn't involve a bank. The seller finances the property for the buyer. The buyer moves in when the contract is signed. The buyer pays the seller monthly payments that go towards payment for the home.

You should record the Contract for Deed in the county where the property is located as soon as possible. Recording the contract helps protect you. You should still record the contract even if it states it ?cannot? be recorded. Bring the signed contract to the county courthouse to officially record the contract.

Under a contract for deed, the grantor retains the legal title to the real property until the purchase price is paid in full and the other terms of the contract are completed. Before a contract is paid off, the grantor (vendor) may choose to assign its contract rights to a third party.

A major drawback of a contract for deed for buyers is that the seller retains the legal title to the property until the payment plan is completed. On one hand, this means that they're responsible for things like property taxes. On the other hand, the buyer lacks security and rights to their home.

Other advantages include: no appraisal required, wider range of buyers, possible profit on financing, and quicker settlement. The biggest disadvantage of a contract for deed for a seller is that the property won?t be out of your name for many years. This quite possibly won?t suit your investment strategy.

In a contract for deed, the purchase of property is financed by the seller rather than a third-party lender such as a commercial bank or credit union. The arrangement can benefit buyers and sellers by extending credit to homebuyers who would not otherwise qualify for a loan.