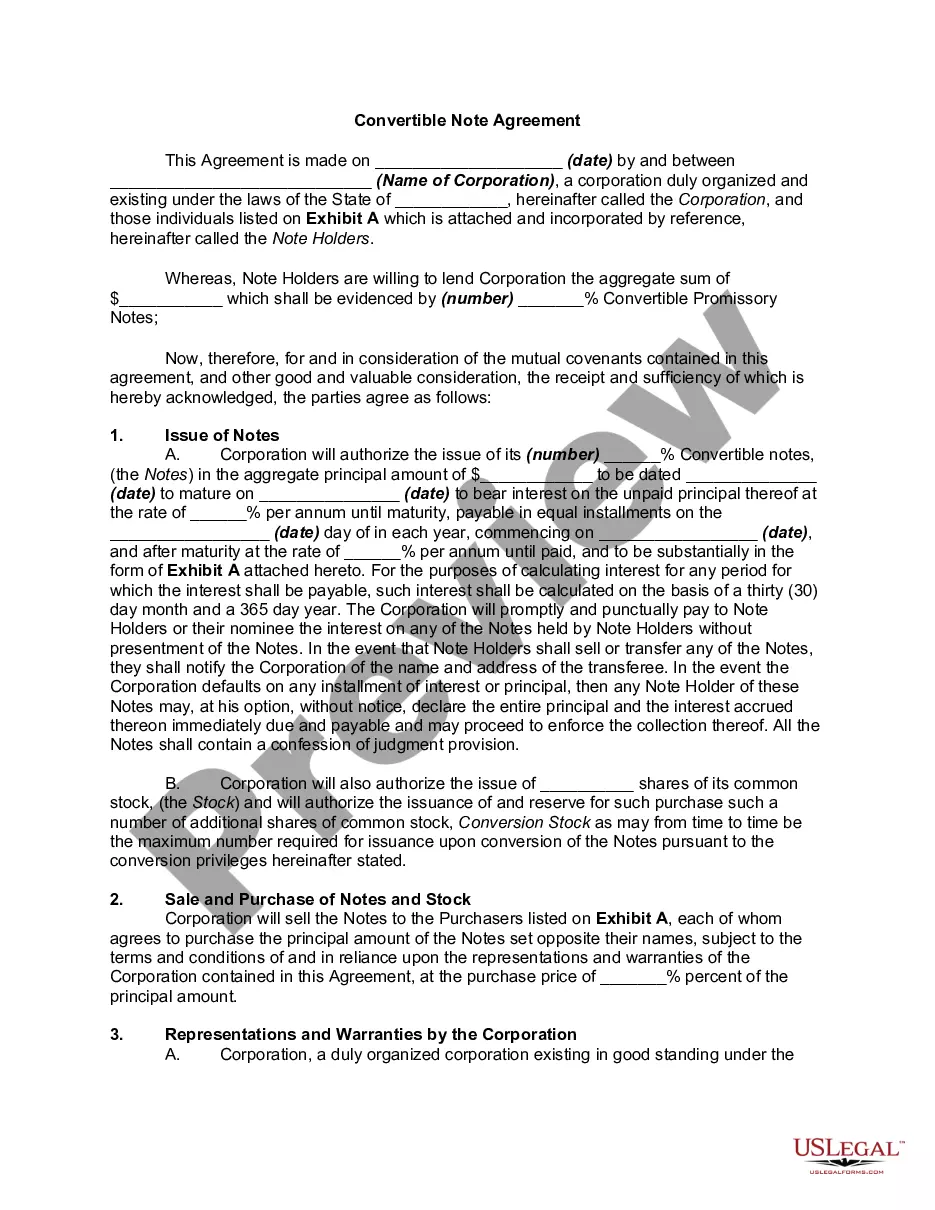

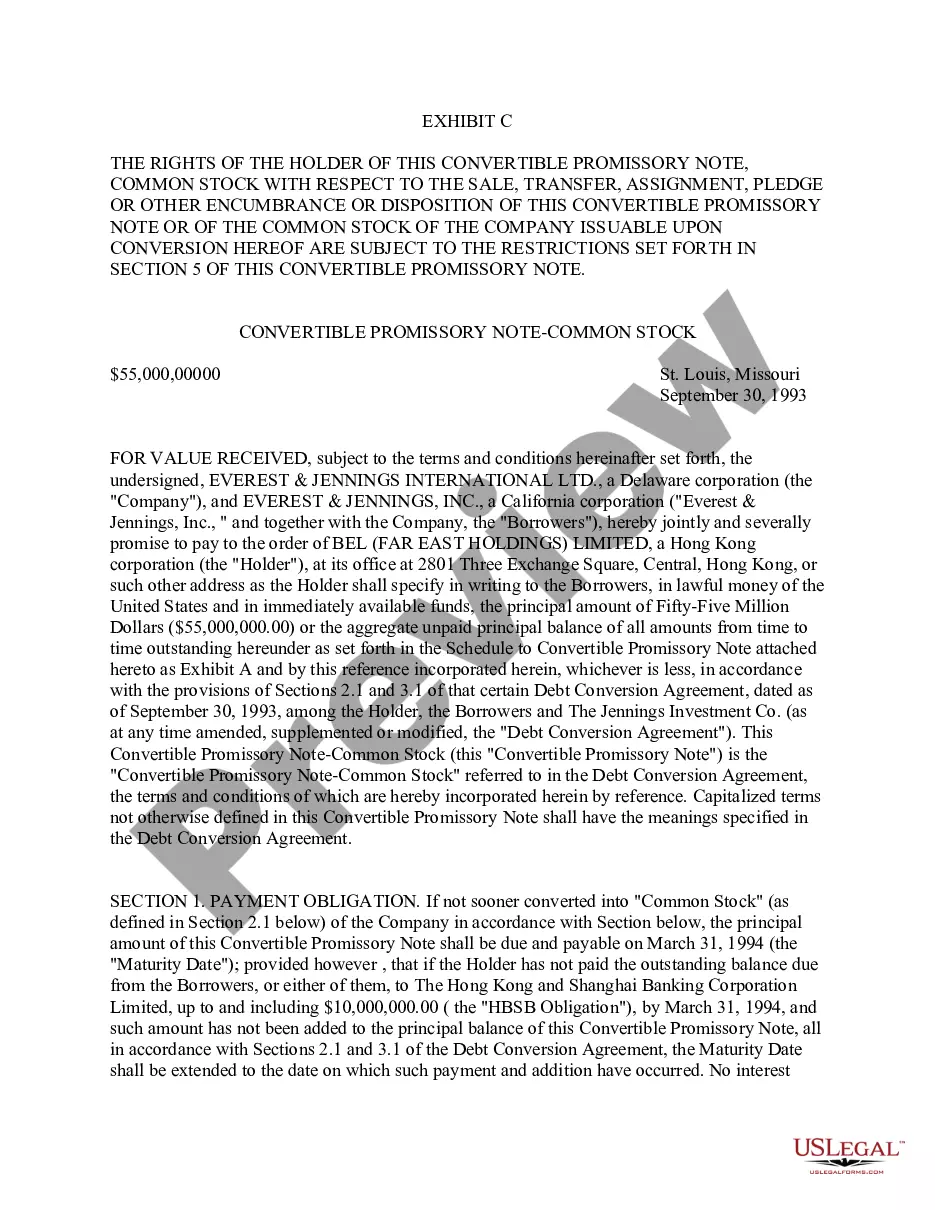

Convertible Note Corporation With Warrants

Description

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

The Convertible Note Corporation With Warrants that you observe on this website is a versatile legal template created by expert attorneys adhering to federal and state laws.

For over 25 years, US Legal Forms has offered individuals, entities, and legal practitioners more than 85,000 validated, state-specific forms for any professional and personal event. It’s the fastest, simplest, and most dependable method to acquire the documents you require, as the service promises bank-grade data protection and anti-malware safeguards.

Register with US Legal Forms to access verified legal templates for all of life’s circumstances at your fingertips.

- Search for the document you require and examine it.

- Scan through the sample you searched for and preview it or assess the form description to ensure it meets your specifications. If it does not, utilize the search feature to find the correct one. Click Buy Now when you have found the template you need.

- Register and Log In.

- Choose the pricing plan that fits your needs and create an account. Use PayPal or a credit card to make a quick payment. If you already possess an account, Log In and check your subscription to continue.

- Obtain the fillable template.

- Select the format you want for your Convertible Note Corporation With Warrants (PDF, DOCX, RTF) and download the example onto your device.

- Complete and sign the document.

- Print the template to fill it out by hand. Alternatively, use an online multifunctional PDF editor to quickly and accurately fill out and sign your form digitally.

- Download your paperwork again.

- Utilize the same document again whenever necessary. Open the My documents tab in your profile to redownload any previously saved forms.

Form popularity

FAQ

Warrants are recorded on a balance sheet as either equity or a liability, depending on the specific terms of the warrant. For a convertible note corporation with warrants, if the warrants are equity instruments, they appear under shareholders’ equity, diluting the ownership percentage when exercised. Conversely, if conditions suggest a liability classification, it will show under long-term liabilities. Proper accounting ensures that stakeholders understand the company's financial position concerning these financial instruments.

A convertible warrant example involves a company that issues warrants alongside a convertible note. For instance, when a startup raises funds, it might offer investors a convertible note corporation with warrants, allowing them to convert their debt into equity at a later date while holding the option to buy additional shares. This arrangement can enhance investor interest, as it provides potential upside along with the security of a debt instrument. Overall, convertible warrants can be an attractive incentive for early-stage investors.

Convertible notes typically cannot be converted at just any moment; they follow specific terms outlined in the agreement. Most note holders can convert their investments into equity during funding rounds or upon specific triggering events, such as a sale or acquisition of the company. Understanding these conditions is crucial for anyone involved with a convertible note corporation with warrants. If you're uncertain about the conversion process, US Legal Forms can provide guidance on your options.

Generally, converting warrants into shares is not a taxable event. Instead, tax implications usually arise when you sell the shares acquired from the conversion. It’s advisable to consult a tax professional or legal expert familiar with convertible note corporations with warrants to fully understand the specific tax implications for your situation.

Warrant coverage in a convertible note gives an investor the right to purchase additional shares of stock in a company.

Companies often issue stock warrants by attaching the warrant to a bond or other security that they use to raise capital. The warrant helps attract investors and also represents potential future capital for the issuing company.

Warrants, on the other hand, typically don't have any intrinsic value of their own. Unlike convertible securities, there's no underlying bond or preferred shares that give the warrant owner any additional rights. The only value that the warrant has comes from its conversion feature.

What Is a Warrant Coverage on a Convertible Note? On a convertible note, a warrant coverage allows the holder to purchase additional shares of a company. The amount that is allowed to be purchased is a percentage based on the loan principal.

Warrants are typically issued by companies as a way to raise capital, while convertible debt is usually issued by investors as a way to hedge their investment. Another key difference is that warrants are often attached to debt, while convertible debt is often attached to equity.