Convertible Note Corporation Template With Tax

Description

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

Securing a primary source for obtaining the latest and pertinent legal templates constitutes a significant portion of navigating bureaucracy. Identifying the appropriate legal documents necessitates precision and carefulness, which underscores the importance of sourcing Convertible Note Corporation Template With Tax exclusively from trustworthy providers, such as US Legal Forms. An incorrect template will squander your time and delay your current situation. With US Legal Forms, you have minimal concerns. You can access and review all pertinent details regarding the document’s application and significance for your circumstances and in your jurisdiction.

Follow these steps to complete your Convertible Note Corporation Template With Tax.

Eliminate the hassle associated with your legal documentation. Explore the extensive US Legal Forms library to discover legal templates, assess their applicability to your situation, and download them instantly.

- Use the catalog navigation or search bar to find your template.

- Examine the form’s description to verify if it meets the prerequisites of your state and locality.

- Check the form preview, if available, to confirm that the form aligns with your requirements.

- Return to the search and seek the appropriate template if the Convertible Note Corporation Template With Tax does not fulfill your needs.

- If you are confident about the form’s applicability, download it.

- If you are a registered user, click Log in to verify and gain entry to your chosen forms in My documents.

- If you lack an account, click Buy now to acquire the template.

- Select the pricing option that meets your needs.

- Continue to the registration to finalize your purchase.

- Conclude your purchase by selecting a payment method (credit card or PayPal).

- Select the document format for downloading Convertible Note Corporation Template With Tax.

- Once you have the form on your device, you can modify it using the editor or print it and fill it out manually.

Form popularity

FAQ

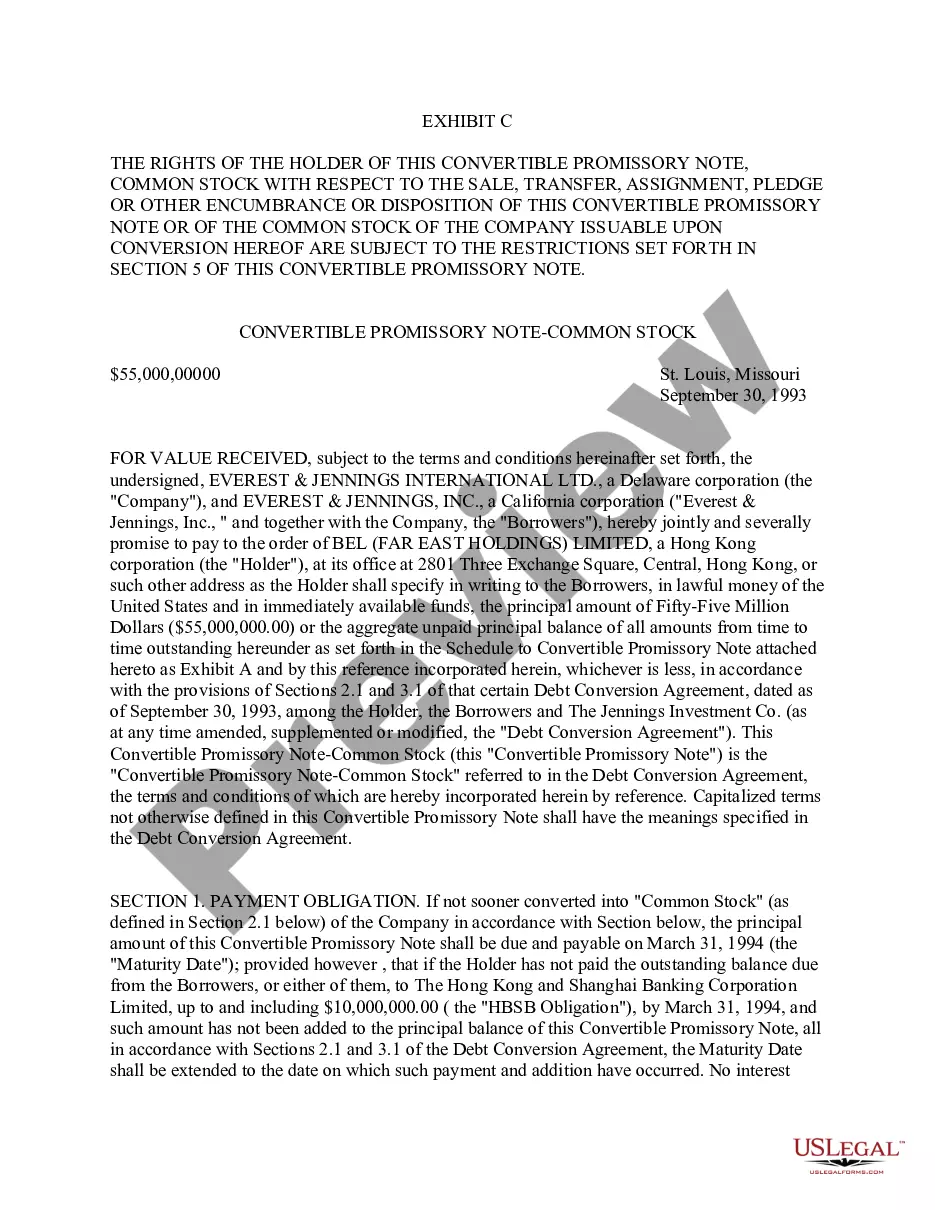

Under a longstanding IRS ruling published over fifty years ago, the conversion of a convertible note for stock of the note's issuer does not result in realized gain or loss because it is not treated as a taxable exchange.

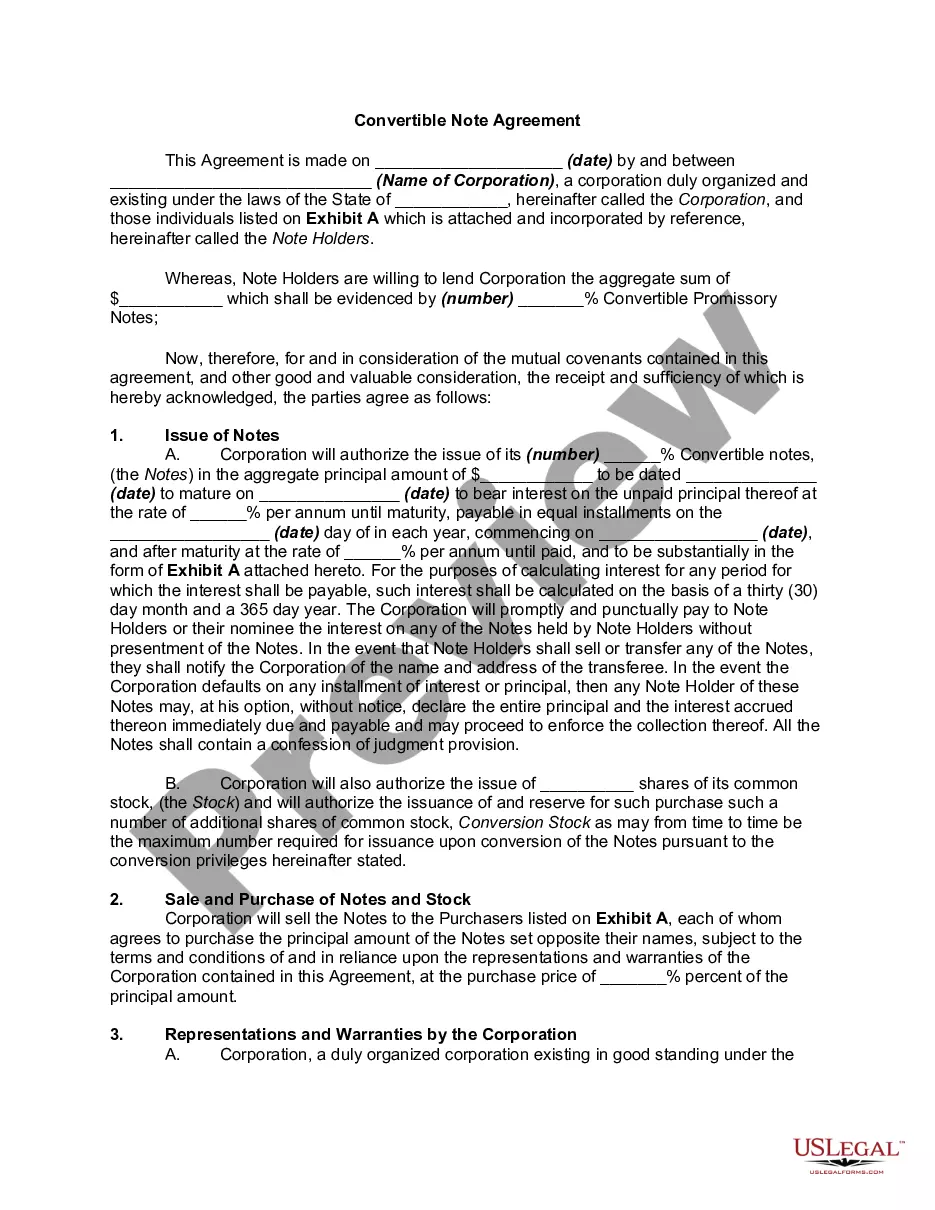

Convertible notes are usually structured as a single agreement called the note purchasing agreement. This covers all of the financing terms. Promissory notes are then issued to individual investors with the date and amount of their investment.

Under a longstanding IRS ruling published over fifty years ago, the conversion of a convertible note for stock of the note's issuer does not result in realized gain or loss because it is not treated as a taxable exchange.

1. Conversion is generally not a taxable event. 2. Certain adjustments to the conversion ratio that have the effect of increasing a convertible note holder's proportionate interest in the issuer can result in a deemed distribution to the convertible note holder even though no cash is actually distributed.

Purchase. The purchase of convertible debt is not a taxable event to the holder unless he transfers appreciated or depreciated property in exchange for the debt. Similarly, the issuer's receipt of proceeds from issuing convertible debt is not a taxable event.