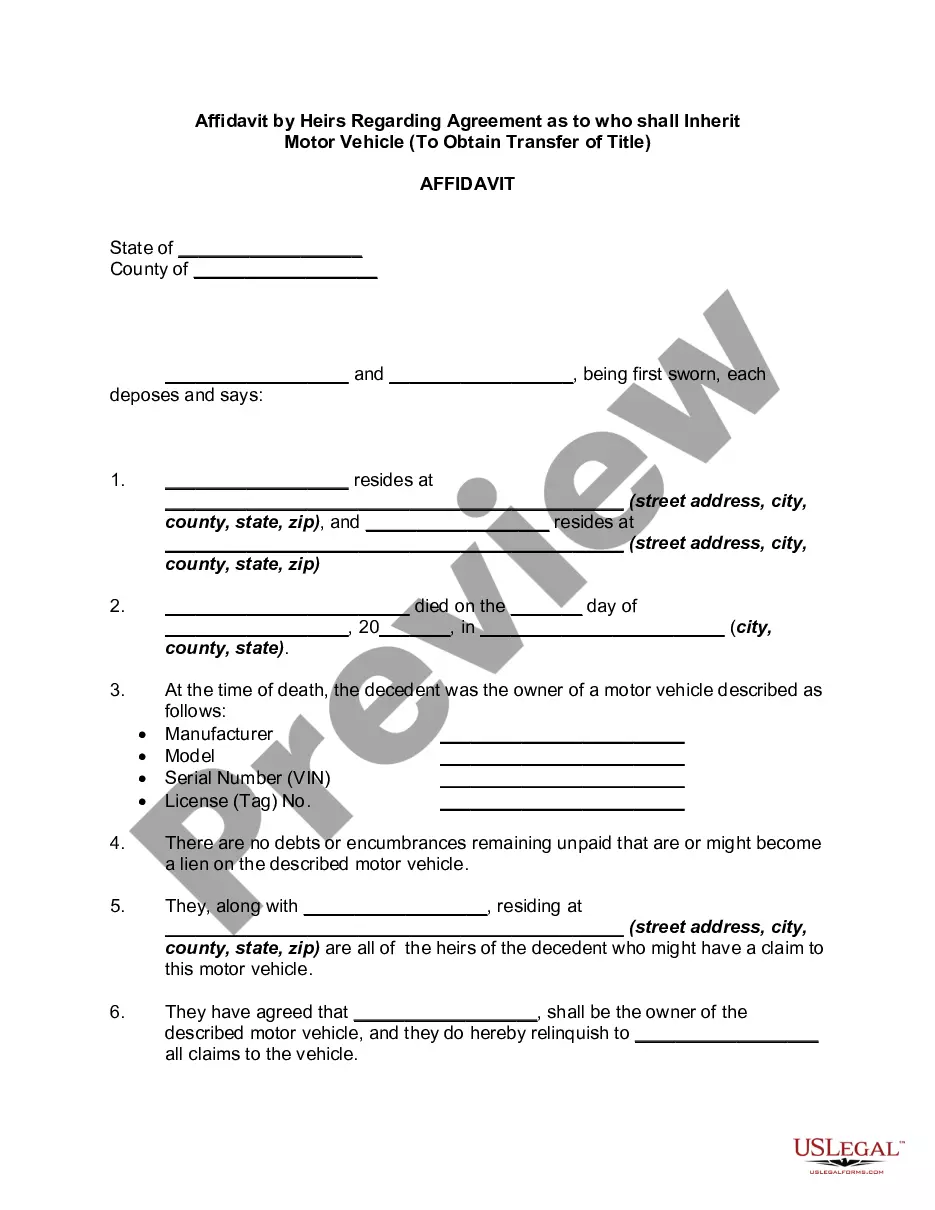

Sworn Statement Document With Withholding Tax

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sworn Statement Of Beneficiary Of Estate And Consent To Close Estate - Uniform Probate Code?

Obtaining legal document samples that comply with federal and local regulations is essential, and the internet provides a multitude of alternatives to select from.

However, what is the benefit of spending time looking for the appropriate Sworn Statement Document With Withholding Tax sample online if the US Legal Forms digital library already consolidates such templates.

US Legal Forms stands as the largest digital legal repository, featuring over 85,000 fillable templates prepared by attorneys tailored to any business or life situation.

Utilize the Preview feature or review the text outline to confirm it meets your specifications. Search for another sample using the search bar if necessary. Select Buy Now once you have located the right form and choose a subscription option. Create an account or Log In and complete your payment via PayPal or credit card. Choose the format for your Sworn Statement Document With Withholding Tax and download it. All documents accessible through US Legal Forms are reusable. To re-download and finalize previously acquired forms, navigate to the My documents tab in your account. Take advantage of the most comprehensive and user-friendly legal document service!

- They are easy to navigate, with all documents categorized by state and intended use.

- Our specialists stay informed on legislative changes, ensuring that your documents are always current and compliant when acquiring a Sworn Statement Document With Withholding Tax from our site.

- Securing a Sworn Statement Document With Withholding Tax is straightforward and fast for both existing and new users.

- If you already possess an account with an active subscription, Log In and save the document sample you require in your desired format.

- If you are a newcomer to our website, follow the steps outlined below.

Form popularity

FAQ

Final Withholding Tax is a kind of withholding tax which is prescribed only for certain payors and is not creditable against the income tax due of the payee for the taxable year.

Procedure. In the Implementation Guide for Financial Accounting , choose Financial Accounting Global Settings ? Withholding Tax ? Extended Withholding Tax ? Calculation ? Withholding Tax Types ? Define Withholding Tax Type for Payment Posting .

Apply online at the DOR's Taxpayer Access Point portal to receive a Withholding Account Number immediately after completing the registration. Find an existing Withholding Account Number: on Form 89-105, Employer's Withholding Tax Return. by contacting the DOR.

Employees may change their Mississippi and Federal withholding tax rates by completing a new Mississippi Form 89-350 ?and Federal Form W-4.

1- Income from French securities paid to individuals and legal entities that do not have their actual residence or registered office in France is subject to withholding tax in France. Withholding tax rates are usually 25% for dividends, 16% for interest, and 33% for royalties.