Ending An Irrevocable Trust For A House

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

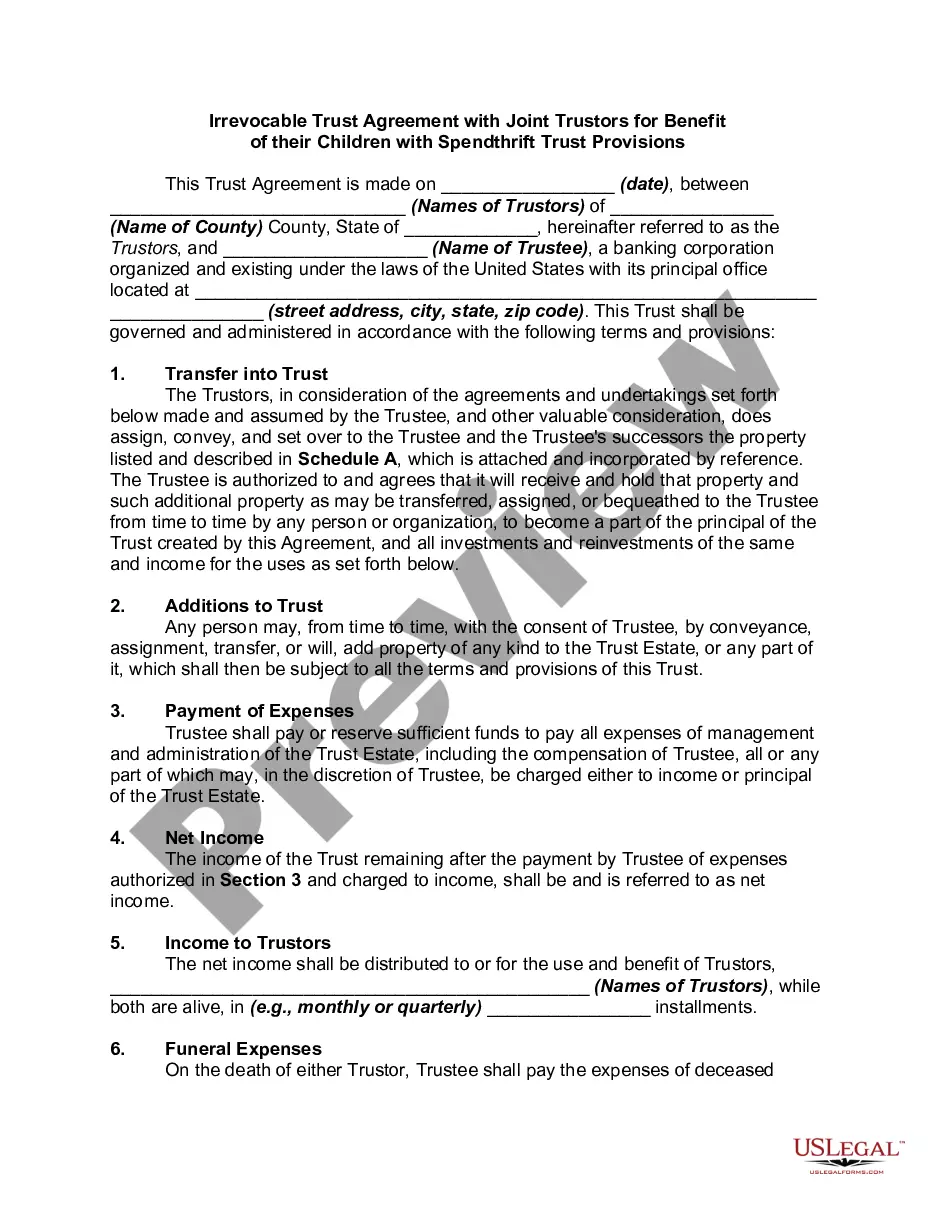

How to fill out Irrevocable Trust Agreement For Benefit Of Trustor's Children And Grandchildren With Spendthrift Trust Provisions?

Locating a reliable source for obtaining the latest and suitable legal documents is part of the challenge of managing bureaucracy.

Identifying the correct legal papers requires accuracy and carefulness, which is why it is crucial to take samples of Terminating An Irrevocable Trust For A Home exclusively from reputable providers, such as US Legal Forms. An incorrect form will squander your time and delay your current situation.

Once you have the form on your device, you can modify it using the editor or print it out and complete it manually. Eliminate the hassle associated with your legal documentation. Explore the extensive US Legal Forms library where you can find legal templates, verify their suitability for your situation, and download them instantly.

- Utilize the catalog navigation or search bar to locate your template.

- Examine the details of the form to confirm it meets the needs of your state and locality.

- Review the form preview, if accessible, to make sure the template is what you are looking for.

- Continue searching to find the appropriate template if the Terminating An Irrevocable Trust For A Home does not satisfy your needs.

- When you are confident about the form's relevance, download it.

- If you are a registered customer, click Log in to verify and access your chosen forms in My documents.

- If you don’t have an account yet, click Buy now to acquire the template.

- Choose the pricing option that fits your requirements.

- Advance to registration to complete your purchase.

- Finish your transaction by selecting a payment method (credit card or PayPal).

- Choose the document format for downloading Terminating An Irrevocable Trust For A Home.

Form popularity

FAQ

The two most common ways to terminate and/or modify an irrevocable trust is to 1) argue that there has been a change of circumstances not anticipated by the settlors at the time they created the trust (for example changes in tax law, and 2) argue that all beneficiaries consent to the proposed termination and or ...

Instead, in most cases, an irrevocable trust can only be dissolved by court order. The details of dissolving an irrevocable trust differ widely between states and jurisdictions. However, typically you will need to get approval from the trust's beneficiaries and potentially its trustees as well.

The irrevocable trust will automatically dissolve if its intent has been fulfilled. You might also contend that: The purpose of the trust has become illegal, impossible, wasteful or impractical to fulfill; Compliance with trust terms preclude accomplishing a material purpose of the trust; and.

Placing a home into an irrevocable trust can protect it from creditors and litigation, but when the home is sold, someone will have to pay the capital gains on the sale. Although irrevocable trusts are great for distributing assets to beneficiaries, they are also responsible for paying capital gains taxes.

Unless the assets are included in the taxable estate of the original owner (or ?grantor?), the basis doesn't reset. To get the step-up in basis, the assets in the irrevocable trust now must be included in the taxable estate at the time of the grantor's death.