Accounting Tips

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

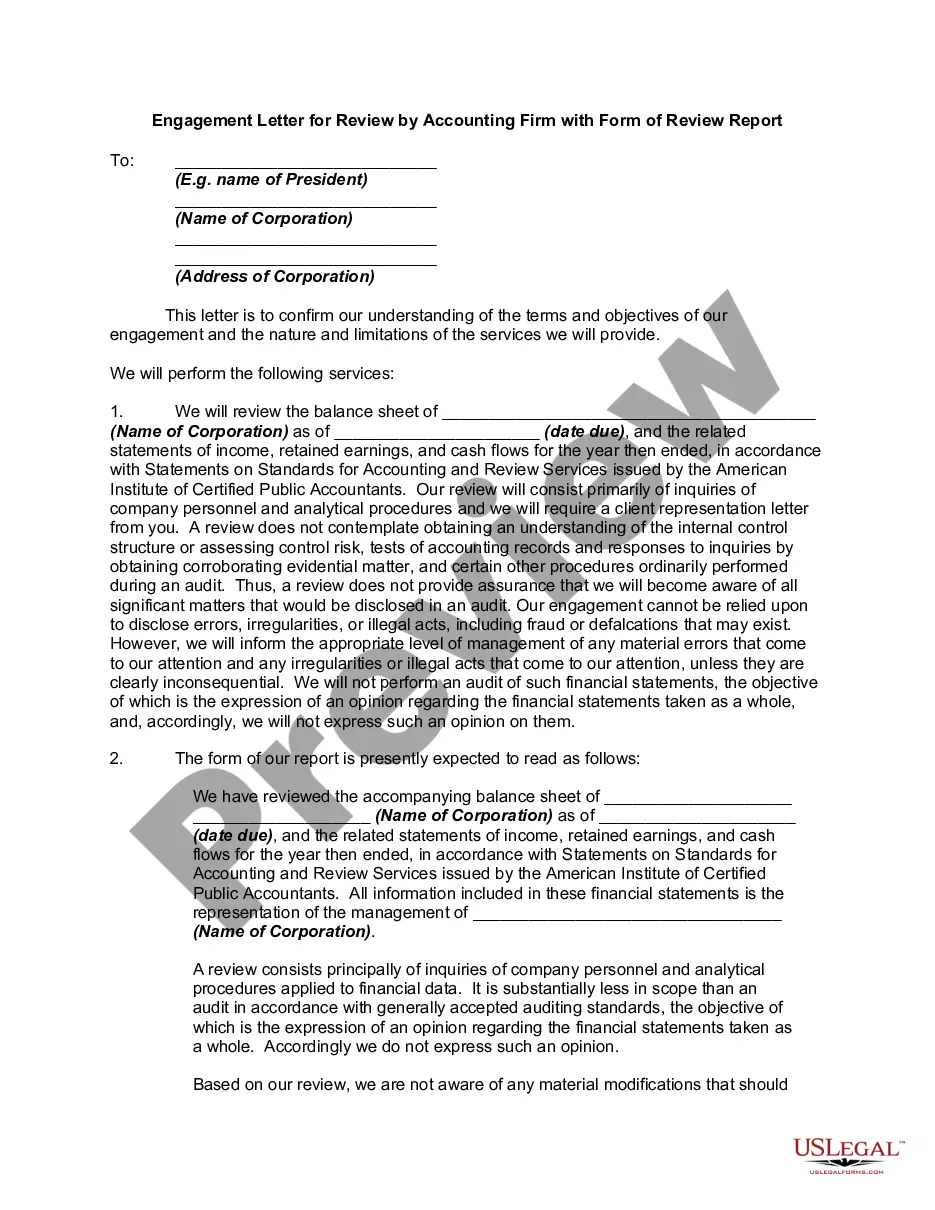

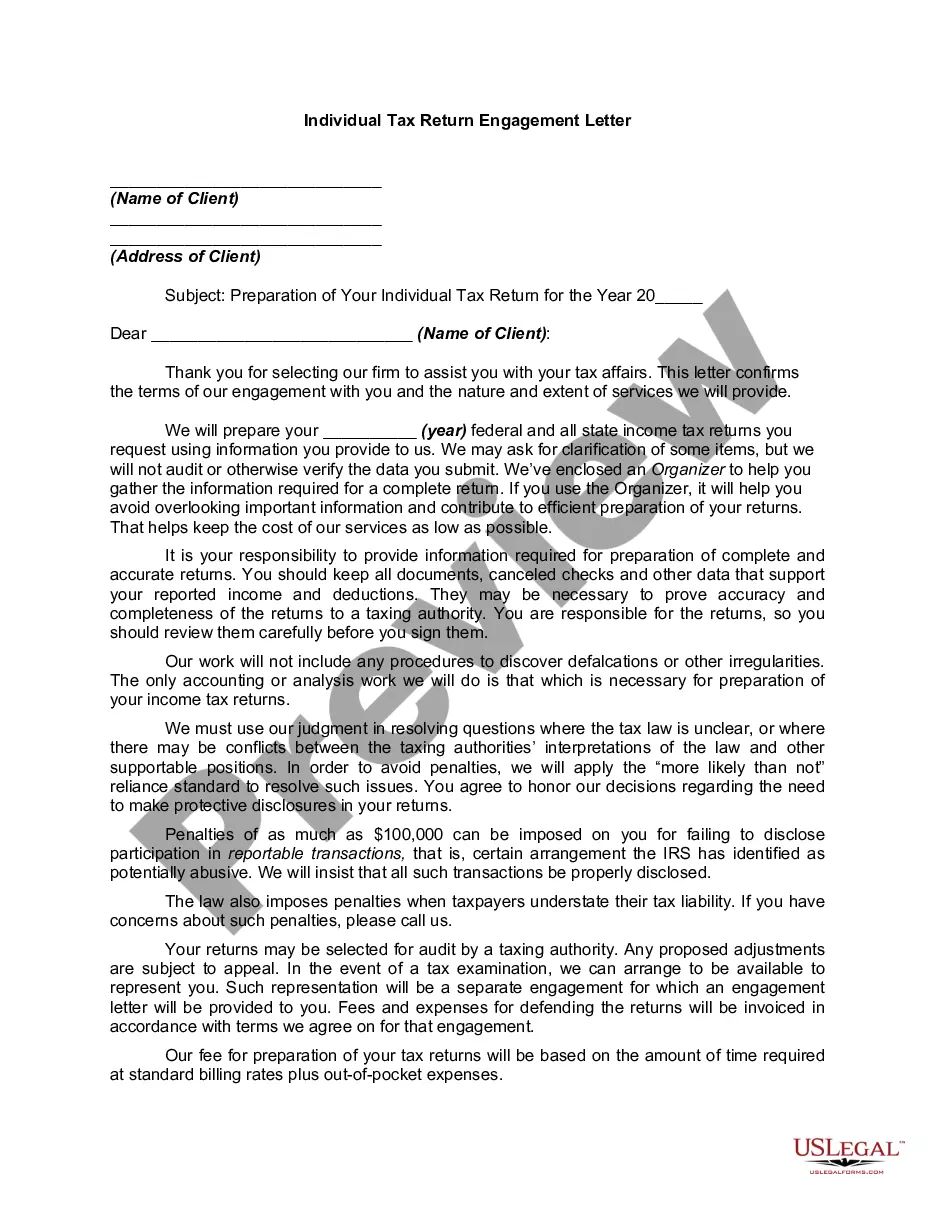

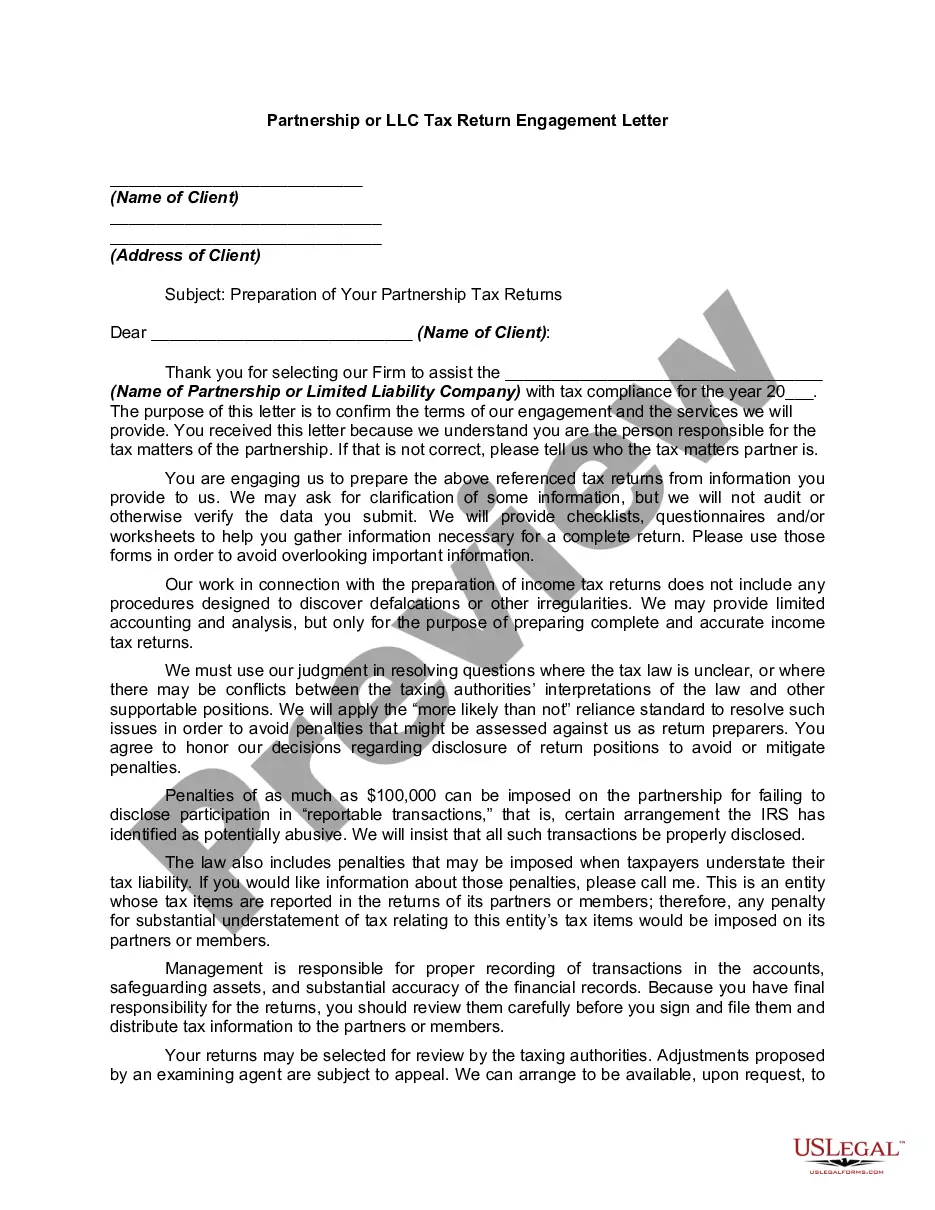

How to fill out Engagement Letter Between Accounting Firm And Client For Tax Return Preparation?

- If you're a returning user, first ensure your subscription is active. Then, log in to your account and select the desired form template to download it.

- For new users, begin by checking the Preview mode and description of the forms. Make certain that you select the form that meets your specific legal requirements.

- Should you find any inconsistencies, utilize the Search tab to locate an alternate template that fits your needs.

- Once you have found the correct form, click on the Buy Now button and select a subscription plan that works for you. You'll need to create an account to access the complete library.

- Complete your purchase by entering your payment details, be it through a credit card or your PayPal account.

- Finally, download and save your form for further use, which can be accessed anytime through the My Forms section of your profile.

By following these steps, you'll not only save time but also ensure that your legal documents are accurate and compliant. US Legal Forms offers a reliable platform with over 85,000 forms to suit various needs.

Start your journey towards efficient legal documentation today and see how easy it can be with US Legal Forms!

Form popularity

FAQ

The four fundamental aspects of accounting include Recognizing Transactions, Recording Transactions, Reporting Transactions, and Analyzing Transactions. These fundamentals guide the overall accounting process, ensuring each transaction is properly documented and communicated. Embracing these fundamentals as part of your accounting tips can significantly impact how you manage and present your financial data.

To improve your accounting skills, start by learning the basic principles and concepts thoroughly. Regular practice through exercises and real-world scenarios is essential; consider utilizing accounting software for hands-on experience. Additionally, exploring resources, tips, and guides on the US Legal Forms platform can provide you with valuable insights and tools that streamline your accounting process.

The primary rule in accounting is the Double-Entry System, which states that every financial transaction must affect at least two accounts. This ensures that the accounting equation remains balanced, maintaining the integrity of your financial records. Understanding this rule is a fundamental accounting tip that can help you create accurate reports and avoid common pitfalls in your accounting journey.

The five principles of Generally Accepted Accounting Principles (GAAP) include Revenue Recognition, Expense Recognition, Full Disclosure, Materiality, and Consistency. These principles guide how financial statements are prepared and ensure transparency. By adhering to GAAP, you can boost your accounting practices and understand your financial situation better. Implementing these principles is one of the many accounting tips that can enhance your financial reports.

Employers account for tips by recording them in their payroll and accounting systems. They must also ensure that tips are reported as wages for tax purposes. Following accounting tips for proper recording can help employers avoid legal issues and ensure compliance with labor laws. Utilize resources like US Legal Forms for guidance on best practices in managing tip-related income.

Tips must be reported to the IRS as part of your income on your tax return. If you earn over a certain amount in tips, you are required to report them using IRS Form 4070. Accounting tips recommend documenting your tips accurately to avoid discrepancies with the IRS. Keeping detailed records can make this process smoother and ensure compliance.

Yes, tips should be recorded as revenue in your accounting records. This practice helps ensure that your financial statements accurately reflect your income. Moreover, accounting tips for recording tips can help you stay compliant with tax regulations. By categorizing tips as revenue, you maintain transparency in your financial reporting.

The number one rule of accounting focuses on the double-entry system, which ensures that every financial transaction affects at least two accounts. This principle is vital for maintaining accurate financial records. By following essential accounting tips, you can master this rule and enhance your accounting practices. Tools like US Legal Forms can assist you in managing your accounting documentation.

Yes, it is possible to earn $500,000 a year in accounting, especially in senior roles or specialized fields. Factors such as experience, education, and location play crucial roles in salary potential. To increase your earning potential, utilize strategic accounting tips and invest in further training or certifications.

The first step in accounting involves identifying and documenting all financial transactions. This ensures accurate recording, which leads to reliable financial statements. Familiarizing yourself with basic accounting tips can help streamline this process for improved efficiency. Consider using tools like US Legal Forms to organize your financial documents.