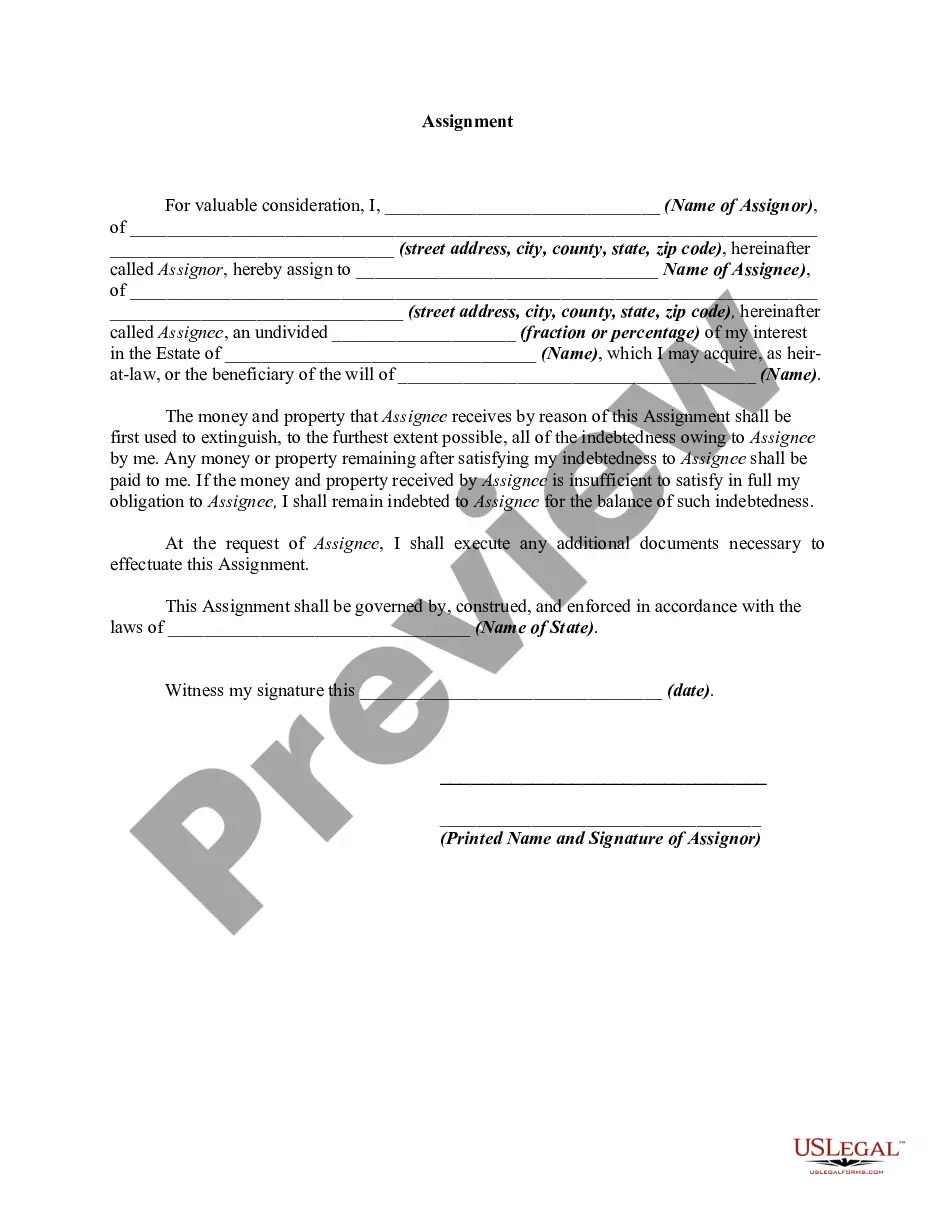

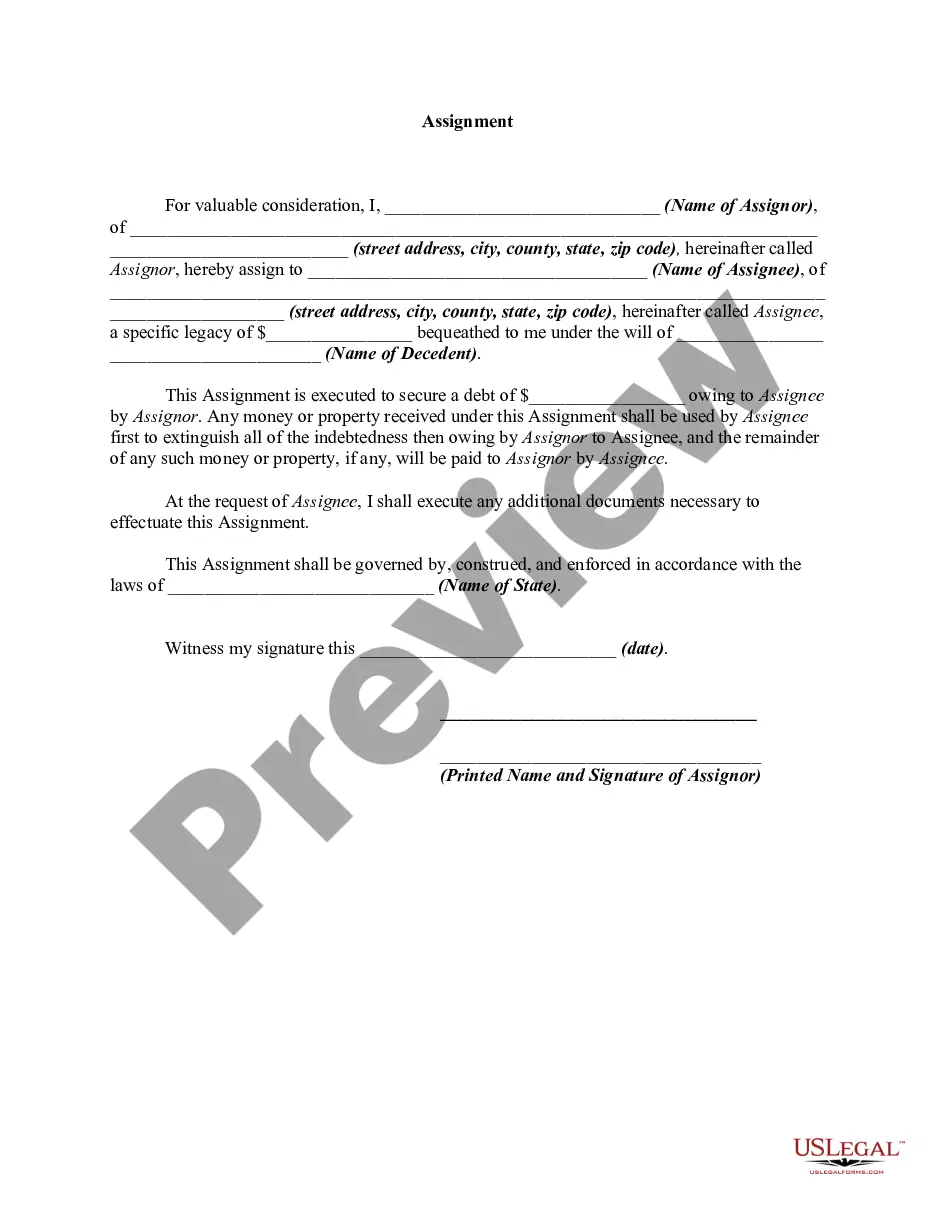

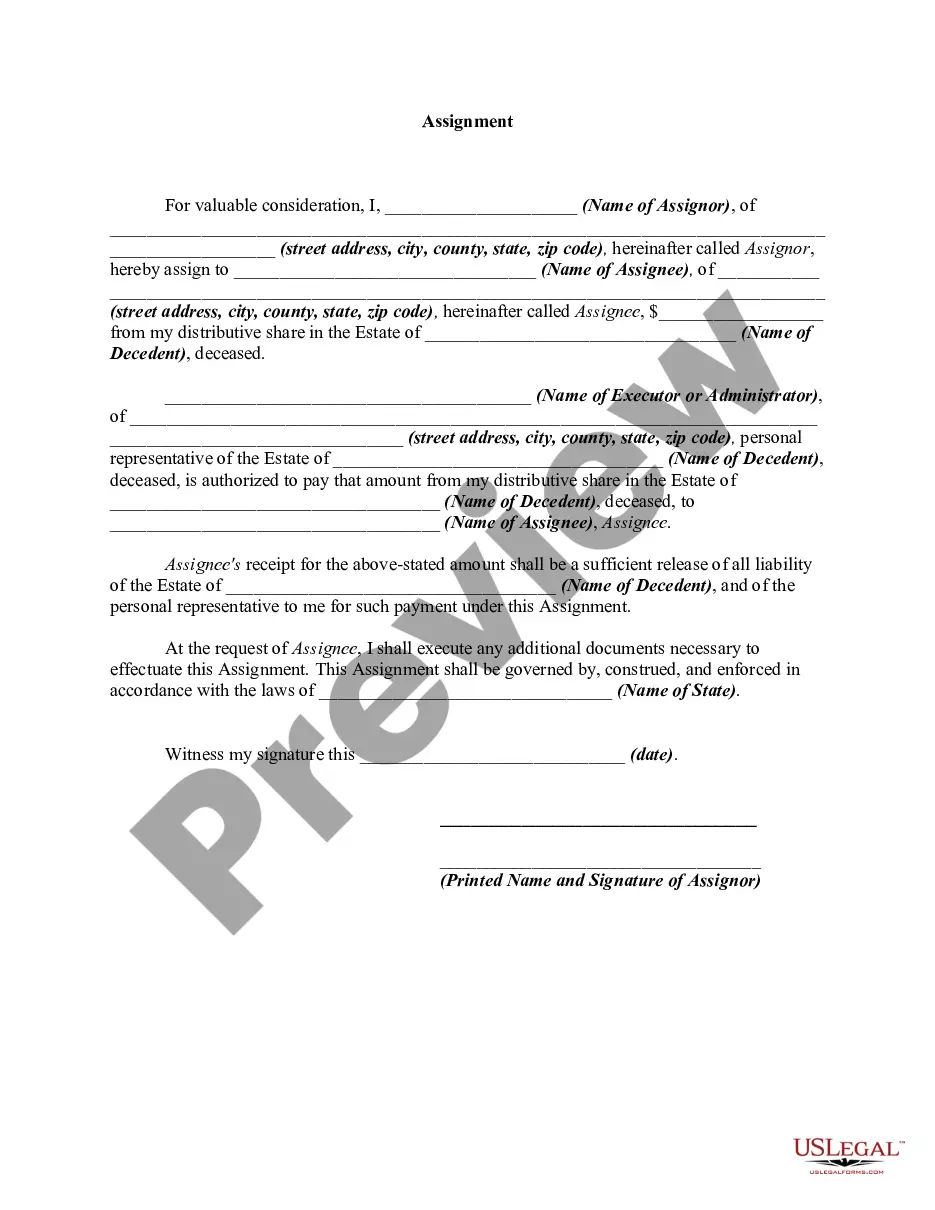

Assignment All Interest With Negative Capital Account

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Assignment Of All Of Expected Interest In Estate In Order To Pay Indebtedness?

Obtaining legal document samples that comply with federal and local laws is essential, and the internet provides a plethora of choices to choose from.

However, why waste time searching for the correct Assignment All Interest With Negative Capital Account template online when the US Legal Forms digital library already has this documentation compiled in one location.

US Legal Forms is the largest online legal repository featuring over 85,000 fillable templates crafted by attorneys for any business or personal situation.

Review the template using the Preview feature or through the textual outline to ensure it meets your needs.

- They are straightforward to navigate, with all documents organized by state and intended use.

- Our specialists stay current with legislative updates, so you can trust that your documents are always accurate and compliant when obtaining an Assignment All Interest With Negative Capital Account from our site.

- Acquiring an Assignment All Interest With Negative Capital Account is simple and swift for all users, whether new or returning.

- If you already possess an account with an active subscription, Log In and download the required document sample in your desired format.

- For new visitors, follow these steps.

Form popularity

FAQ

A negative capital account balance indicates a predominantly outward money flow from a country to other countries. The implication of a negative capital account balance is that ownership of assets in foreign countries is increasing.

This final capital account tabulation is a great indicator of what a partner's taxable gain would be if the interest were sold. From a tax standpoint, a negative capital account is treated as a capital gain upon sale. Conversely, a positive capital account is treated as a capital loss if the interest is sold.

A negative capital account implies a disinvested position on the underlying assets of the partnership, so the IRS requires assurance that the partner with a negative capital account provides restitution to cover its deficit position in the event of liquidation.

If a partnership is liquidated where a partner has a negative capital account, the partner with the negative capital account is expected to pay back the amount owed to the partnership within 90 days of the partnership termination or by the end of the year, whichever comes first.

However, a partner's capital account can be negative. This generally happens when the partnership allocates losses or receives a distribution funded by debt incurred by the partnership. These actions can result in a taxable event for partners, so proactive steps need to be taken to avoid a negative balance.