Residential Home Purchase Withdrawal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

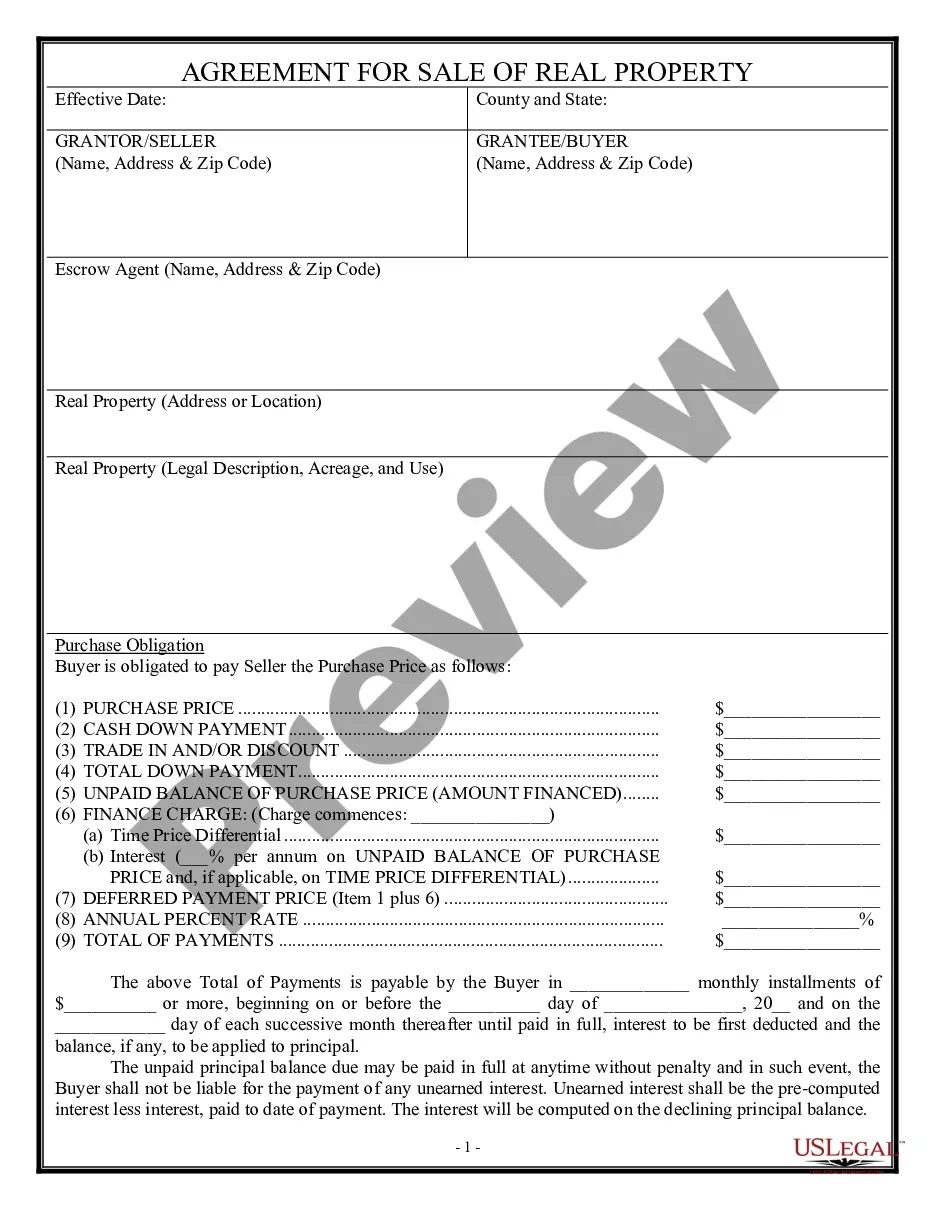

How to fill out Agreement For Sale, Short Form - Residential?

It’s well-known that you cannot instantly become a legal specialist, nor can you quickly learn how to prepare a Residential Home Purchase Withdrawal without possessing a dedicated set of competencies.

Drafting legal documents is a lengthy process that necessitates particular training and expertise. So why not entrust the creation of the Residential Home Purchase Withdrawal to the experts.

With US Legal Forms, one of the most extensive collections of legal templates, you can access anything from court documents to templates for internal business communications.

If you need a different template, initiate your search again.

Create a free account and select a subscription plan to acquire the form. Click on Buy now. After completing the purchase, you can obtain the Residential Home Purchase Withdrawal, complete it, print it, and deliver or mail it to the appropriate parties or organizations.

- We recognize the importance of compliance with federal and state legislation and regulations.

- For this reason, all forms on our site are location-specific and updated frequently.

- Start by visiting our website to obtain the form you require in just a few minutes.

- Utilize the search bar at the top of the page to find the document you need.

- If previewing is available, check it and review the accompanying description to confirm whether the Residential Home Purchase Withdrawal matches your requirements.

Form popularity

FAQ

Changing your mind after signing a real estate contract can be complicated but is sometimes possible. If you have a valid reason under the terms of the agreement, such as unmet contingencies, you may execute a residential home purchase withdrawal effectively. Review your contract carefully and consider seeking assistance from experienced professionals, like those at USLegalForms, to navigate the process smoothly.

To back out of buying a property, first review your contract for any contingencies that might apply. Common reasons for residential home purchase withdrawal include financing issues, property inspection results, or title problems. You should communicate your decision to the seller in a timely manner and consider consulting a legal expert if needed, such as those available through USLegalForms for personalized guidance.

Yes, you must report any Residential home purchase withdrawal from your IRA on your tax return. The IRS requires this information to calculate potential taxes owed. Ensure you include the information provided on Form 1099-R when filing your return. US Legal Forms offers tools to assist you in navigating tax implications and making accurate reports.

To report a Residential home purchase withdrawal from your IRA, you will generally need to complete Form 1099-R. This form details the amount you have withdrawn from your account. It's important to keep a copy for your records and to ensure accurate reporting on your taxes. By using US Legal Forms, you can easily obtain the necessary documents and guidance for proper IRA management.

Under the Home Buyers' Plan, you can withdraw up to $35,000 from your RRSP for a residential home purchase withdrawal. If you are purchasing with a spouse or common-law partner, both of you can withdraw this amount, totaling $70,000 for your home purchase. Remember, these funds must be repaid to your RRSP over a specific time frame to avoid tax penalties.

To withdraw from a Home Buyers' Plan, first confirm that you're eligible by having an agreement to purchase a qualifying home. Next, complete the necessary paperwork, including the Form T1036, to make a residential home purchase withdrawal. On approval, the funds will be disbursed to assist you in buying your new home.

The 59.5 withdrawal rule refers to a guideline that applies primarily to retirement accounts, stating that withdrawals before age 59.5 typically incur penalties. Understanding this rule is important if you consider a residential home purchase withdrawal since early withdrawals can affect your long-term retirement savings. However, the HBP offers an exception for those using RRSP funds to purchase their first home.

To initiate a residential home purchase withdrawal from your RRSP for the Home Buyers' Plan, you must complete Form T1036. This form allows you to specify the amount you wish to withdraw. Ensure you have a qualifying home purchase agreement in place, as this is a crucial requirement for the HBP.

The Home Buyers' Plan (HBP) allows for a residential home purchase withdrawal from your RRSP, but it comes with drawbacks. One major disadvantage is that you must repay the withdrawn amount over 15 years, adding a long-term commitment. Additionally, not repaying the amount can lead to tax implications, which might strain your finances later on.