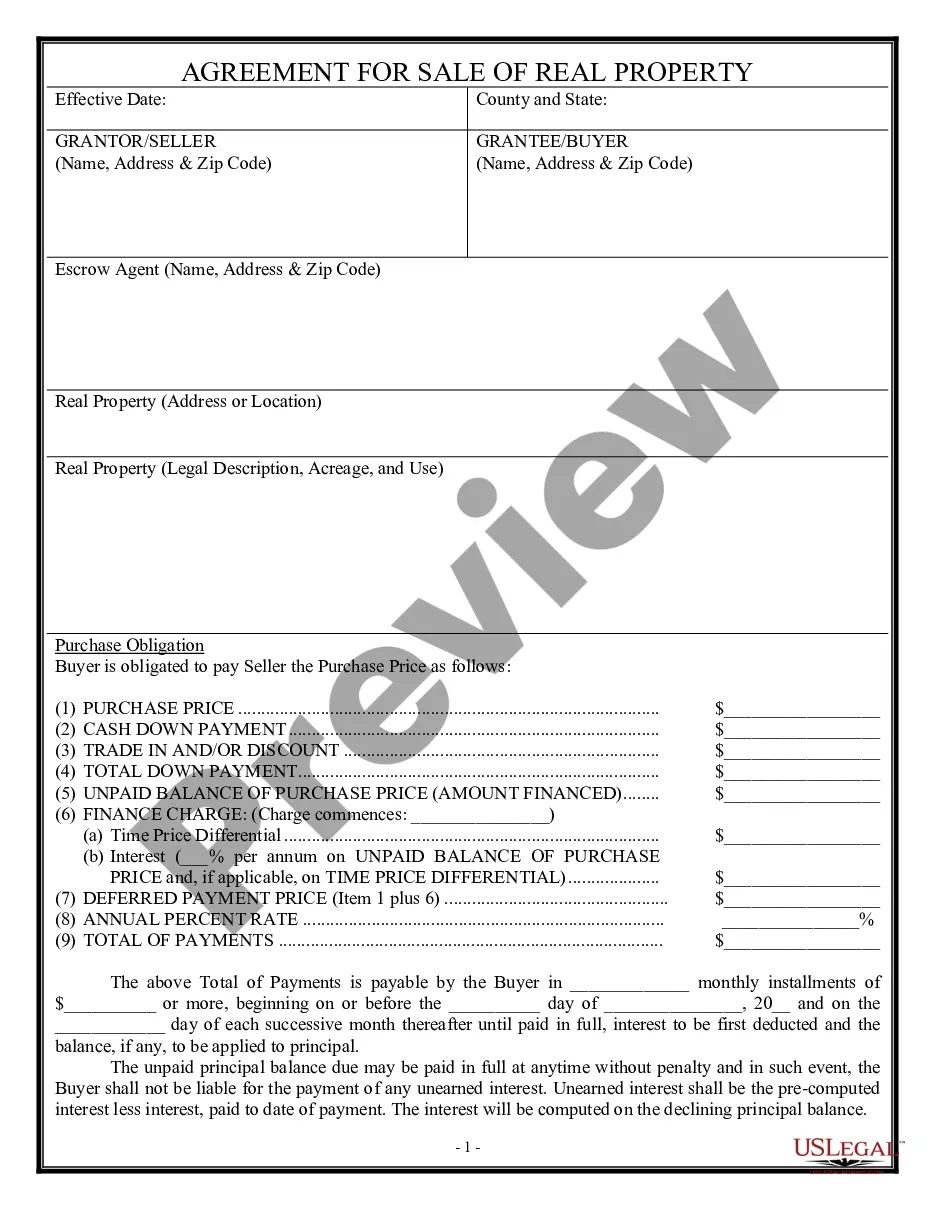

Home Purchase With 401k

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement For Sale, Short Form - Residential?

Legal documentation management can be daunting, even for experienced experts.

If you are interested in a Home Purchase With 401k and lack the time to search for the appropriate and current version, the procedures may be stressful.

US Legal Forms meets all your requirements, from personal to business documentation, all in one convenient place.

Leverage cutting-edge tools to complete and manage your Home Purchase With 401k.

Here are the steps to follow after downloading the necessary form: Verify it is the correct form by previewing and reviewing its description. Confirm that the template is valid in your state or county. Click Buy Now when you are prepared. Choose a monthly subscription plan. Select the file format you require, and Download, complete, sign, print, and send your document. Enjoy the US Legal Forms online library, supported by 25 years of expertise and reliability. Change your everyday document management into a simple and user-friendly process today.

- Tap into a resource library of articles, manuals, and guides relevant to your situation and requirements.

- Save time and energy searching for the documents you need, and utilize US Legal Forms' advanced search and Review feature to find Home Purchase With 401k and download it.

- If you hold a membership, Log In to your US Legal Forms account, search for the form, and download it.

- Check your My documents tab to discover the documents you previously saved and manage your folders as desired.

- If this is your first experience with US Legal Forms, create a free account and gain unlimited access to all the platform's benefits.

- A comprehensive online form library could be a transformative solution for anyone seeking to handle these circumstances efficiently.

- US Legal Forms is a leader in the online legal form industry, offering over 85,000 state-specific legal documents available to you at any time.

- With US Legal Forms, you can access legal and business forms tailored to your state or county.

Form popularity

FAQ

You can withdraw $10,000 or half your vested amount in the plan up to a maximum of $50,000 to purchase a house. If you're taking out an asset-based mortgage, you can use 70% of what you have in your retirement accounts as income to qualify for the loan.

Yes, it's possible to take money out of your 401(k) to purchase a house outright or cover the down payment on a house. However, be aware that you'll be taxed on any funds you withdraw.

Borrowing 401(k) funds to buy a home Since this is essentially loaning money to yourself, you don't have to pay the early withdrawal penalty or income tax on the amount you initially withdraw. As long as you pay it back on time, you won't owe the IRS any extra money for this type of withdrawal.

Yes, you can use your 401(k) to buy a house without penalty, provided you use a 401(k) loan rather than a withdrawal. Unlike a 401(k) withdrawal, a 401(k) loan is not subject to a 10 percent early distribution penalty from the IRS. The money you receive will not be taxed as income.