Debtor Harassing For These

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

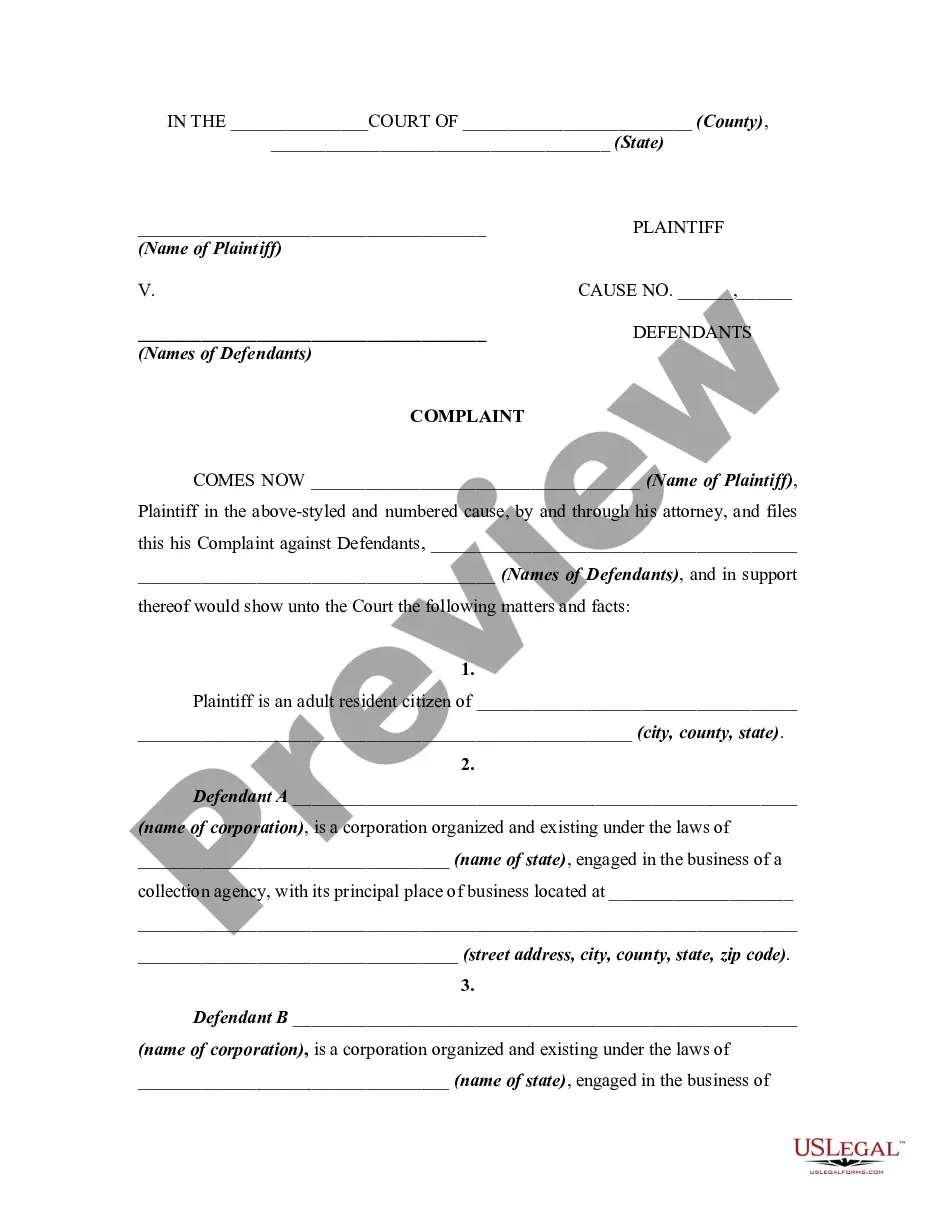

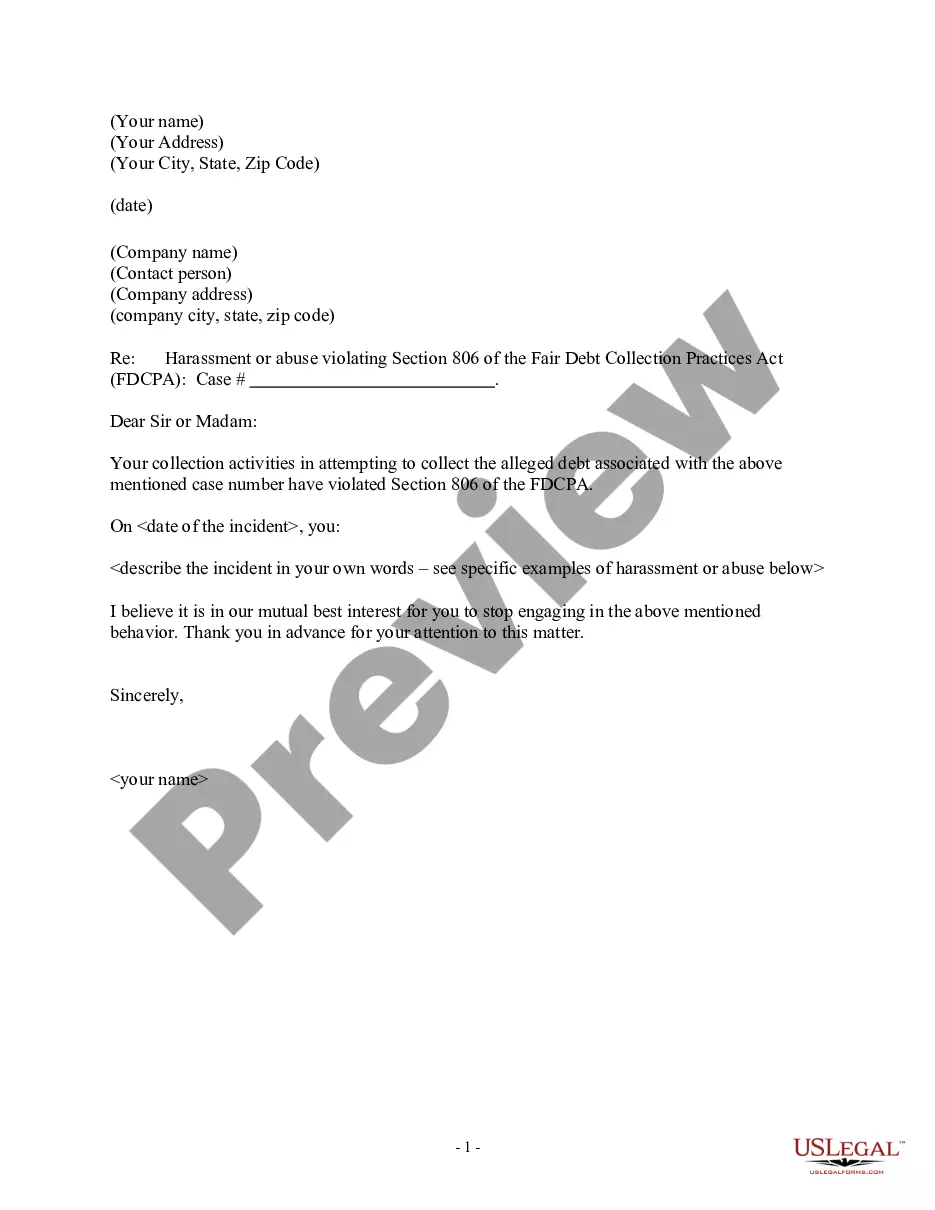

How to fill out Complaint By Debtor For Harassment In Attempting To Collect A Debt, Using Harassing And Malicious Information, And Violating The Federal Fair Debt Collection Practices Act?

It’s obvious that you can’t become a legal professional overnight, nor can you figure out how to quickly prepare Debtor Harassing For These without having a specialized set of skills. Creating legal documents is a long venture requiring a particular education and skills. So why not leave the creation of the Debtor Harassing For These to the specialists?

With US Legal Forms, one of the most comprehensive legal template libraries, you can access anything from court documents to templates for in-office communication. We understand how important compliance and adherence to federal and local laws and regulations are. That’s why, on our website, all forms are location specific and up to date.

Here’s start off with our platform and get the form you require in mere minutes:

- Discover the document you need by using the search bar at the top of the page.

- Preview it (if this option available) and check the supporting description to figure out whether Debtor Harassing For These is what you’re looking for.

- Begin your search again if you need a different form.

- Register for a free account and select a subscription plan to purchase the template.

- Choose Buy now. Once the transaction is complete, you can download the Debtor Harassing For These, complete it, print it, and send or send it by post to the designated individuals or entities.

You can re-gain access to your forms from the My Forms tab at any time. If you’re an existing client, you can simply log in, and locate and download the template from the same tab.

No matter the purpose of your documents-be it financial and legal, or personal-our platform has you covered. Try US Legal Forms now!

Form popularity

FAQ

Dispute in writing, and include any evidence that supports your claims (such as copies of cancelled checks showing you paid the debt or a police report in the case of identity theft). If the debt collector knows that you don't owe the money, it should not try to collect the debt.

Summary: If you're being sued by a debt collector, here are five ways you can fight back in court and win: 1) Respond to the lawsuit, 2) make the debt collector prove their case, 3) use the statute of limitations as a defense, 4) file a Motion to Compel Arbitration, and 5) negotiate a settlement offer.

Dispute in writing, and include any evidence that supports your claims (such as copies of cancelled checks showing you paid the debt or a police report in the case of identity theft). If the debt collector knows that you don't owe the money, it should not try to collect the debt.

Don't pay, don't promise to pay and don't give any payment information the collector may use later. Ask for information on the debt and say you'll call back to discuss it later. Making a single payment ? even just $5 or $10 ? is an acknowledgment of the debt and can have serious repercussions.

Don't provide personal or sensitive financial information Never give out or confirm personal or sensitive financial information ? such as your bank account, credit card, or full Social Security number ? unless you know the company or person you are talking with is a real debt collector.