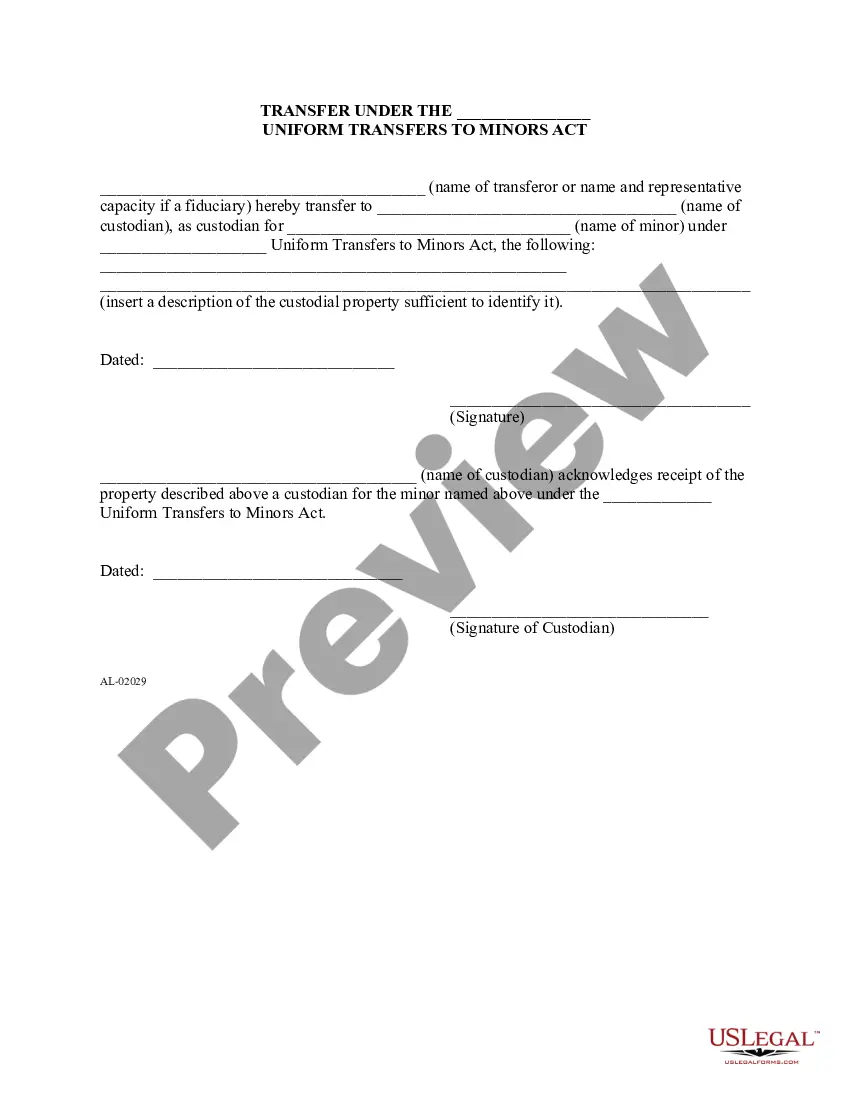

Uniform Transfers With Interest

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Transfer Of Property Under The Uniform Transfers To Minors Act?

Obtaining a reliable resource to access the most up-to-date and pertinent legal templates is half the challenge of navigating bureaucracy.

Locating the appropriate legal documents requires precision and carefulness, which is why it is crucial to take samples of Uniform Transfers With Interest solely from credible sources, such as US Legal Forms. An incorrect template will squander your time and delay your situation.

Eliminate the hassle that comes with your legal documentation. Browse the extensive US Legal Forms library where you can discover legal templates, assess their applicability to your situation, and download them immediately.

- Utilize the library navigation or search bar to find your template.

- Examine the form’s description to verify if it meets the criteria of your state and county.

- View the form preview, if available, to confirm that the form is indeed the one you seek.

- Return to the search and locate the suitable document if the Uniform Transfers With Interest does not fulfill your requirements.

- If you are confident about the form’s relevance, proceed to download it.

- As an authorized user, click Log in to verify and access your chosen templates in My documents.

- If you do not possess an account yet, click Buy now to acquire the template.

- Select the pricing plan that aligns with your needs.

- Continue to the registration to complete your purchase.

- Finalize your purchase by selecting a payment method (credit card or PayPal).

- Choose the document format for downloading Uniform Transfers With Interest.

- Once you have the form on your device, you may modify it using the editor or print it and fill it out manually.

Form popularity

FAQ

What are the tax rules for UTMA in 2023? In 2023, the first $1,250 of a child's unearned income from a UTMA account is tax-free. This is one of the main tax benefits of UTMA accounts. The next $1,250 is taxed at the child's rate, and income over $2,500 is taxed at the parent's rate.

Both of these accounts can grow exponentially over time, which makes them great savings vehicles for your kids, especially since the interest they earn will be based on the average market return for the stock market, as opposed to much lower basic savings account rates.

B or 1099DIV should be received at the end of the tax year from the financial institution handling the UGMA/UTMA account to report any interest or earnings on the account.

The first $1,100 in earnings in the UTMA account are tax-free. This earnings figure includes dividends, interest income, and any capital gains. The next $1,100 in earnings is taxable at the child's tax rate. Because your child probably doesn't earn much income, their tax rate is typically 10%.

Because money placed in an UGMA/UTMA account is owned by the child, earnings are generally taxed at the child's?usually lower?tax rate, rather than the parent's rate. For some families, this savings can be significant. Up to $1,050 in earnings tax-free. The next $1,050 is taxable at the child's tax rate.