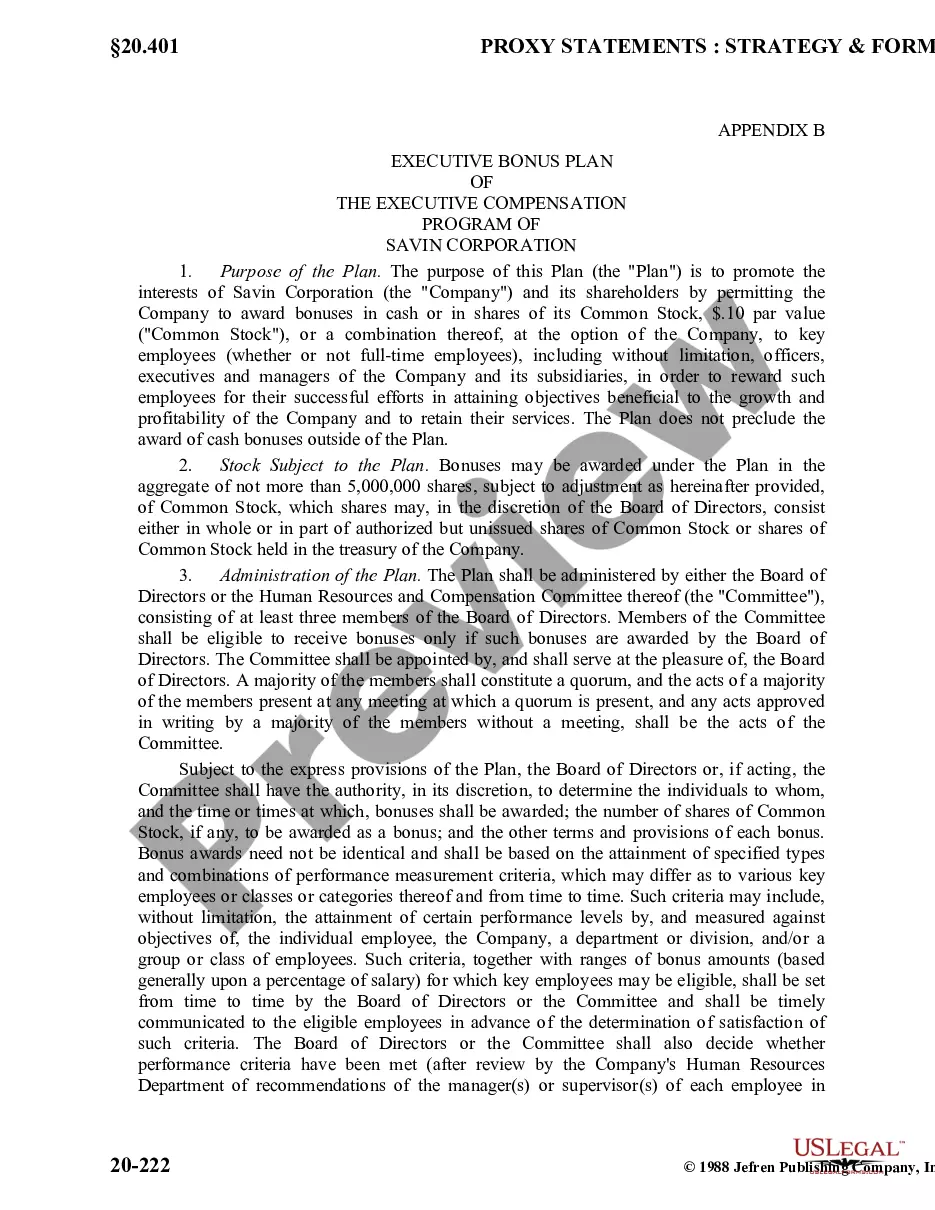

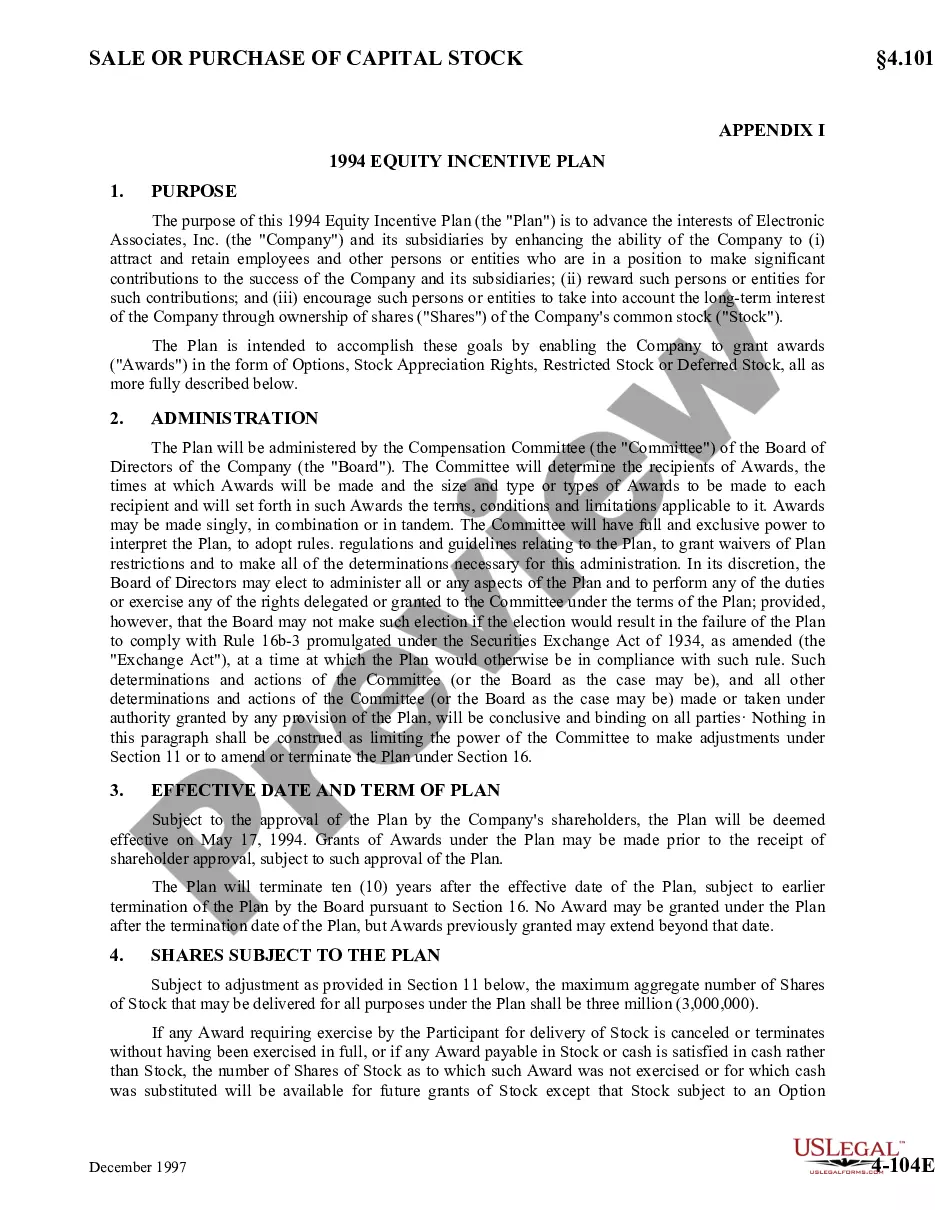

Employee Stock Incentive Plan With Bonus

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Executive Employee Stock Incentive Plan?

The Employee Stock Incentive Plan With Bonus displayed on this page is a reusable official template crafted by qualified attorneys in accordance with federal and local statutes and regulations.

For over 25 years, US Legal Forms has supplied individuals, companies, and legal experts with more than 85,000 validated, state-specific forms for any professional and personal circumstance. It’s the fastest, easiest, and most reliable method to acquire the documents you require, as the service ensures the utmost level of data protection and anti-malware measures.

Complete and sign the documents. Print the template for manual completion, or use an online multi-functional PDF editor to swiftly and accurately fill out and sign your form with a legally-binding electronic signature. Download your documents again when necessary. Revisit the My documents tab in your account to redownload any forms you previously saved. Subscribe to US Legal Forms to have verified legal templates for every aspect of life readily available.

- Search for the document you require and review it.

- Browse through the sample you searched and preview it or verify the form description to ensure it meets your requirements. If it doesn’t, use the search bar to locate the correct one. Click Buy Now when you have identified the template you need.

- Choose and Log In.

- Select the subscription plan that fits you and create an account. Use PayPal or a credit card for a quick payment. If you already possess an account, Log In and check your subscription to proceed.

- Acquire the editable template.

- Select the format you want for your Employee Stock Incentive Plan With Bonus (PDF, Word, RTF) and save the document on your device.

Form popularity

FAQ

The $100,000 limit for incentive stock options indicates the maximum aggregate value of options that can qualify for favorable tax treatment in one year. This rule is primarily applicable within employee stock incentive plans with bonus elements. Knowing this limit helps employees plan their stock options wisely and optimize their compensation.

The $100,000 limit typically refers to the cap on the value of incentive stock options that can be exercised in a calendar year. This important threshold is designed to keep tax payments lower for employees participating in employee stock incentive plans with bonus opportunities. It's crucial for employees to understand this limit to maximize their benefits.

The $100,000 incentive stock option limit refers to the maximum value of stock options that can be exercised in a year without incurring additional tax penalties. This limit is particularly relevant within employee stock incentive plans with bonus options. It ensures that employees benefit from favorable tax treatment while encouraging long-term ownership.

These options, which are contracts, give an employee the right to buy, or exercise, a set number of shares of the company stock at a preset price, also known as the grant price. This offer doesn't last forever, though. You have a set amount of time to exercise your options before they expire.

If this amount is not included in Box 1 of Form W-2, add it as "Other Income" on your Form 1040. Report the sale on your 2023 Schedule D, Part I as a short-term sale. The sale is short-term because not more than one year passed between the date you acquired the actual stock and the date you sold it.

Here's an example: You can purchase 1,000 shares of company stock at $20 a share with your vested ISO. Shares are trading for $40 in the market. If you already own 500 company shares, you can swap those shares (500 shares x $40 market price = $20,000) for the 1,000 new shares, rather than paying $20,000 in cash.

When you buy an open-market option, you're not responsible for reporting any information on your tax return. However, when you sell an option?or the stock you acquired by exercising the option?you must report the profit or loss on Schedule D of your Form 1040.

Contributions to a stock bonus plan are discretionary, but they must be substantial and recurring. Further, stock bonus plans cannot discriminate toward highly compensated employees, such as executives. Annual contributions to a stock bonus plan are limited to 25% of each employee's total compensation.