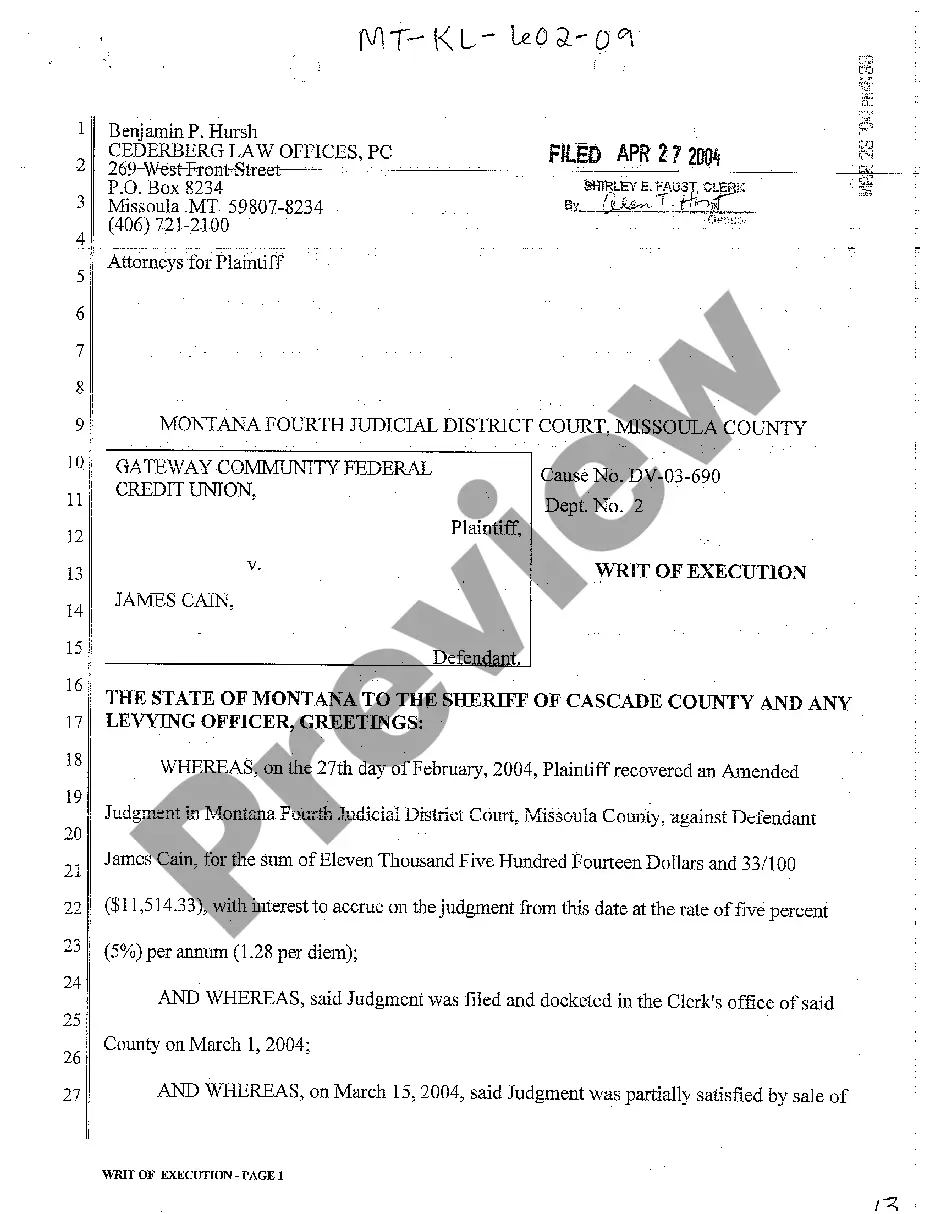

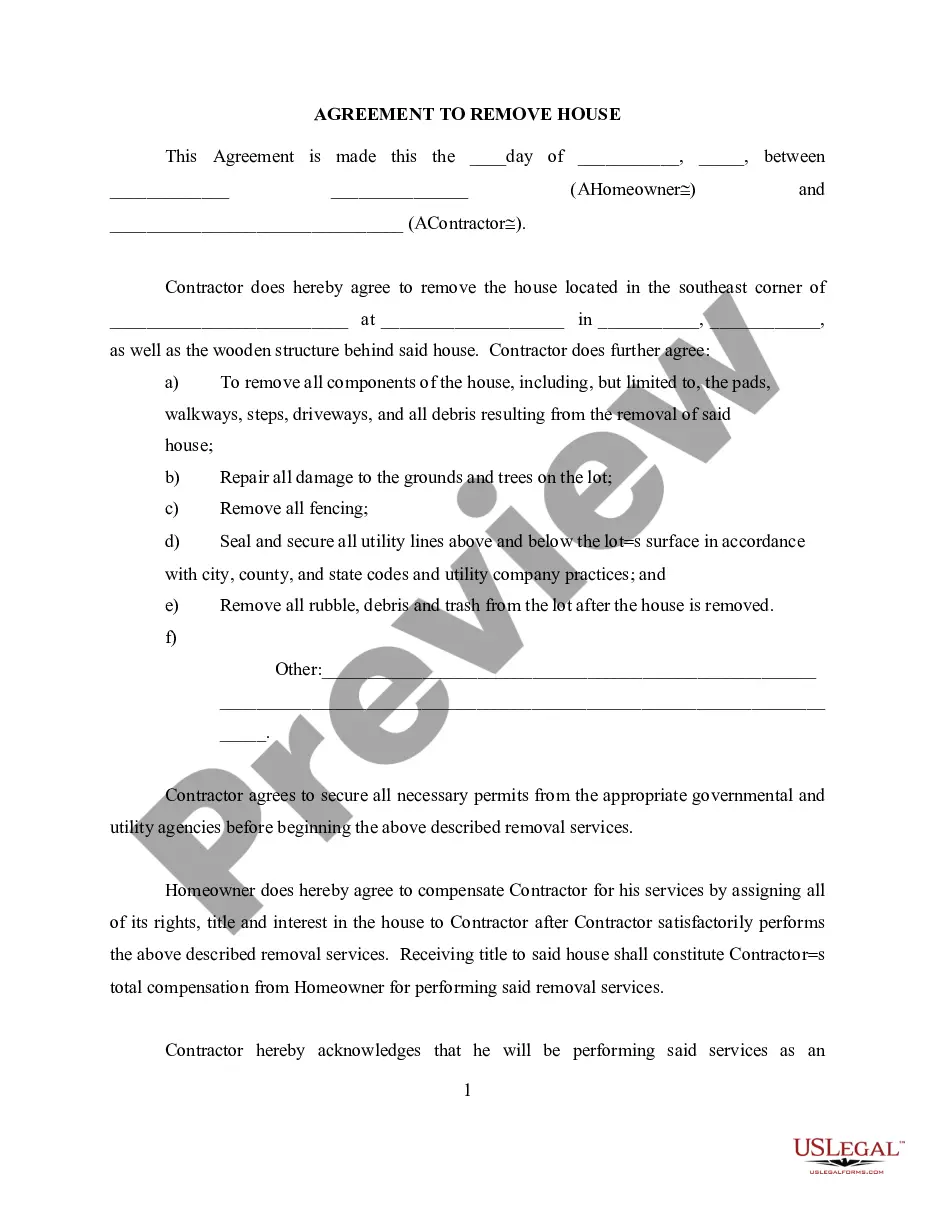

Construction Cost Contract Plus With Gst In Houston

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Grocery stores and convenience stores not only sell food products, they also sell a wide variety of other items and services – some of them taxable, and others nontaxable. For example, flour, sugar, bread, milk, eggs, fruits, vegetables and similar groceries (food products) are not subject to Texas sales and use tax.

If your customer provides the materials, then you are providing labor only. You're not responsible for tax on the materials. Under a lump-sum contract, you do not collect sales tax on materials or labor from your customer. You are the consumer of all items purchased to perform the work.

When we send a lump-sum payment directly to you, it is subject to a mandatory 20% federal withholding tax rate in the year you receive the payment. This withholding will be reported to the IRS and credited toward any income tax you may owe.

Contractor services performed on residential real property are not usually subject to sales tax. The Texas Administrative Code Section 3.291(a)(12) defines residential real property to include the following: Family dwellings.

(1) Food and food ingredients are exempt from sales tax unless otherwise taxable under subsection (c) of this section. (2) Water is exempt as explained in §3.318 of this title (relating to Water-Related Exemptions).

Texas Administrative Code. (a) Persons who must keep records. (1) Sellers of taxable items and purchasers who store, use, or consume taxable items in this state shall keep books, papers, and records in the form that the comptroller requires.

While there's no state income tax in Texas, there's a variety of other taxes you should make sure are taken care of. Currently, Texas unemployment insurance rates range from 0.25% to 6.25% with a taxable wage base of up to $9,000 per employee per year in 2025. Fun fact: the wage base has remained $9,000 since 1997.

Labor to repair, remodel, or restore residential real property is not taxable. Residential real property means family dwellings, including apartment complexes, nursing homes, iniums, and retirement homes. It does not include hotels or residential properties rented for periods of less than 30 days.