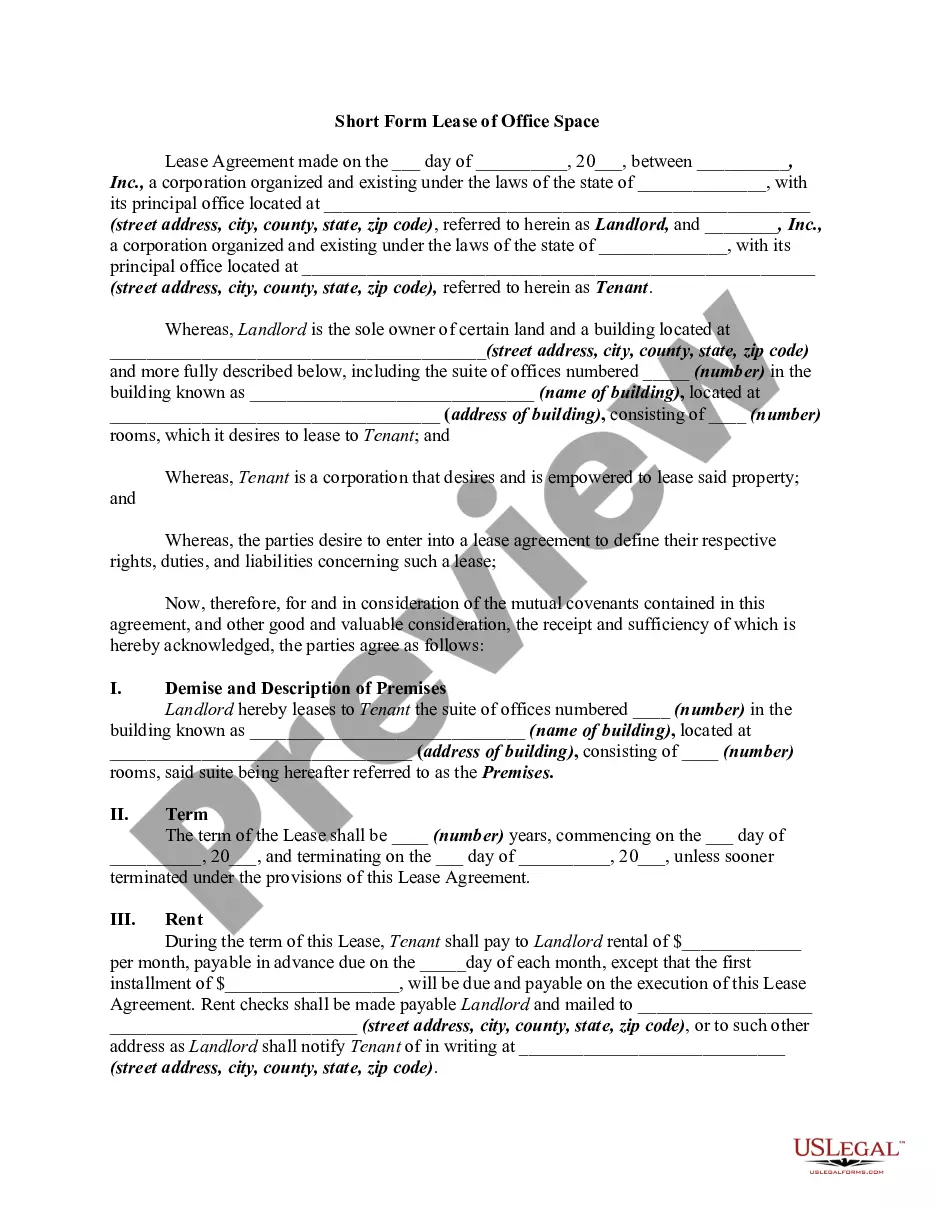

Commercial Lease Agreement Application With Kitchen In Collin

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

An LLC can be a great choice for food and beverage business owners looking to grow while protecting their personal assets from liability.

Compare Commercial Lease Agreements Gross leases tend to benefit the tenant, whereas net leases are more landlord friendly. In a gross lease, the tenant has more control over how much is spent on such expenses as janitorial services and utilities.

The most common net lease is a “triple net” lease agreement which shifts all operating expenses onto the restaurant. These expenses include maintenance costs, insurance and real property taxes.

For example, small mom and pop restaurants are probably best as sole proprietorships or partnerships. But, if your restaurant starts becoming popular and you're considering expanding and opening multiple locations, filing paperwork to become an LLC or corporation may be a worthwhile option.

This will be done using a Land Registry form known as a TR1. If the lease is for less than 7 years, then the lease can be assigned by using a deed of assignment. Both these documents have the same effect and will generally be executed by both you as the current tenant and the assignee.

Types of leasehold estates The first type is most common: Estate for years: An agreement that permits occupancy between two specified dates, at the end of which the property must be vacated. Estate from period to period: A monthly tenancy that has no specified end date.

1. Gross Lease. Gross leases are most common for commercial properties such as offices and retail space. The tenant pays a single, flat amount that includes rent, taxes, utilities, and insurance.

The triple net (NNN) lease is often considered the most prevalent form of commercial lease, particularly for retail and industrial properties, due to its predictability for landlords and clear delineation of expense responsibilities for tenants.

The landlord of a commercial space for rent may require the following: Security deposit (e.g., one month's rent or more) Financial statements. Profit and loss statements. Balance sheet. Business bank statements. Previous landlord information. Credit reports. Business tax returns.

What are the most important steps for drafting a commercial lease agreement? Identify the parties and the property. Determine the rent and the term. Negotiate the improvements and the maintenance. Allocate the taxes and the insurance. Include the clauses and the contingencies. Review and sign the agreement.