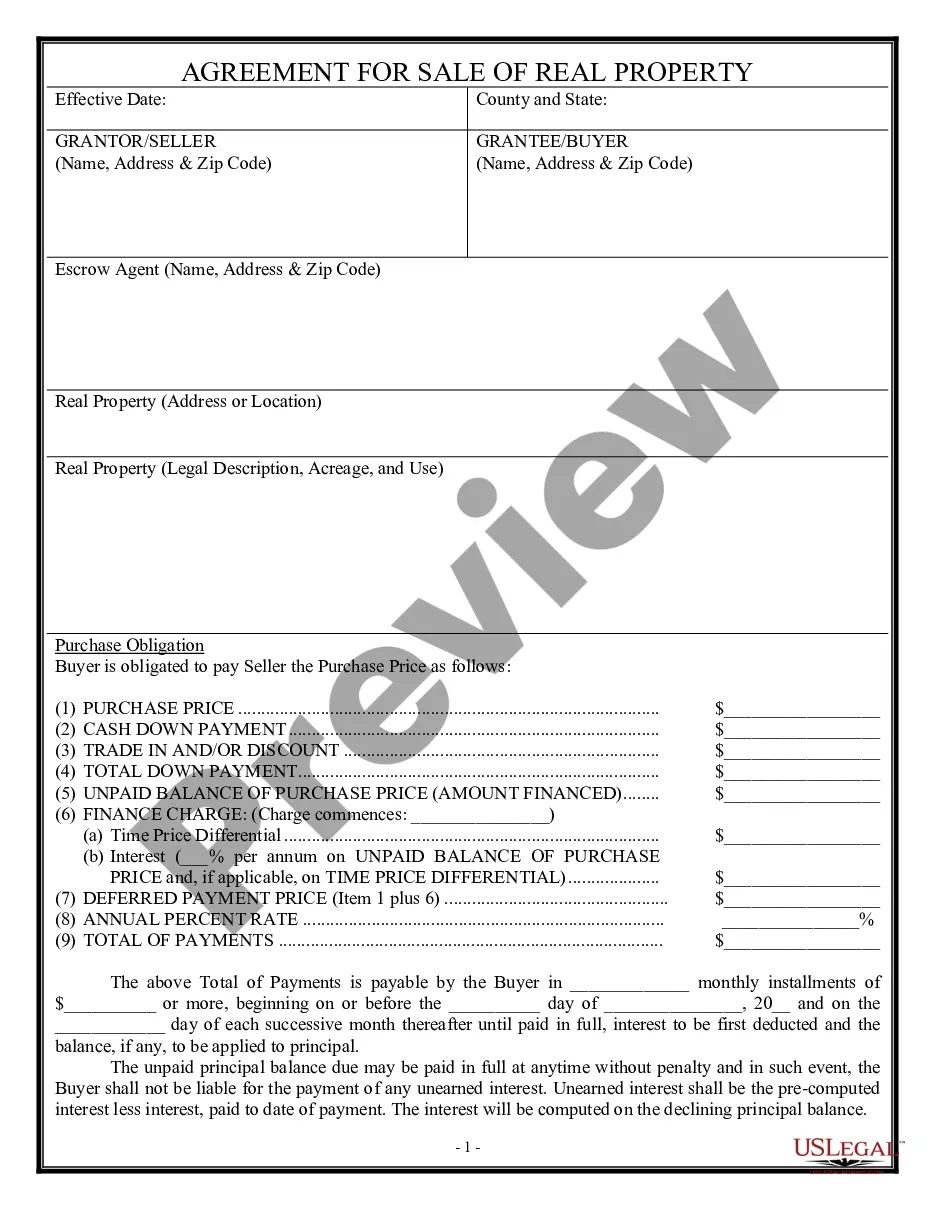

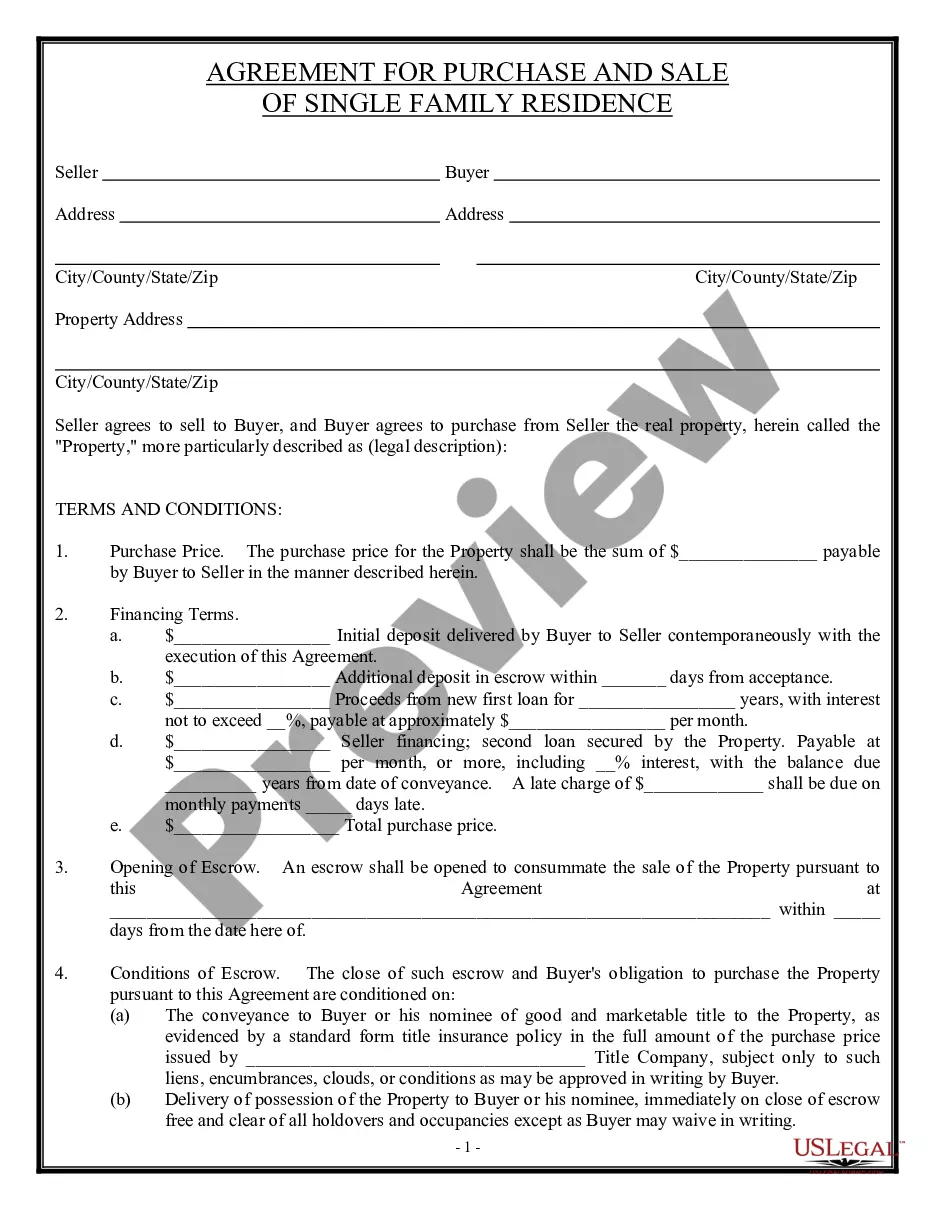

Closure Any Property Formula In Texas

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

What Are the Steps to Financial Close? Identify transactions and record them in a journal. Post to the general ledger. Prepare an unadjusted trial balance. Reconcile debits and credits. Create adjusting journal entries. Run an adjusted trial balance and financial statements. Close the books and generate financial reports.

To put it in simple terms, the seller will be responsible for the property tax balance that accrued from the beginning of the tax year until the date of closing, and the buyer will be responsible for property taxes that are due for the period after the closing date. This is a process called proration.

The closing process involves four specific steps: Step 1: Close revenue accounts to Income Summary. Income Summary is a temporary account used during the closing process. Step 2: Close expense accounts to Income Summary. Step 3: Close Income Summary to Retained Earnings. Step 4: Close dividends to Retained Earnings.

The closing process typically begins with reviewing and reconciling accounts to identify discrepancies and errors. Adjusting entries are then recorded to account for accruals, deferrals, depreciation, and other adjustments necessary to reflect the correct financial position.

In order to qualify for a non-judicial foreclosure, the lienholder must have a deed of trust with a "power of sale" clause, giving them the authority to sell the property. These foreclosures are governed by Section 51.002 of the Texas Property Code as well as the contractual documents.