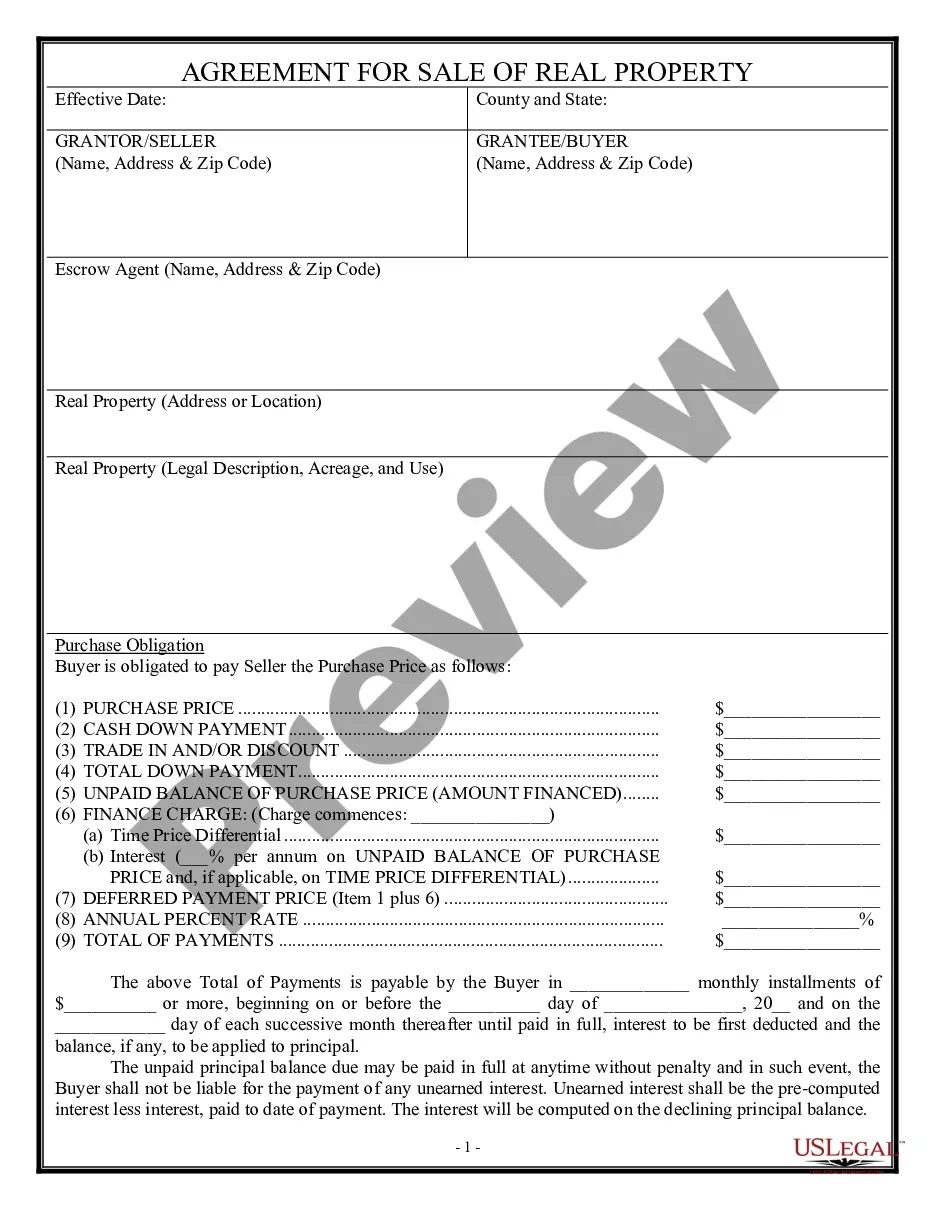

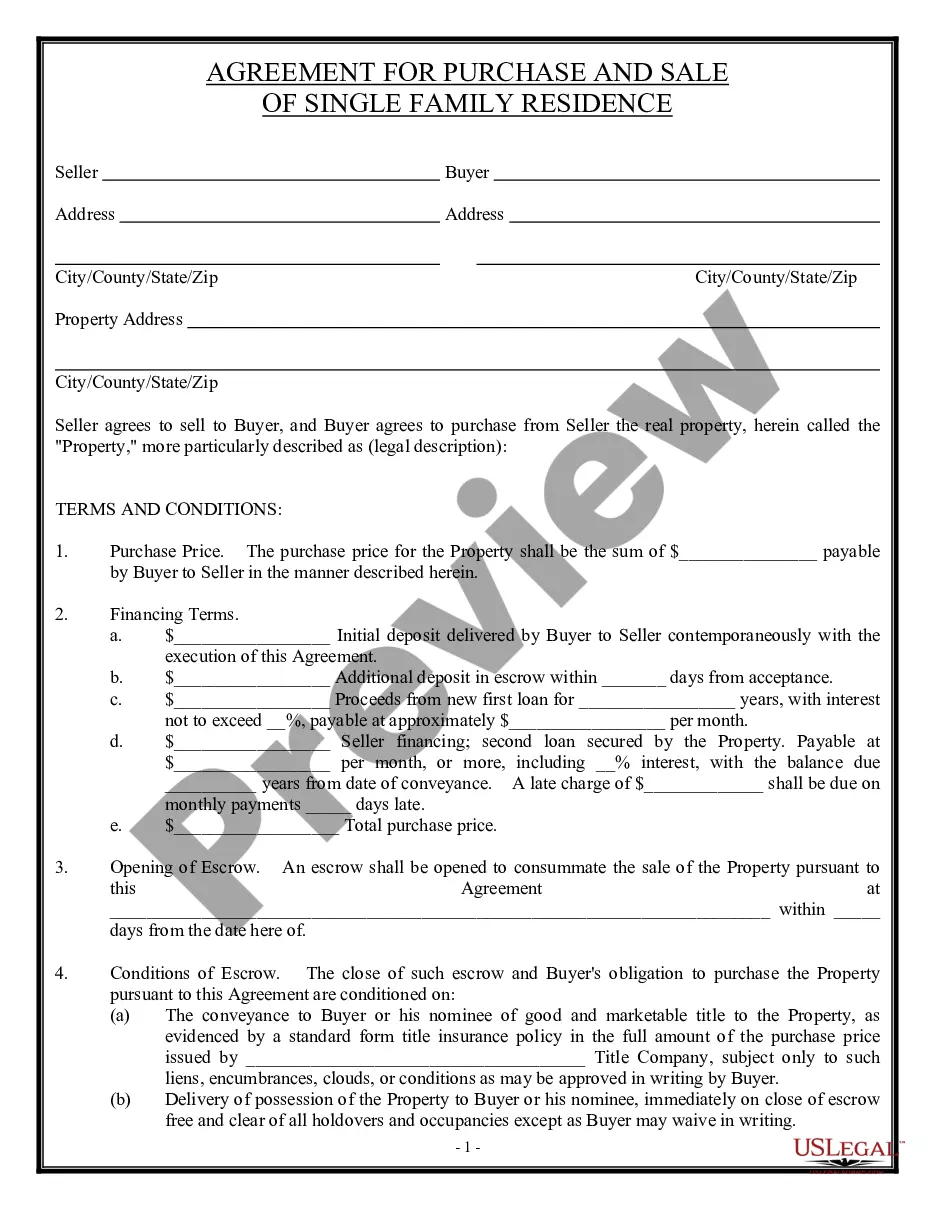

Closure Any Property Formula In Riverside

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Under state law, property is reappraised upon completion of new construction or change of ownership. A supplemental tax bill is an additional property tax bill based on the difference between the prior assessed value and the new assessed value of real property.

Property owners who occupy their homes as their principal place of residence on January 1 may be eligible for an exemption. The Homeowners' Exemption provides for a maximum reduction of $7,000 off the assessed value of your residence.

Unsecured (Personal) Property Taxes are ad-valorem (value based) property taxes that the Office of the Assessor assesses to the owner of record as of January 1 of each year. Because the taxes are not secured by real property such as land, these taxes are called “Unsecured.”

A taxable possessory interest is created when a private party is granted the exclusive use of real property owned by a non-taxable entity. The possession must be independent, durable, and provide a private benefit to the possessor.

A supplemental tax is the result of a reassessment of real property, effective when there is a change in ownership or completion of new construction. A supplemental assessment is the difference between the assessed value on the roll and the assessed value as of a supplemental event.

Payments can also be made by credit card using our telephone payment system. Call our office at (951) 955-3900 or (877) 748-2689 for those taxpayers residing in the desert area and listen to the option, "Payment By Credit Card". You must use a "touch tone" (NOT "PULSE") telephone to access the payment options.

A party seeking a continuance of the date set for trial, whether contested or uncontested or stipulated to by the parties, must make the request for a continuance by a noticed motion or an ex parte application under the rules in chapter 4 of this division, with supporting declarations.

This rule is essentially forcing parties to try to settle issues in their case before going to trial. If Local Rule 5153 is not complied with, the Court will not allow your case to go forward until these procedures are met.

Persons intending to appear remotely shall notify all opposing parties of their intention before the hearing. That notice may be given informally, including by telephone, email, or text message. No advance notice to the court of the intention to appear remotely is required prior to the date of the hearing.

Riverside Superior Court Local Rule 3116 provides: Unless otherwise specified in the Order to Show Cause, any response in opposition to an Order to Show Case (a) shall be in the form of a written declaration and (b) shall be filed no less than four court days before the hearing on the Order to Show Cause.