Sell Closure Property With Example In Florida

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

If the seller intentionally leaves personal property behind, it could be considered “abandoned.” That means you now own all that stuff, and you're on the hook for cleaning it out.

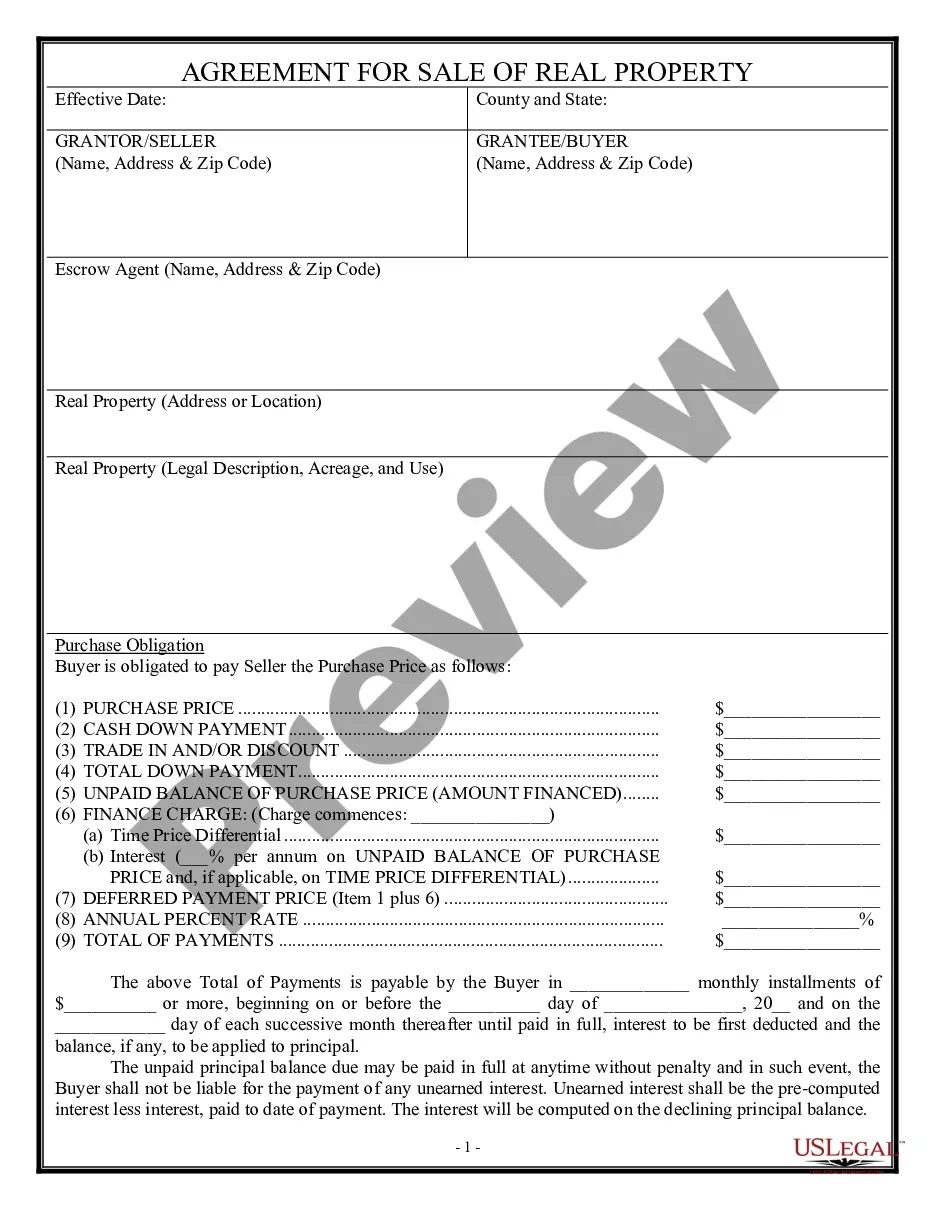

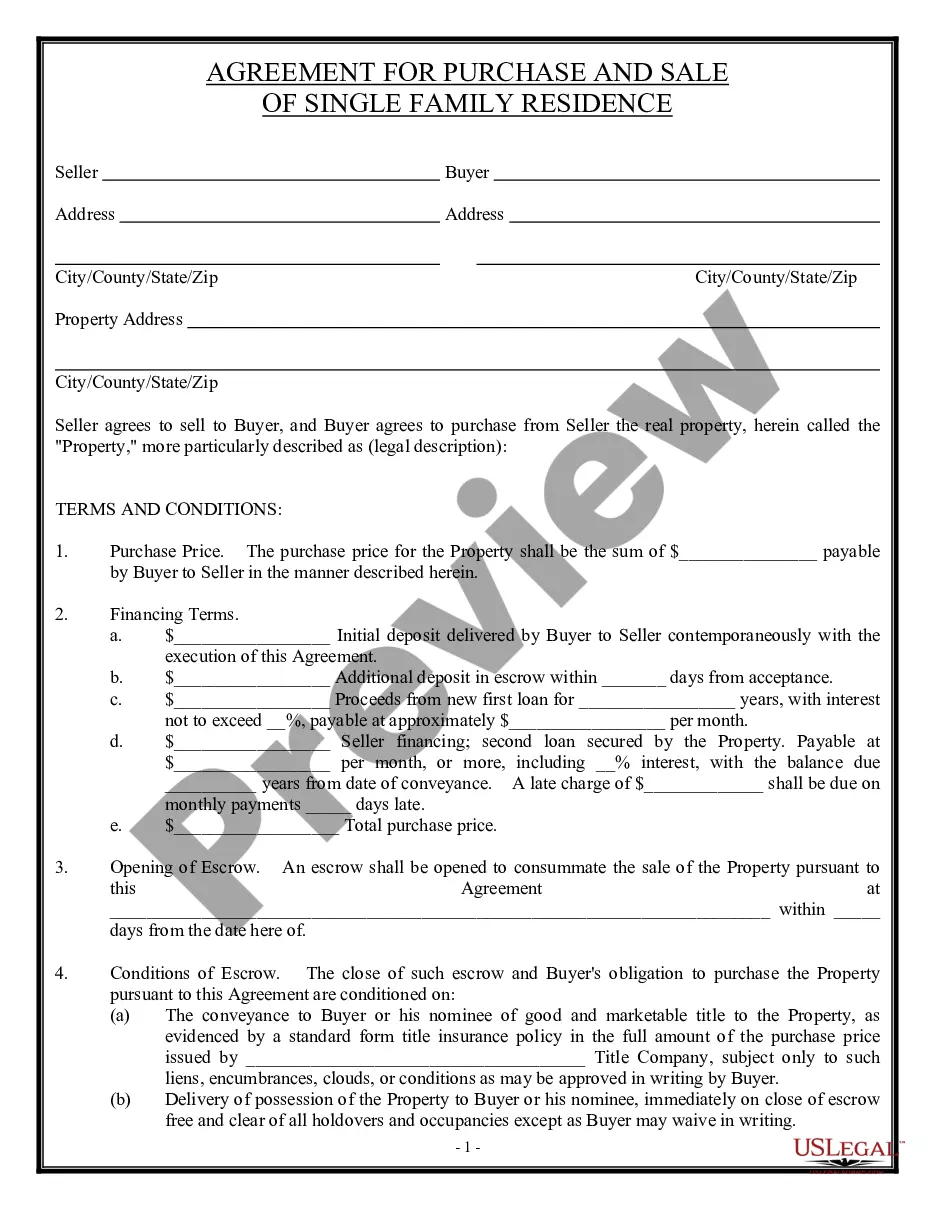

In Florida, the seller typically bears the responsibility for paying property taxes up to the date of closing. This means that the seller is accountable for the portion of property taxes that have accrued during their ownership of the property.

For residential real estate in South Florida, a general timeline for a real estate closing is 30 to 60 days. In other words, it typically takes somewhere between one month and two months from the date an agreement is reached until a residential real estate transaction is finalized (closed).

A closing is the finalization of a real estate transaction, during which ownership of the property transfers from the seller to the buyer. At this stage, all documents are signed, and funds are exchanged. The buyer typically receives the keys to their new property on the closing date.

In Florida, lenders may foreclose on a mortgage in default by using the judicial foreclosure process. This is commenced by filing a lawsuit in the Circuit Court in the county where the property being foreclosed is located.

The sale is an auction, which is open to the public. At the sale, the lender usually makes a credit bid. The lender can bid up to the total amount owed, including fees and costs, or it may bid less. If the lender is the highest bidder, the property becomes "Real Estate Owned" (REO).

In Florida, surplus funds generally belong to the homeowner whose property was foreclosed upon. However, other creditors may make claims to these funds, which can affect how and when they are distributed.

In Florida, like many other states, the foreclosure process typically commences after a specific period of consecutive missed payments, normally ranging from three to six months.

Typically closing on a home takes anywhere from 30-45 days. The National Association of Realtors reports that the average time to close on a single-family home is around 43 days. During this time, each party will complete critical activities to ensure that the home closes promptly.

Foreclosure Process: If the buyer defaults on the contract, the seller may need to go through a foreclosure process to regain possession of the property. This process can be lengthy, costly, and more complicated than evicting a tenant, as the buyer holds an equitable interest in the property.