Closing Any Property Without Permission In Cook

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The closing process typically begins with reviewing and reconciling accounts to identify discrepancies and errors. Adjusting entries are then recorded to account for accruals, deferrals, depreciation, and other adjustments necessary to reflect the correct financial position.

The closing process involves four specific steps: Step 1: Close revenue accounts to Income Summary. Income Summary is a temporary account used during the closing process. Step 2: Close expense accounts to Income Summary. Step 3: Close Income Summary to Retained Earnings. Step 4: Close dividends to Retained Earnings.

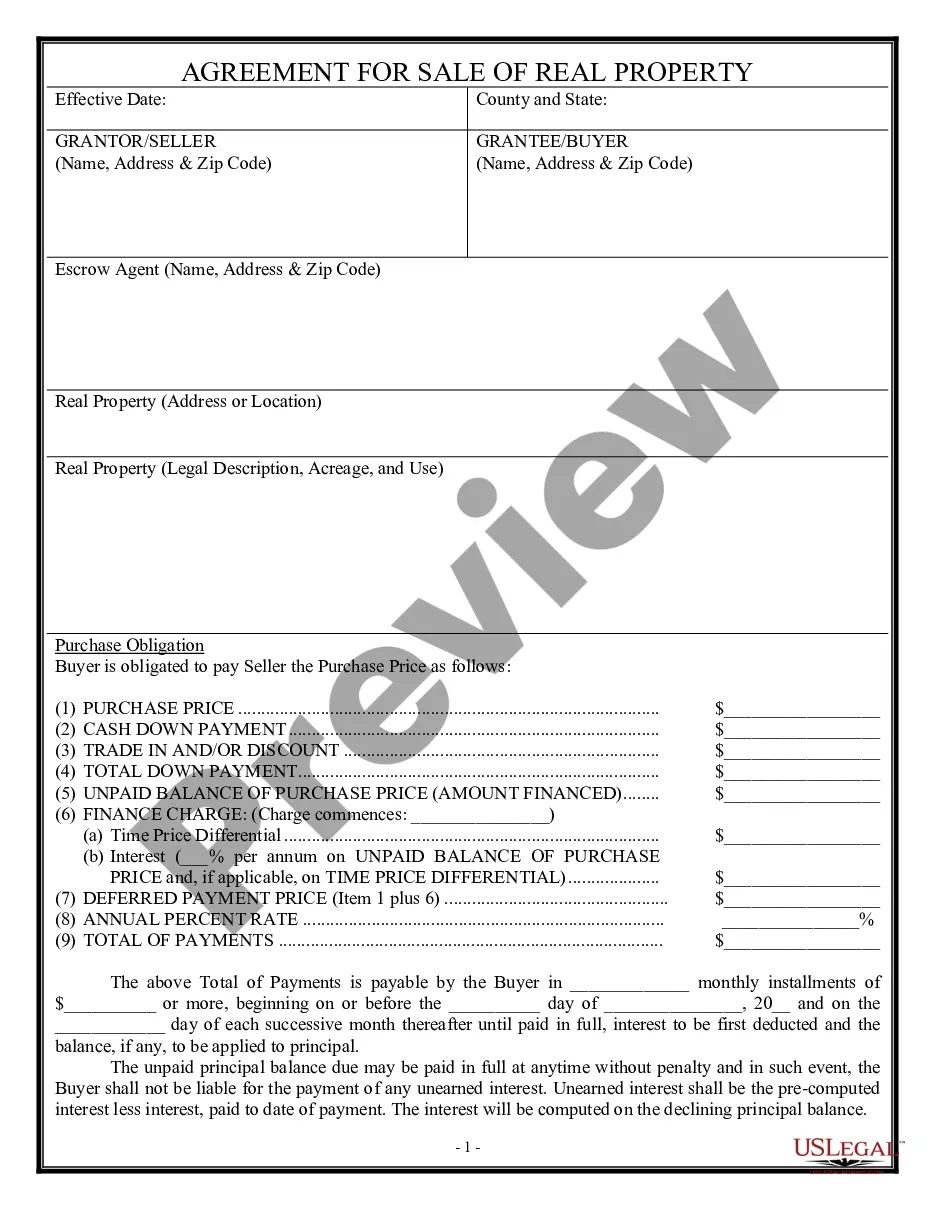

If a person other than the owner attempts to sell the property, the transaction is considered illegal. This type of sale falls under fraudulent transactions and can be nullified under Philippine law. Even if the buyer was unaware that the seller was not the legitimate owner, the sale would still be void.

What Are the Steps to Financial Close? Identify transactions and record them in a journal. Post to the general ledger. Prepare an unadjusted trial balance. Reconcile debits and credits. Create adjusting journal entries. Run an adjusted trial balance and financial statements. Close the books and generate financial reports.

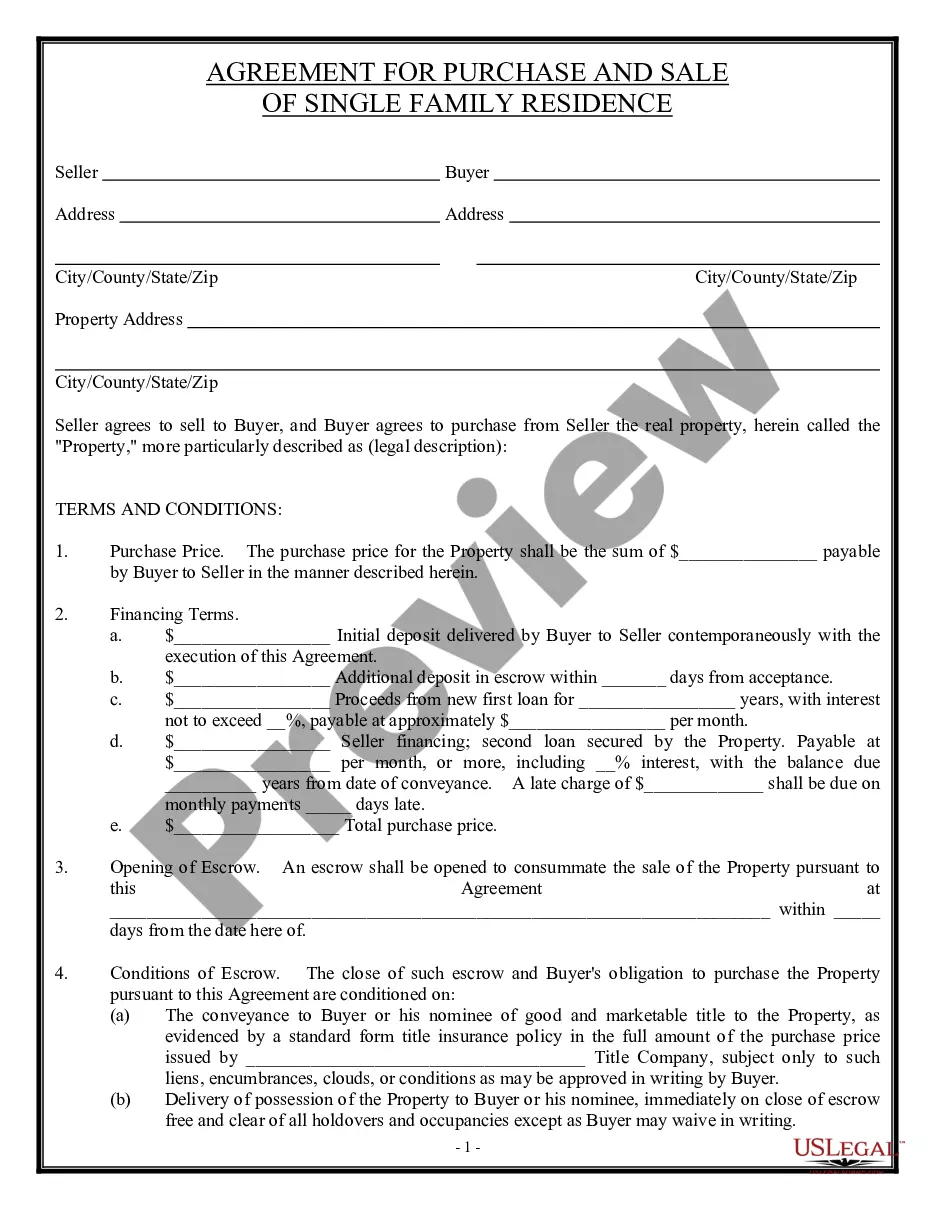

Can a California home seller require that a buyer must physically view the home being sold? Sure, why not? There is no legal restriction on such a clause. The seller probably wants to be certain that the buyer is serious, won't back out during the sale, and won't sue the seller for defects discovered after closing.

Obtain Authorization: If you're interested in renting out a property that you don't own, seek explicit permission and authorization from the property owner. Clarify Agreements: Document any agreements in writing and ensure they're legally binding to protect both parties involved.

If you've financed your home, wait at least 12 months before turning your primary residence into a rental. While some lenders make an exception, waiting 12 months before turning your residence into a rental property is a common rule.

Yes you can Airbnb without owning any property. It's called subletting. But it's not illegal youMoreYes you can Airbnb without owning any property. It's called subletting. But it's not illegal you just need the landlord's permission. This is my area of expertise.

The seller does not have to be present at the buyers' closing.