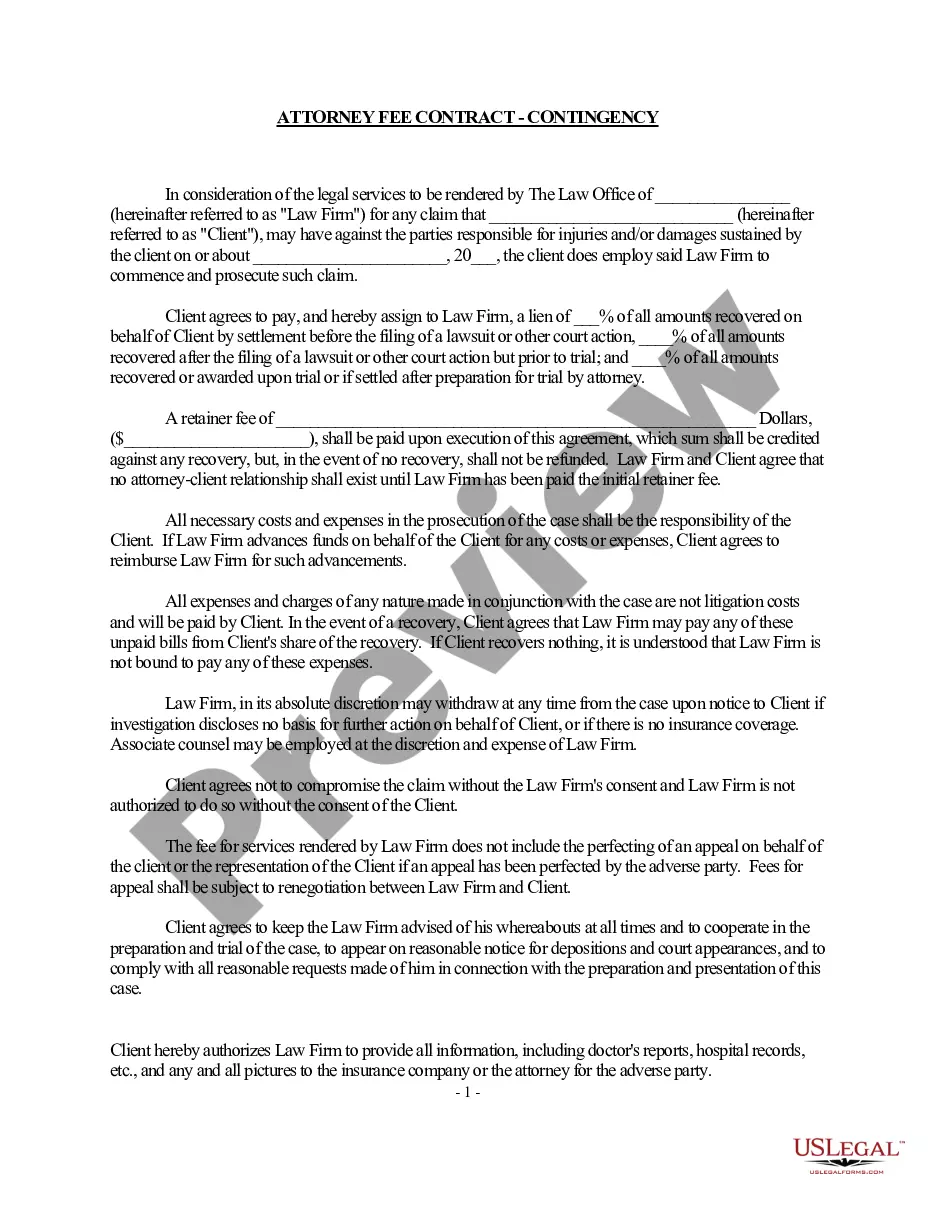

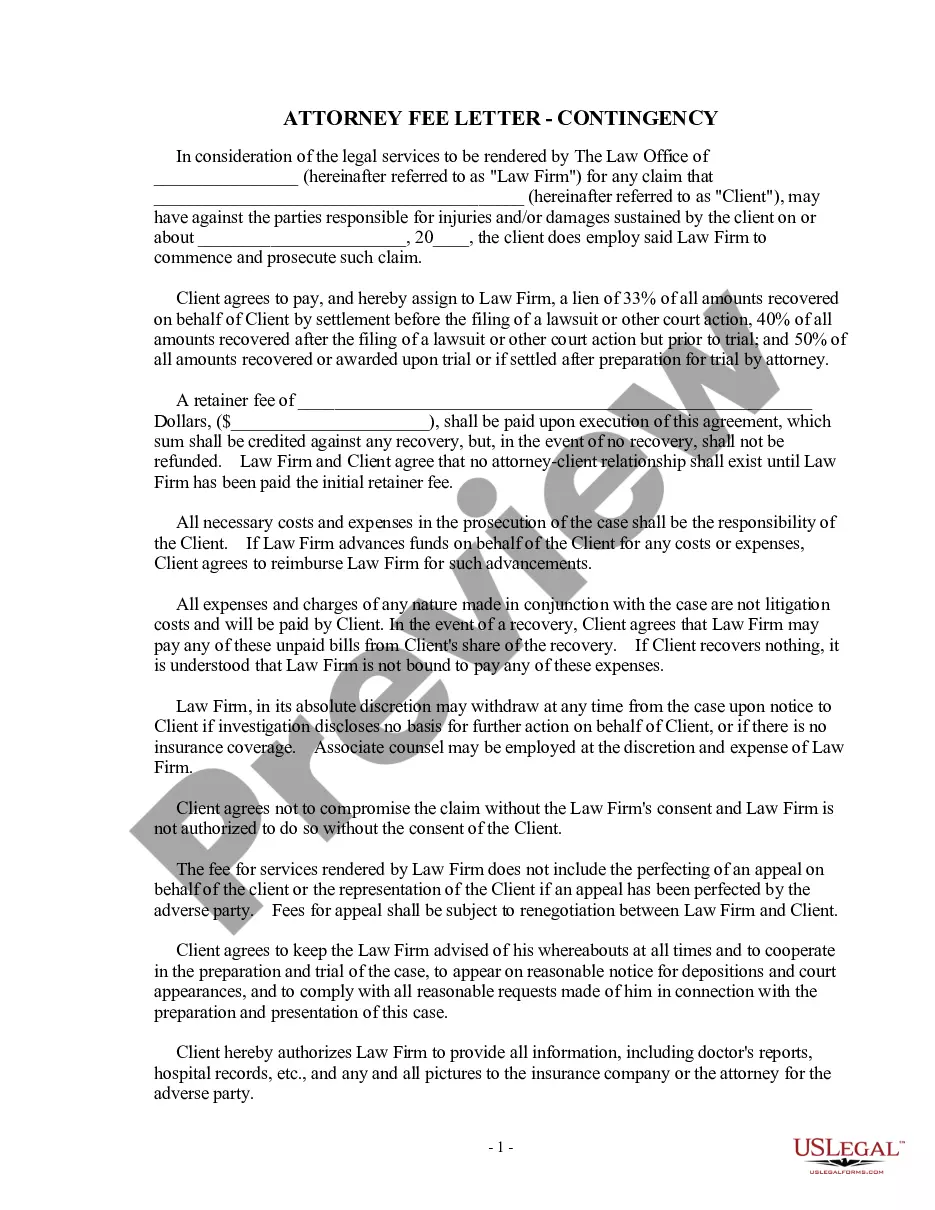

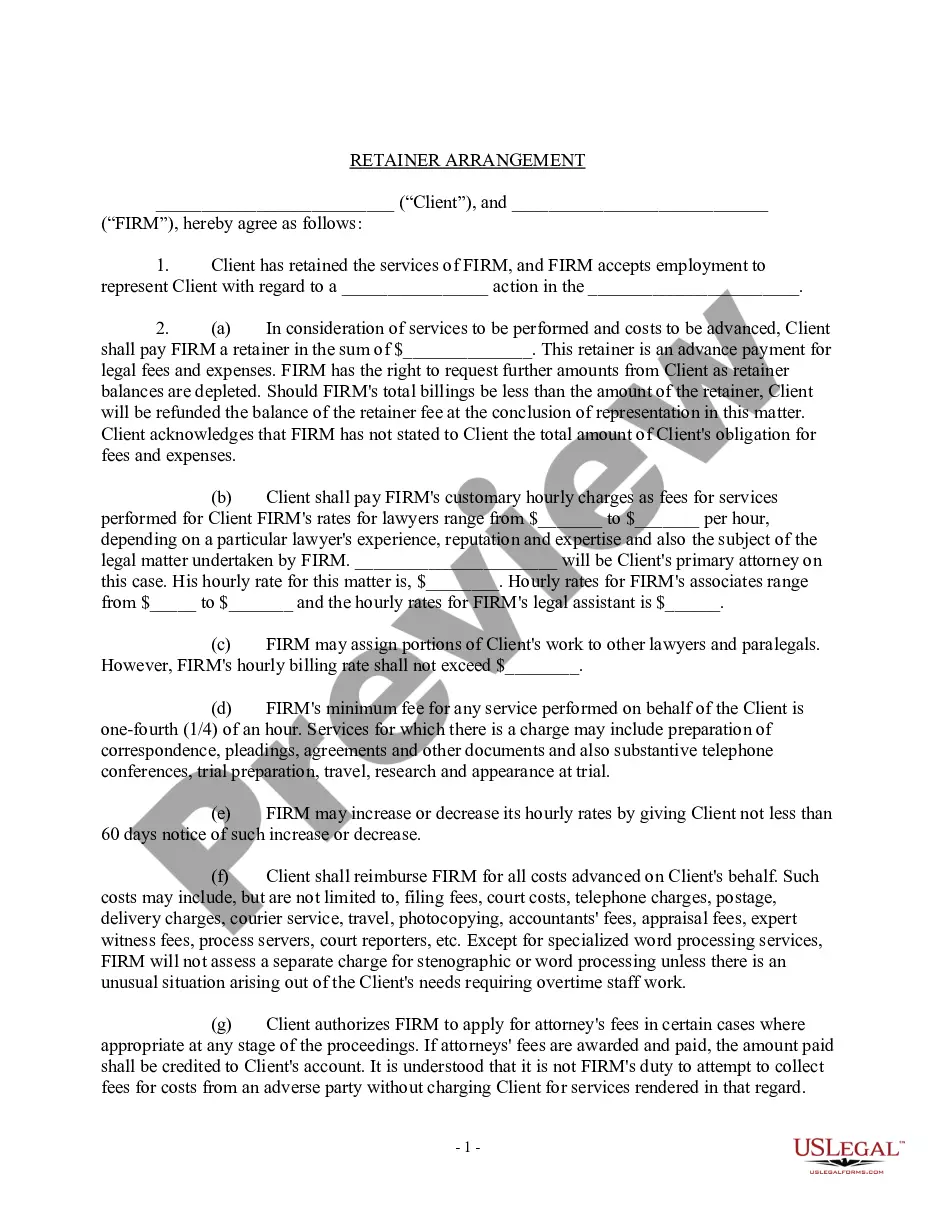

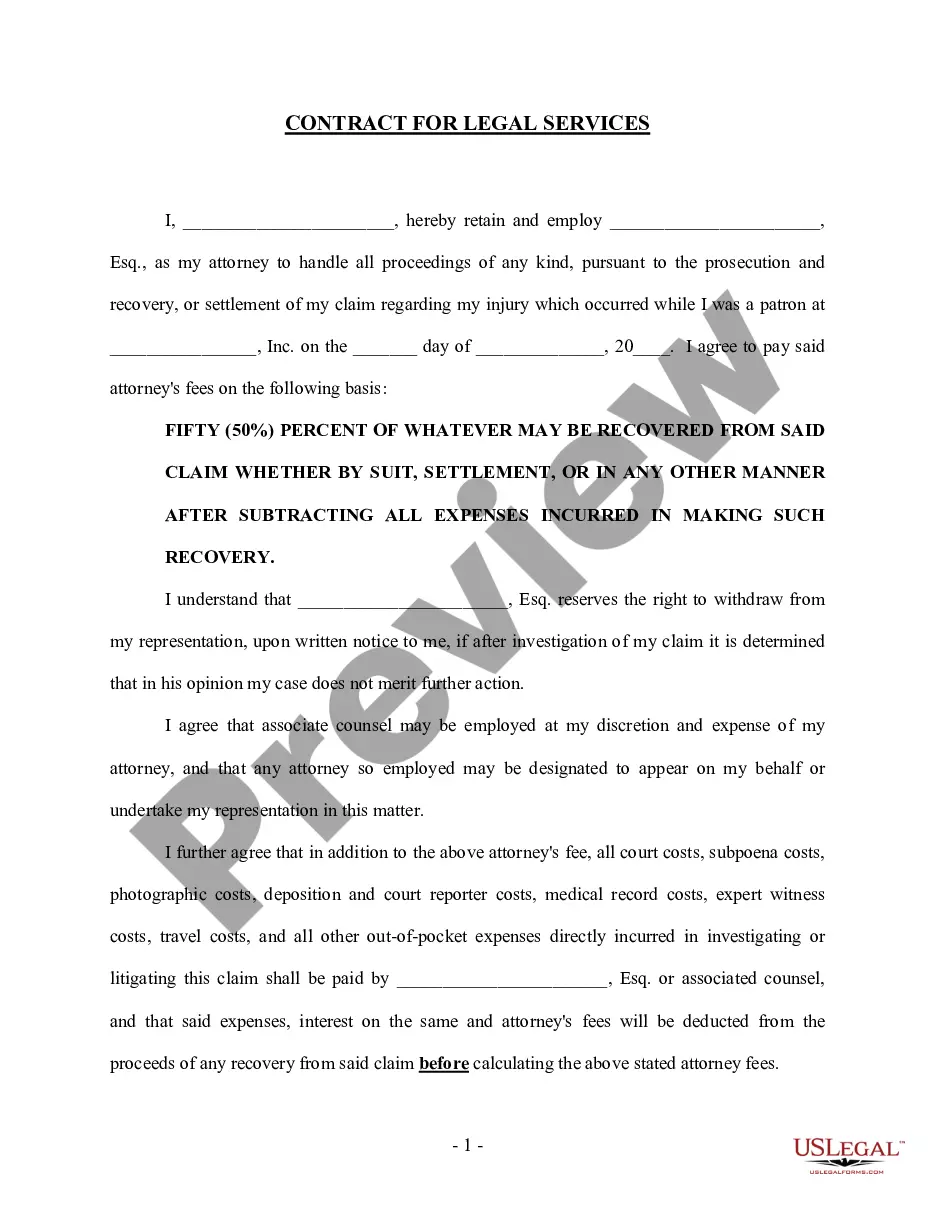

Contingency Fee For Erc In Cook

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Reporting ERC on Tax Returns Form 941-X: To claim the ERC, you generally need to file an amended federal employment tax return. This is done using Form 941-X for each applicable quarter. This form reports wages and health insurance costs related to the ERC.

Going forward, the only way to apply for the ERC is to file an amended Form 941X (Quarterly Federal Payroll Tax Return) for the quarters during which the company was an eligible employer.

Because the ERC is considered an income-related grant under IAS 20, an entity may elect to present the income in one of two ways: (1) gross as a grant or other income item, or (2) net as a deduction from the expense category in which the reporting entity reports employment taxes (typically employee compensation).

The statute of limitations (SOL) on amending payroll tax returns (Form 941-X) for 2021 ends on April 15, 2025, and the ERC ends on the same date.

It provides a safety net for unexpected expenses and ensures the project stays on track, both in terms of budget and timeline. The recommended percentage for a contingency fund is between 5-10% of the total budget, but this may vary depending on project complexity and past experiences.

In most cases, ETH and ERC-20 withdrawals normally should take no longer than two hours to be processed.

Credit amount The total ERC benefit per employee can be up to $26,000 ($5,000 in 2020 and $7,000 per quarter in 2021).

The statute of limitations (SOL) on amending payroll tax returns (Form 941-X) for 2021 ends on April 15, 2025, and the ERC ends on the same date. Legislators attempted to end the ERC on January 31, 2024, as part of H.R. 7024, but this bill failed in a Senate roll call vote in early August 2024.

Fax the signed copy of your return using your computer or mobile device to the IRS's ERC claim withdrawal fax line at 855-738-7609. This is your withdrawal request. Keep your copy with your tax records. Note: This fax line is only for ERC claim withdrawals.

You may qualify for ERC if your business or organization experienced a significant decline in gross receipts during 2020 or a decline in gross receipts during the first three quarters of 2021.