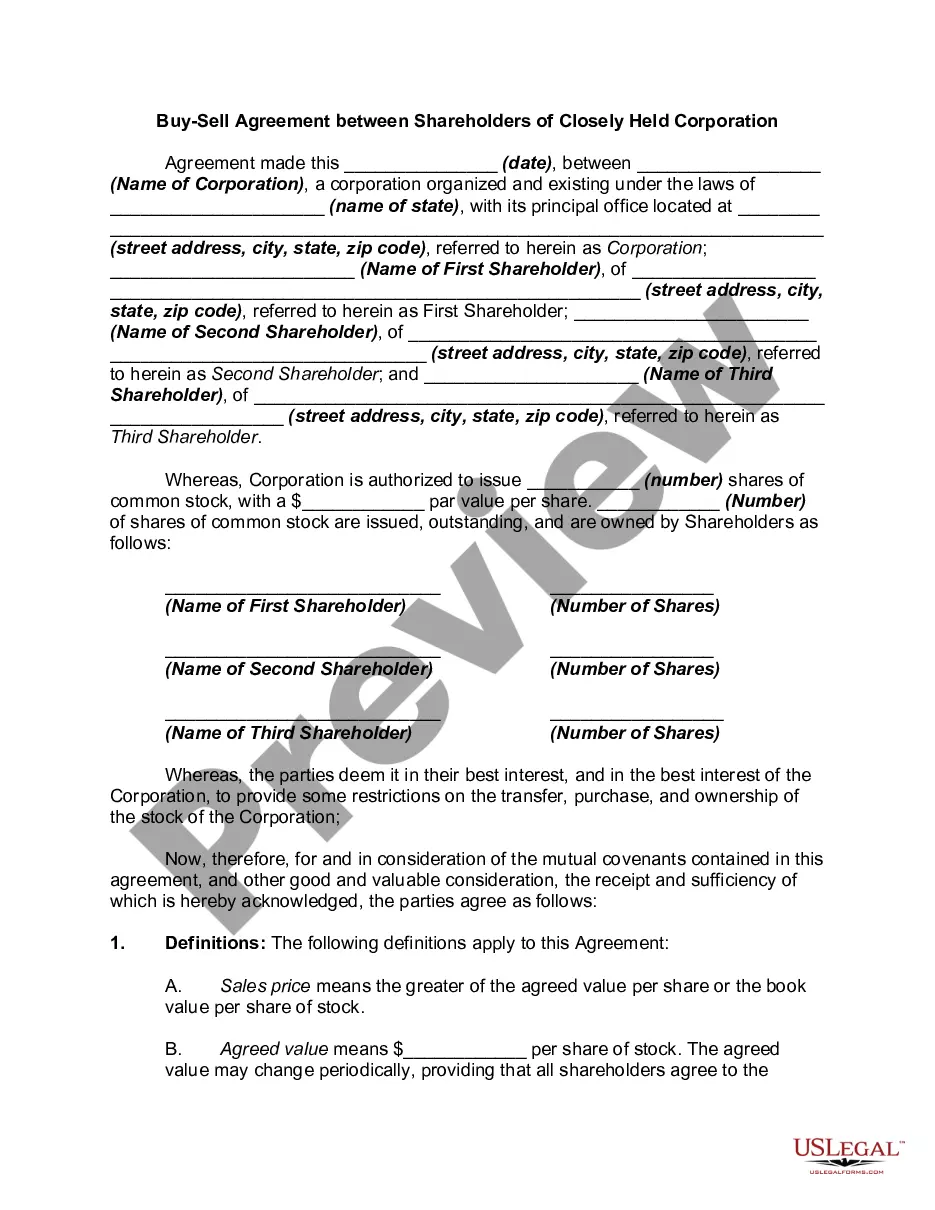

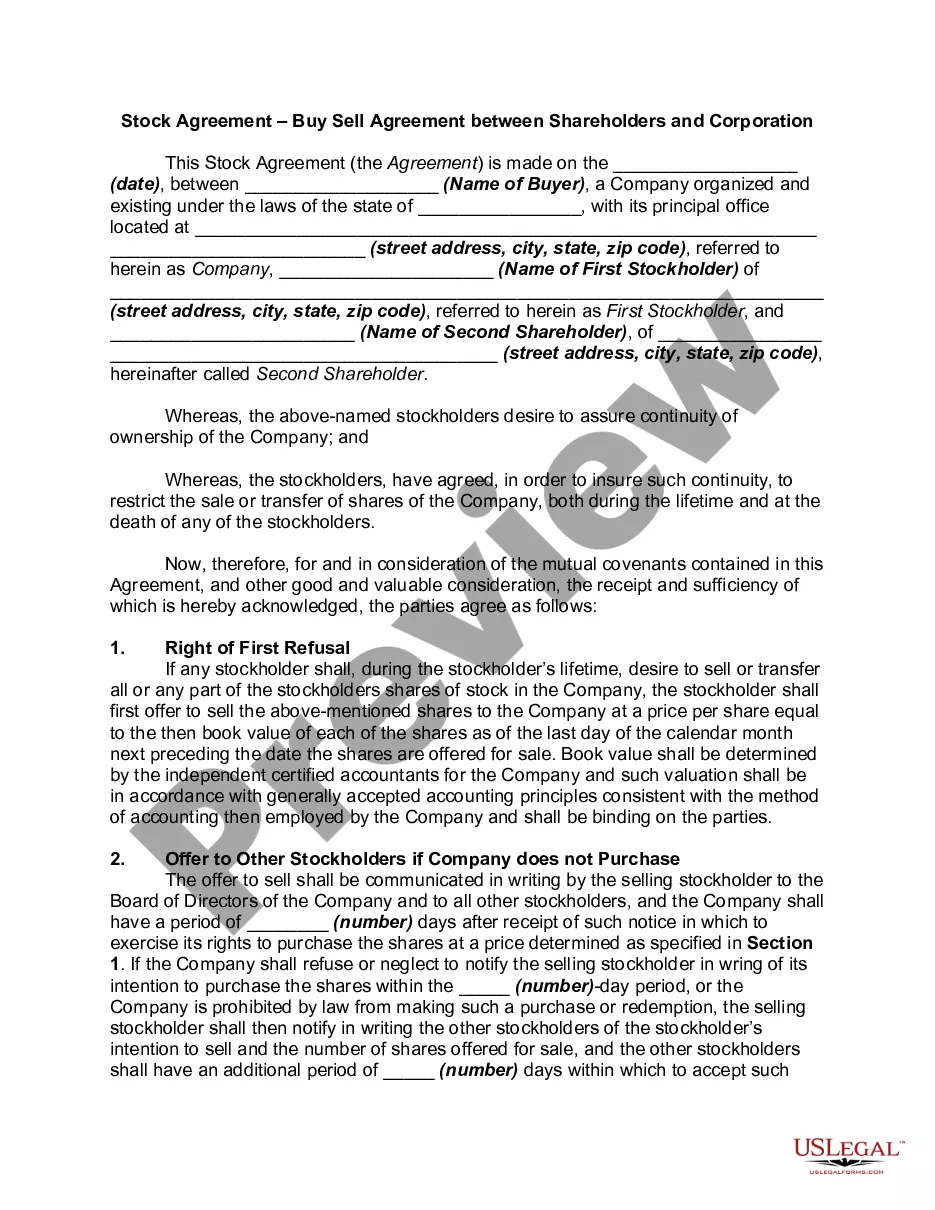

The purpose of this agreement is to provide for the sale by a stockholder during his/her lifetime, or by a deceased stockholder's estate, and to provide all or a substantial part of the funds for the purchase. The form contains the following provisions: total value of the capital stock, procedure upon the death of a stockholder, and amending procedures for the agreement.

Como Se Compra Una Casa En Short Sale In Wake

Category:

State:

Multi-State

County:

Wake

Control #:

US-00442

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Some lenders may be more willing to negotiate while others have policies. Handling these situations requires patience, persistence, and strong negotiation skills. Short sale negotiations can take time.

The agent represents the seller, not the lender. In a short sale, the offer is negotiated with the seller, just as in a traditional sale. The offer is then submitted to the lender, not for an “acceptance” but for approval of the terms and net proceeds.

While a seller typically pays all real estate agent commissions and other closing costs, in a short sale the seller pays nothing; the lender or bank foots the bill.

Short sale package: The borrower has to prove financial hardship by submitting a financial package to their lender. The package includes financial statements, a letter describing the seller's hardship(s), and financial records, including tax returns, W-2s, payroll stubs, and bank statements.

The most basic is physical selling short or short-selling, by which the short seller borrows an asset (often a security such as a share of stock or a bond) and quickly sells it. The short seller must later buy the same amount of the asset to return it to the lender.

Short sales allow a homeowner to dispose of a property that is losing value. Although they do not recoup the costs of their mortgage, a short sale allows a buyer to escape foreclosure, which can be much more damaging to their credit score.