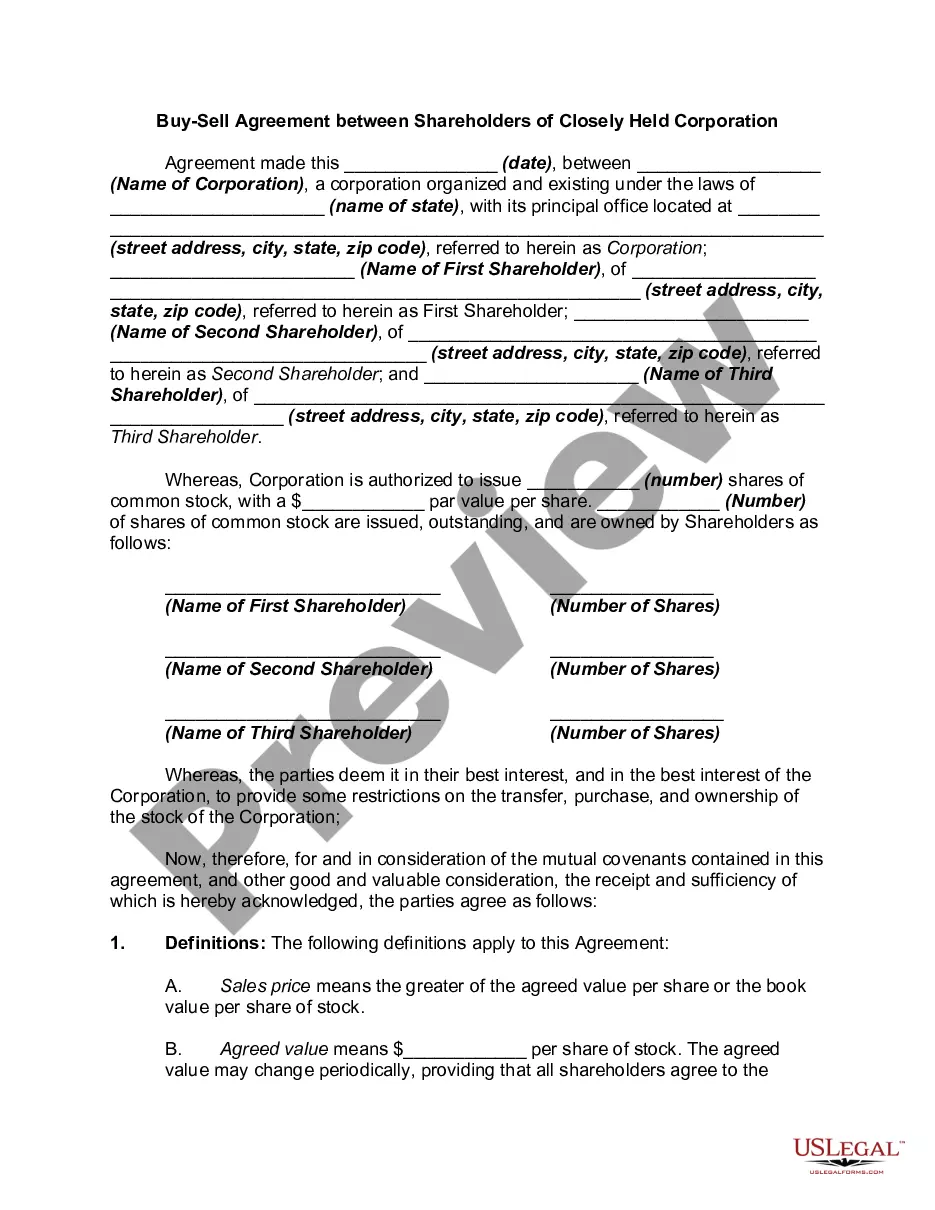

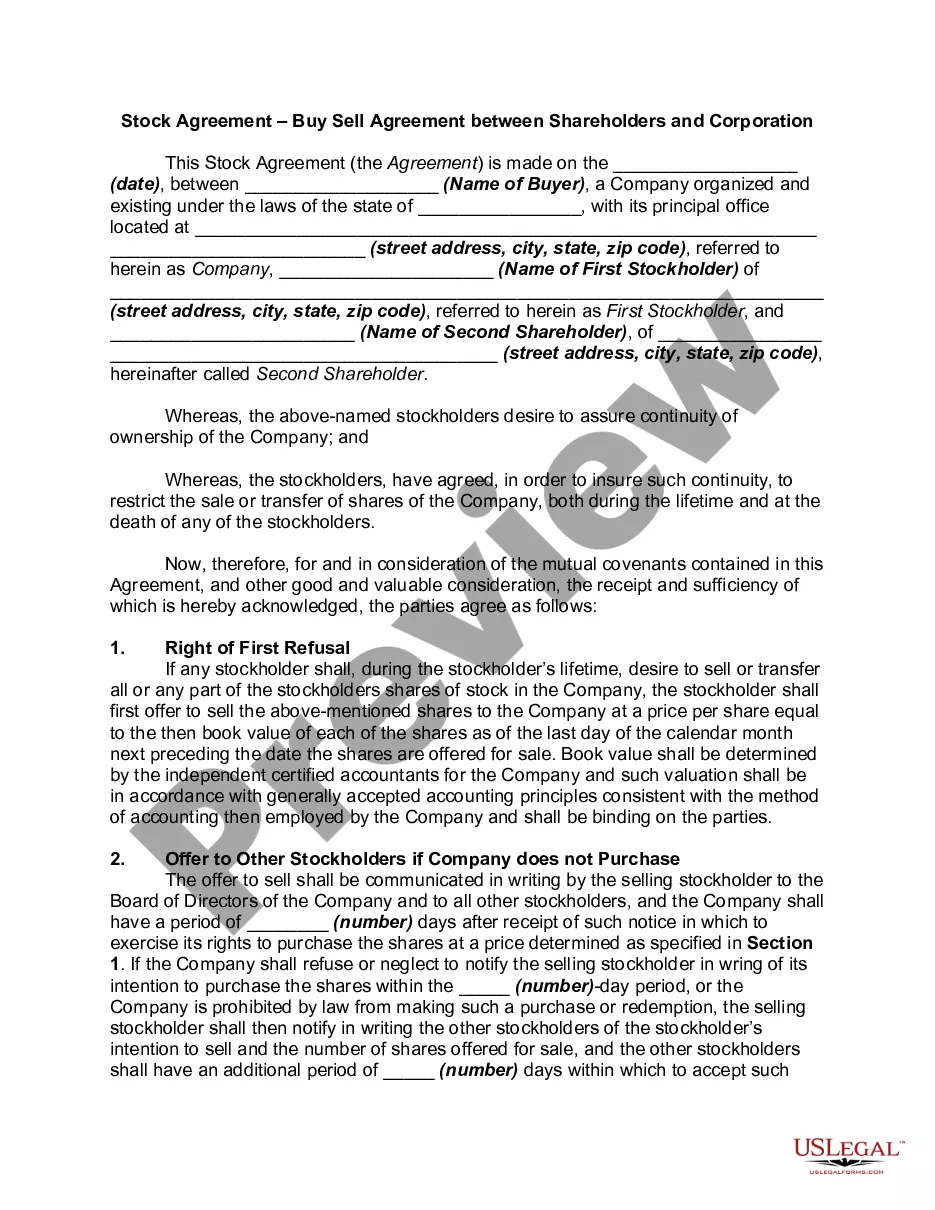

The purpose of this agreement is to provide for the sale by a stockholder during his/her lifetime, or by a deceased stockholder's estate, and to provide all or a substantial part of the funds for the purchase. The form contains the following provisions: total value of the capital stock, procedure upon the death of a stockholder, and amending procedures for the agreement.

Como Se Compra Una Casa En Short Sale In Riverside

Category:

State:

Multi-State

County:

Riverside

Control #:

US-00442

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Short sales allow a homeowner to dispose of a property that is losing value. Although they do not recoup the costs of their mortgage, a short sale allows a buyer to escape foreclosure, which can be much more damaging to their credit score.

The most basic is physical selling short or short-selling, by which the short seller borrows an asset (often a security such as a share of stock or a bond) and quickly sells it. The short seller must later buy the same amount of the asset to return it to the lender.

What Are the Downsides of Using a Short Sale to Avoid a Foreclosure for Sellers? You Might Face a Deficiency Judgment After a Short Sale. Short Sale Tax Implications Following a Short Sale. A Short Sale Will Damage Your Credit Scores. Finding a New Home. Foreclosure Might Be a Better Option.

A short sale is a transaction in which the lender, or lenders, agree to accept less than the mortgage amount owed by the current homeowner. In some cases, the difference is forgiven by the lender, and in others the homeowner must make arrangements with the lender to settle the remainder of the debt.

A short sale is a transaction in which the lender, or lenders, agree to accept less than the mortgage amount owed by the current homeowner. In some cases, the difference is forgiven by the lender, and in others the homeowner must make arrangements with the lender to settle the remainder of the debt.

A short sale occurs when a homeowner sells their property for less than what they owe on their mortgage. For sellers, it's a way to avoid foreclosure if they can no longer afford their mortgage payments.

Short term sales means sales that last for no longer than one year.