Claim Dependent On Taxes Canada In Wayne

Description

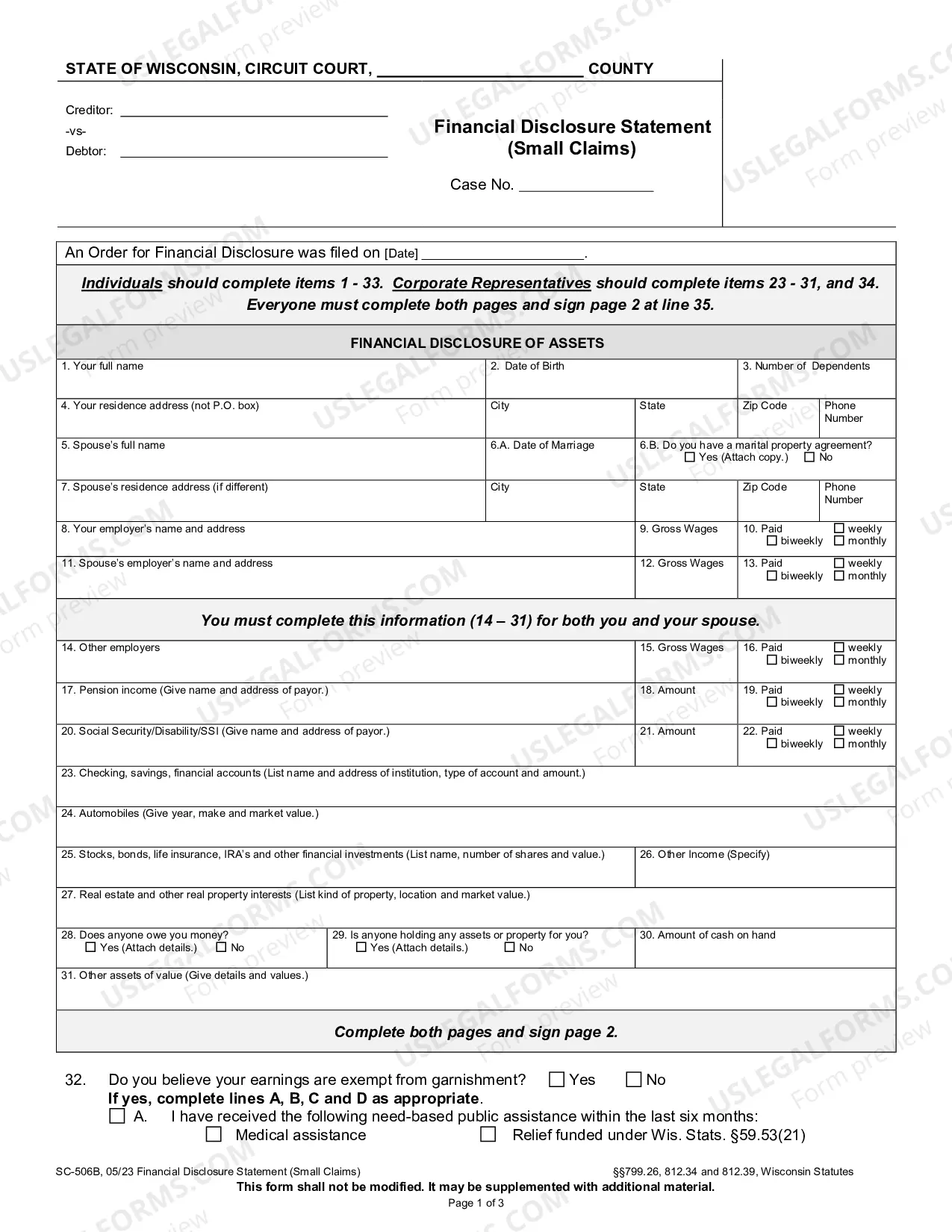

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

In addition, the dependant must also be one of the following persons by blood, marriage, common-law partnership or adoption: your parent or grandparent. your child, grandchild, brother, or sister under 18 years of age.

Unfortunately you cannot add a parent as a dependant under the PSHCP. The only eligible dependants are the employee's spouse/partner, children, and children of the spouse/partner.

Whatever the case, when it comes to your taxes, the rule is that you must be a resident of Canada in order to claim personal amounts for your dependants. The only exception is if the Canadian income on your return represents 90% or more of your total world income.

An individual claimed as a dependent must be a citizen, national, or resident of the United States, or a resident of Canada or Mexico.

Your child, grandchild, brother, or sister under the age of 18 (over 18 qualifies if the dependant is physically or mentally impaired)

Here's how it works: If 90% or more of your worldwide income for the tax year comes from Canadian sources, you may be eligible for the basic personal amount (the most common non-refundable tax credit) and other credits that residents are typically entitled to.

Your parent or grandparent. your child, grandchild, brother, or sister under 18 years of age. your child, grandchild, brother, or sister 18 years of age or older with an impairment in physical or mental functions.

Claiming the Canada caregiver amount for spouse or common-law partner, or eligible dependant age 18 or older. You may be entitled to claim an amount of $2,616 in the calculation of line 30300 if your spouse or common-law partner has an impairment in physical or mental functions.

Dependent adults are those who have a mental or physical limitation and depend on one or more persons for care or support. Foreign national dependent adults may be exempt from the travel restrictions if they are either: fully vaccinated, or. travelling together with their parent, step-parent, guardian or tutor.