Promissory Note Calculator With Balloon Payment

Description

How to fill out Promissory Note - Balloon Note?

Regardless of whether it is for commercial reasons or personal affairs, everyone must handle legal issues at some point in their lives.

Filling out legal paperwork requires meticulous care, beginning with choosing the appropriate template.

Once it is downloaded, you can fill out the document using editing software or print it and complete it by hand. With an extensive US Legal Forms catalog available, you will never have to waste time searching for the appropriate template online. Utilize the library’s straightforward navigation to discover the right document for any circumstance.

- Obtain the template you require using the search bar or catalog browsing.

- Review the document’s details to make sure it corresponds to your circumstances, state, and county.

- Select the document’s preview to examine it.

- If it is not the right document, return to the search feature to locate the Promissory Note Calculator With Balloon Payment template you need.

- Acquire the template if it satisfies your requirements.

- If you have a US Legal Forms account, simply click Log in to access previously saved documents in My documents.

- In case you do not have an account yet, you can obtain the document by clicking Buy now.

- Select the suitable payment option.

- Complete the profile registration form.

- Choose your payment method: either a credit card or PayPal account.

- Select the file type you wish and download the Promissory Note Calculator With Balloon Payment.

Form popularity

FAQ

Balloon payments are not illegal; however, they must comply with state and federal regulations. Borrowers should be aware of the risks involved, and lenders must disclose all terms clearly. Utilizing a promissory note calculator with balloon payment can aid in understanding these terms and help you make informed decisions.

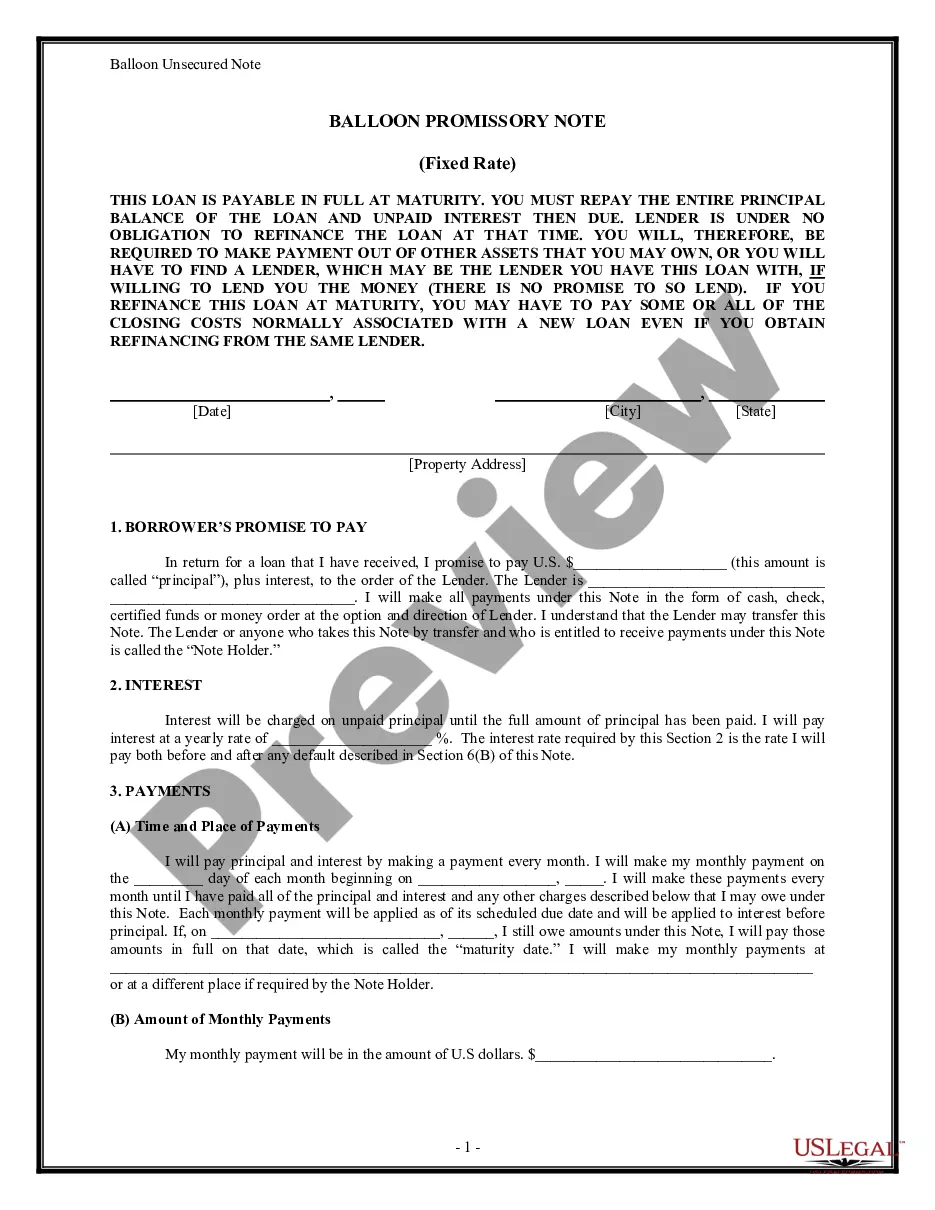

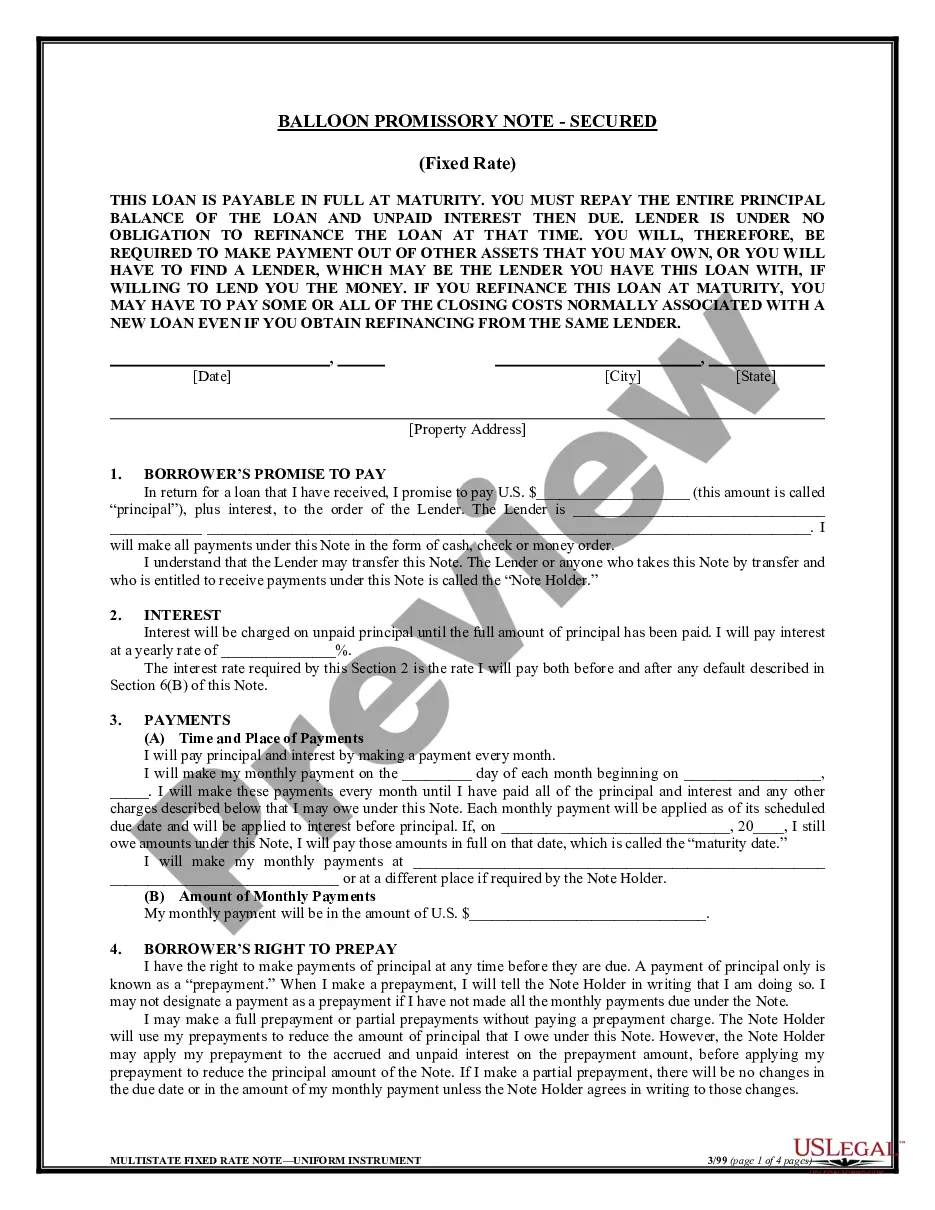

Example of a Balloon Loan Let's say a person takes out a $200,000 mortgage with a seven-year term and a 4.5% interest rate. Their monthly payment for seven years is $1,013. At the end of the seven-year term, they owe a $175,066 balloon payment.

Balloon Loan Your loan has a balloon payment. At the end of the loan term, any balance remaining will have to be paid. In the case of a balloon loan, often very little, if any, of the loan balance is paid down, therefore, the last payment, the balloon payment can be most of the initial loan balance.

Balloon payment schedule A 30/5 structure means the lender calculates your monthly payments as if you'll be repaying the loan for 30 years, but you actually only make those payments for five years. At the end of the five-year (60-month) term, you'll repay the remaining principal, or $260,534.53, as a lump sum.

We can use the below formula to calculate the future value of the balloon payment to be made at the end of 10 years: FV = PV*(1+r)n?P*[(1+r)n?1/r] The rate of interest per annum is 7.5%, and monthly it shall be 7.5%/12, which is 0.50%.

A balloon payment is the final amount due on a loan that is structured as a series of small monthly payments followed by a single much larger sum at the end of the loan period.