Sample Overpayment Letter To Customer With Credit Card In Contra Costa

Description

Form popularity

FAQ

The details of the transaction are as follows: • Date of transaction: INSERT DATE OF TRANSACTION • Amount of transaction:INSERT AMOUNT OF TRANSACTION • Name of merchant: INSERT NAME OF SELLER • Reasons for the request for chargeback: FOR EXAMPLE you did not receive the goods, they were faulty etc Please let me ...

To trigger the federal requirements, the written notice must provide the creditor with the following: (1) account identification infor mation, (2) identification of the specific bill (or bills) in dispute, (3) a statement that the debtor believes the bill is in error, and (4) the reason(s) why the bill is disputed.

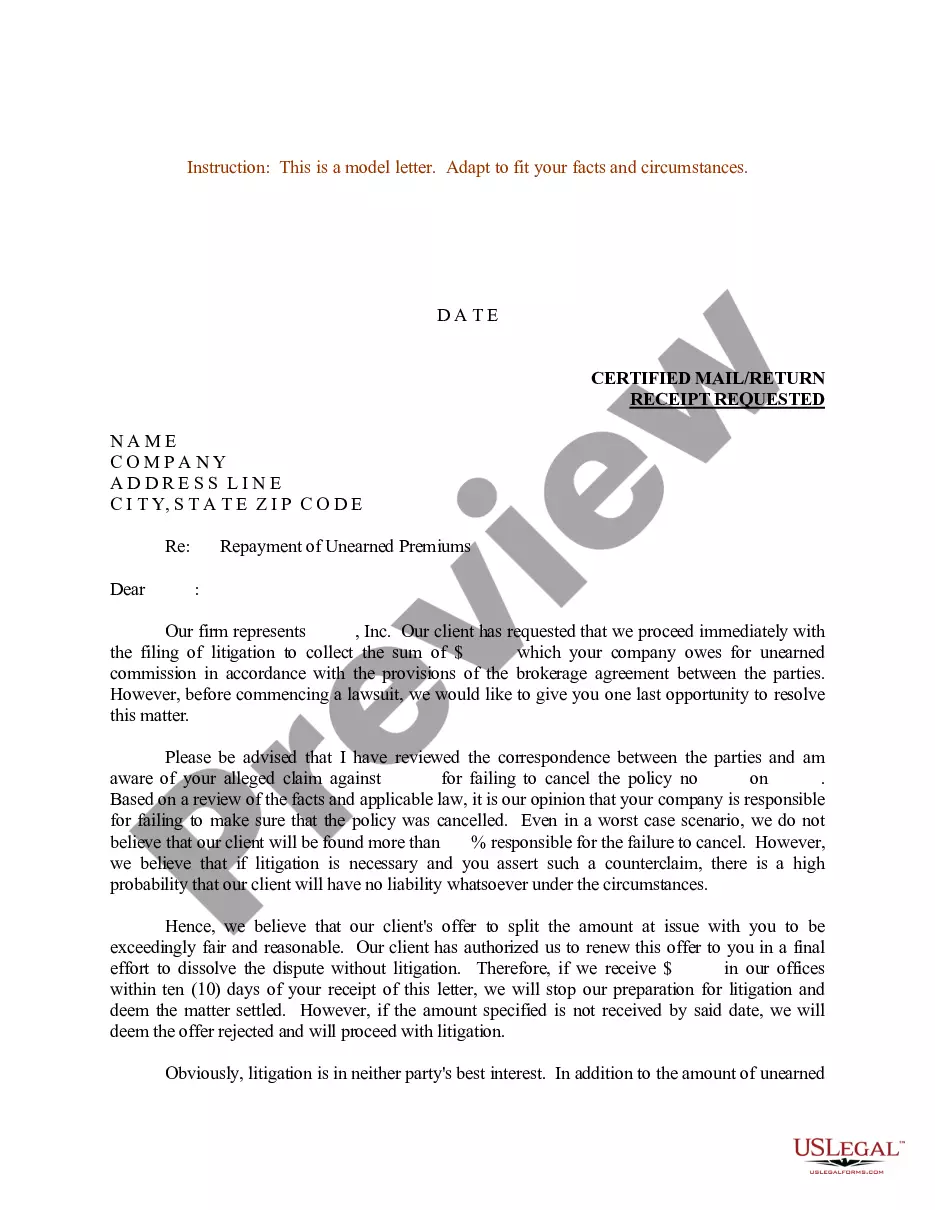

1. Confirm the overpayment with Accounting/Risk management/Operations, before proceeding with any negotation. 2. Offer to credit the overpay to their next bill, once confirmed and while determining whether “overpay” is an acceptable refund policy....

When a business receives an overpayment, it is required to notify the customer and to offer to refund the excess amount or apply it as a credit toward a future invoice. The agreed-upon resolution should be documented and implemented quickly.

Your letter should identify each item you dispute, state the facts, explain why you dispute the information, and ask that the business that supplied the information take action to have it removed or corrected. You may want to enclose a copy of your report with the item(s) in question circled.

Your letter should identify each item you dispute, state the facts, explain why you dispute the information, and ask that the business that supplied the information take action to have it removed or corrected. You may want to enclose a copy of your report with the item(s) in question circled.

Dear Sir or Madam: I am the victim of identity theft. My ATM/Debit card was lost or stolen or was used for an unauthorized transaction on insert date. I did not authorize any transactions on or after this date, and I did not authorize anyone else to use my ATM/Debit card in any way.

Contact your credit card issuer: You can reach your credit card issuer by calling the number on the back of your card, emailing customer service, using the app to report the issue or submitting a written dispute.

2) What is the 609 loophole? The “609 loophole” is a misconception. Section 609 of the Fair Credit Reporting Act (FCRA) allows consumers to request their credit file information. It does not guarantee the removal of negative items but requires credit bureaus to verify the accuracy of disputed information.