Purchase Of Asset Double Entry In San Diego

Category:

State:

Multi-State

County:

San Diego

Control #:

US-00418

Format:

Word;

Rich Text

Instant download

Description

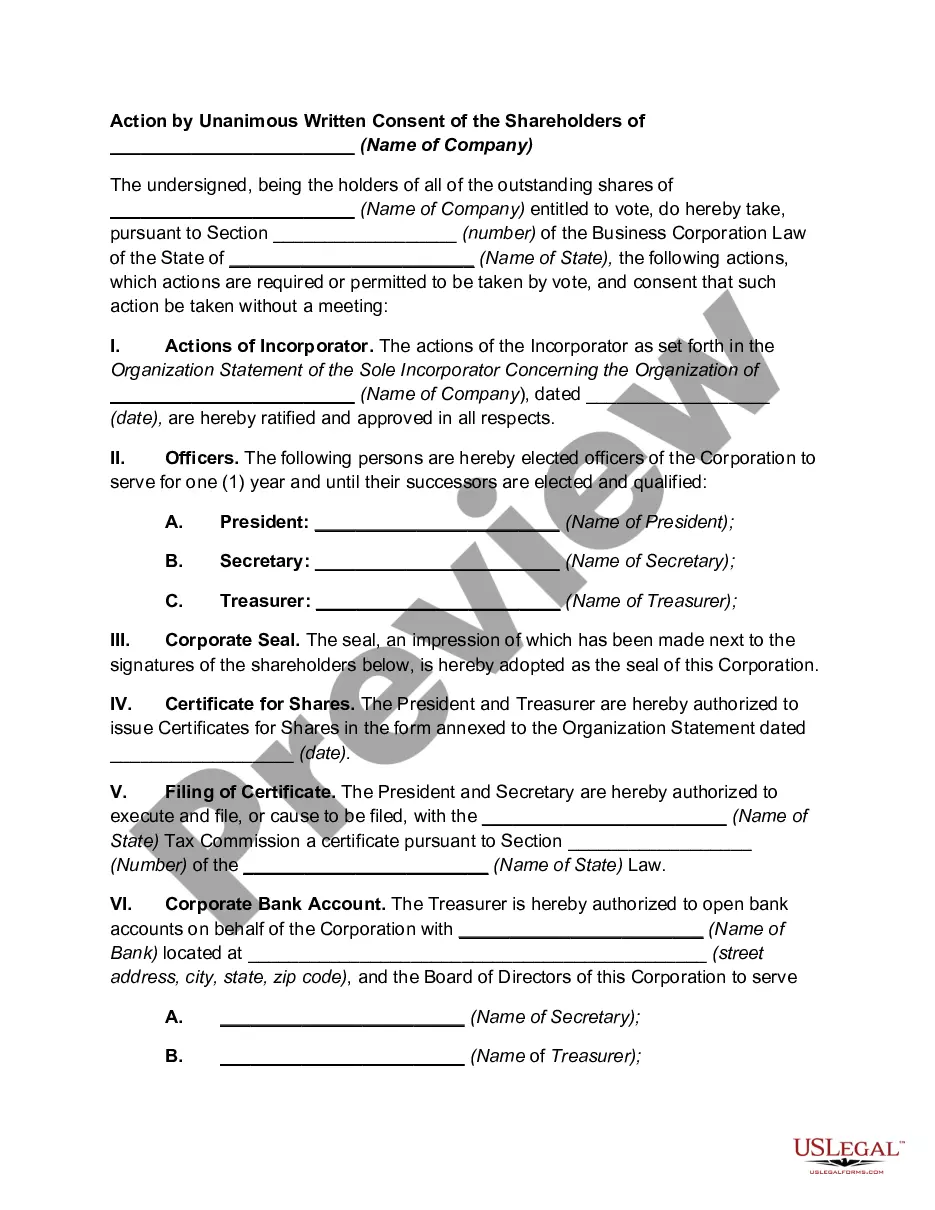

The Purchase of Asset Double Entry in San Diego is a legal document designed to facilitate the sale of business assets from a seller to a buyer. This agreement outlines key elements such as the assets being sold, liabilities that the buyer may assume, and the purchase price allocated to different asset categories. Users are instructed to modify the agreement by deleting non-applicable sections and filling in their specific details, ensuring it aligns with their circumstances. The form is particularly useful for legal professionals like attorneys and paralegals, who can employ it in transaction negotiations and ensure legal compliance. Partners and owners can utilize the agreement to specify asset transfers while protecting their interests. Additionally, legal assistants should be able to assist in drafting and editing the document to meet client needs, thus streamlining the asset purchase process. Filling instructions highlight the need for accuracy to prevent misunderstandings. Potential use cases include acquisitions of equipment, inventory, and goodwill in various business sectors across San Diego.

Free preview