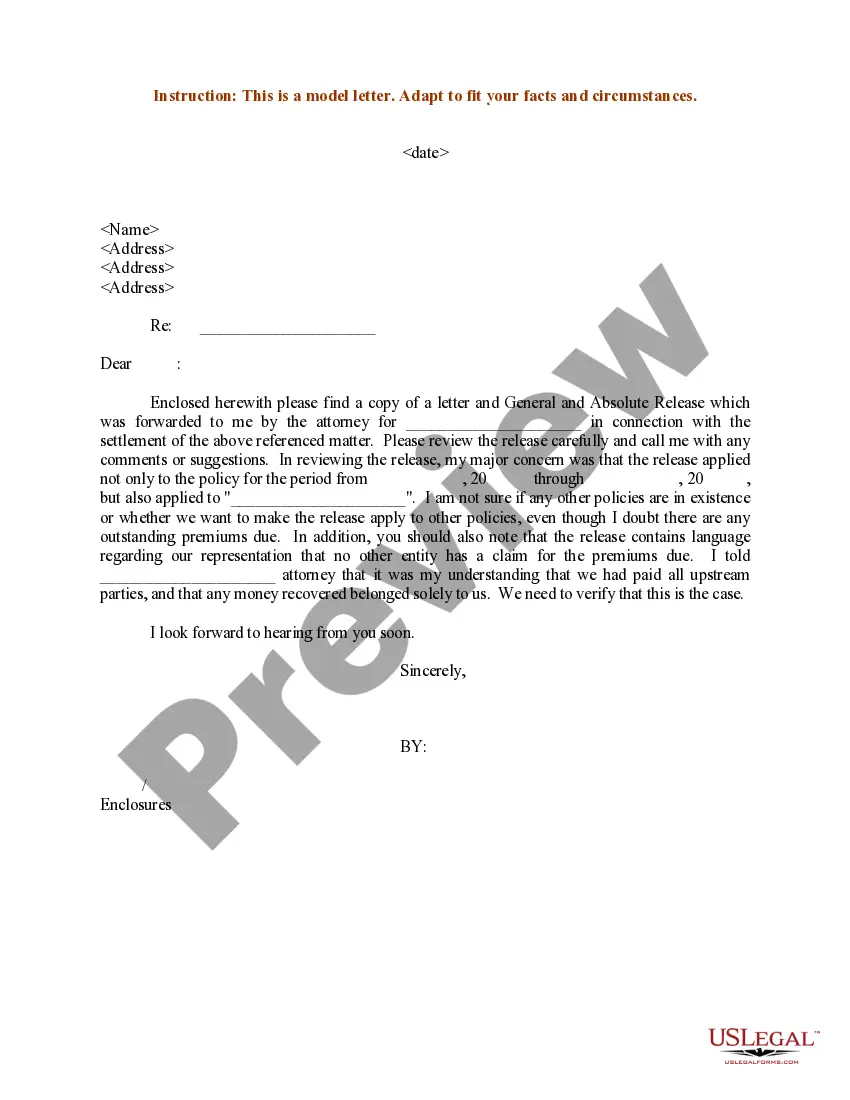

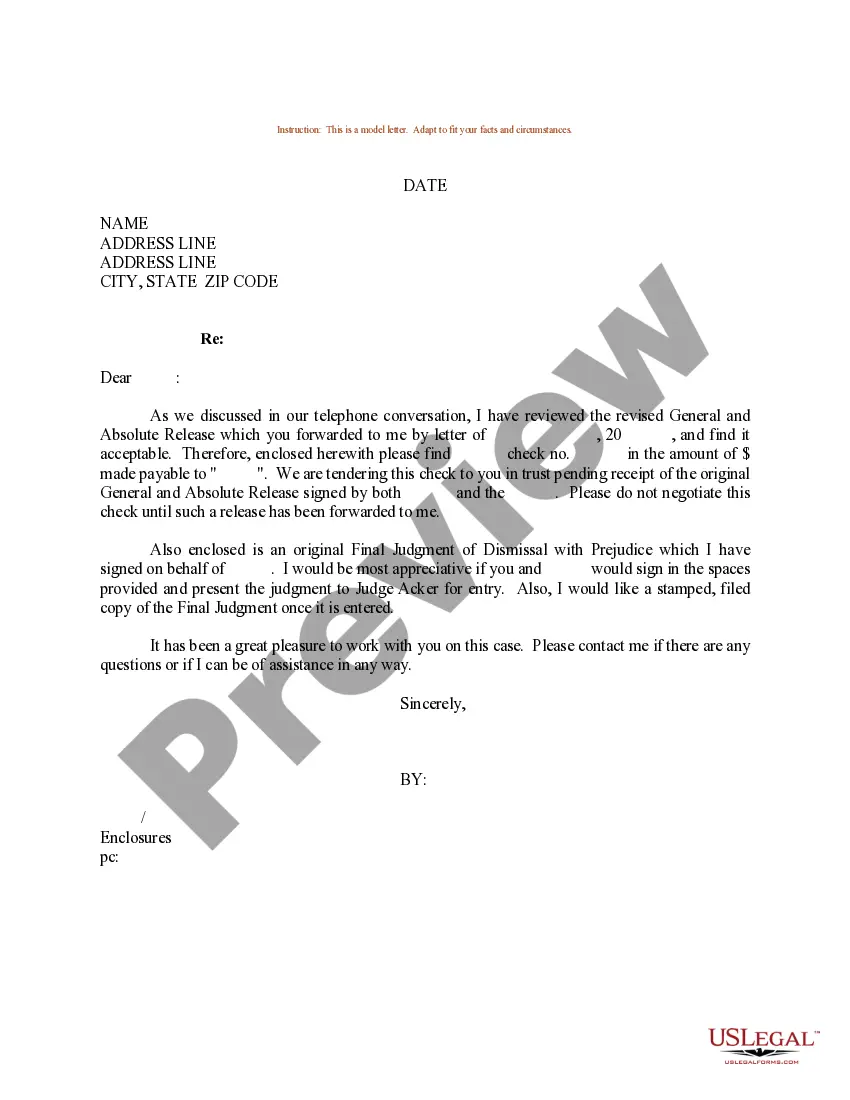

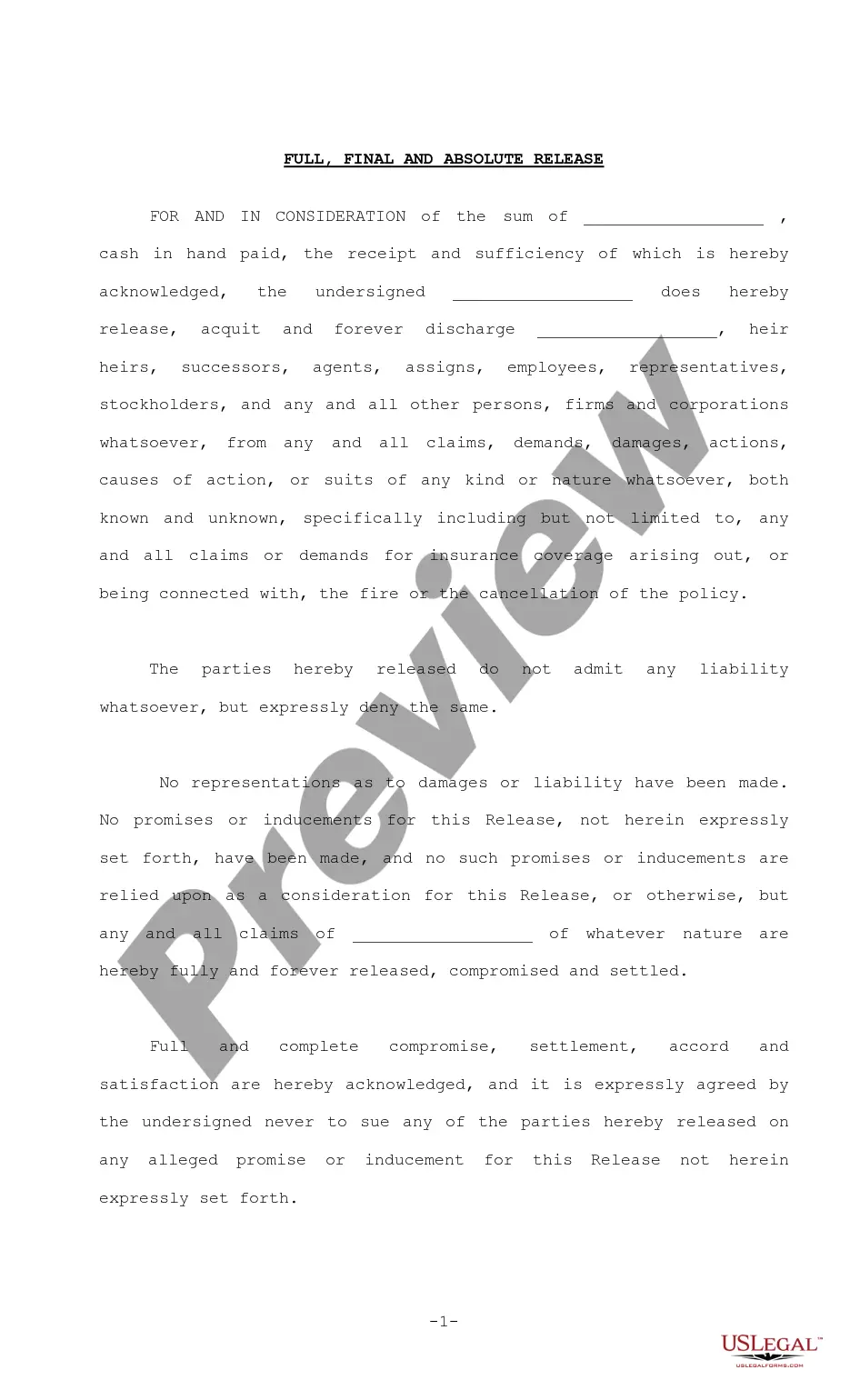

Sample Letter Release Contract For Installment Payment In Nassau

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

If you e-filed, send it to: NYS PERSONAL INCOME TAX PROCESSING CENTER, PO BOX 4124, BINGHAMTON NY 13902-4124. If you filed a paper return, send it to: STATE PROCESSING CENTER, PO BOX 15555, ALBANY NY 12212-5555. If you are using a private delivery service, refer to Publication 55 for designated services.

You must file Form IT-203, Nonresident and Part-Year Resident Income Tax Return, if you: were not a resident of New York State and received income during the tax year from New York State sources, or. moved into or out of New York State during the tax year.

(8/15) Purpose of form. Married nonresidents and part-year residents who are required to file a joint New York State return must use the combined income of both spouses to determine the base tax subject to the income percentage allocation, even if only one spouse has New York source income.

The IT-201 is the main income tax form for New York State residents. It is analogous to the US Form 1040, but it is four pages long, instead of two pages. The first page of IT-201 is mostly a recap of information that flows directly from the federal tax forms.

A tax warrant in New York is a legal claim by the state on personal and real property due to unpaid income, sales, or other New York State taxes. The Department of Taxation and Finance (NYS DTF) issues tax warrants, and they create a lien against assets, allowing the state to seize wages, income, and assets.

If one of you was a New York State resident and the other was a nonresident or part-year resident, you must each file a separate New York return. The resident must use Form IT-201. The nonresident or part-year resident, if required to file a New York State return, must use Form IT-203.