Sample Letter To Close Trust Account With The Same Email In Collin

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Irrevocable trusts generally end after the death of the grantor, when the trustee distributes all of the assets to the beneficiaries. The grantor can also specify an end date or a condition that must be met before the assets can be distributed.

Having the accounts in your trust will help if you become incapacitated. (2/3 of Americans will be incapacitated for some time in their lifetime). Banks are much more hesitant to honor powers of attorney today. I have never had hesitation from a bank to honor a successor trustee during incapacity.

Some of your financial assets need to be owned by your trust and others need to name your trust as the beneficiary. With your day-to-day checking and savings accounts, I always recommend that you own those accounts in the name of your trust.

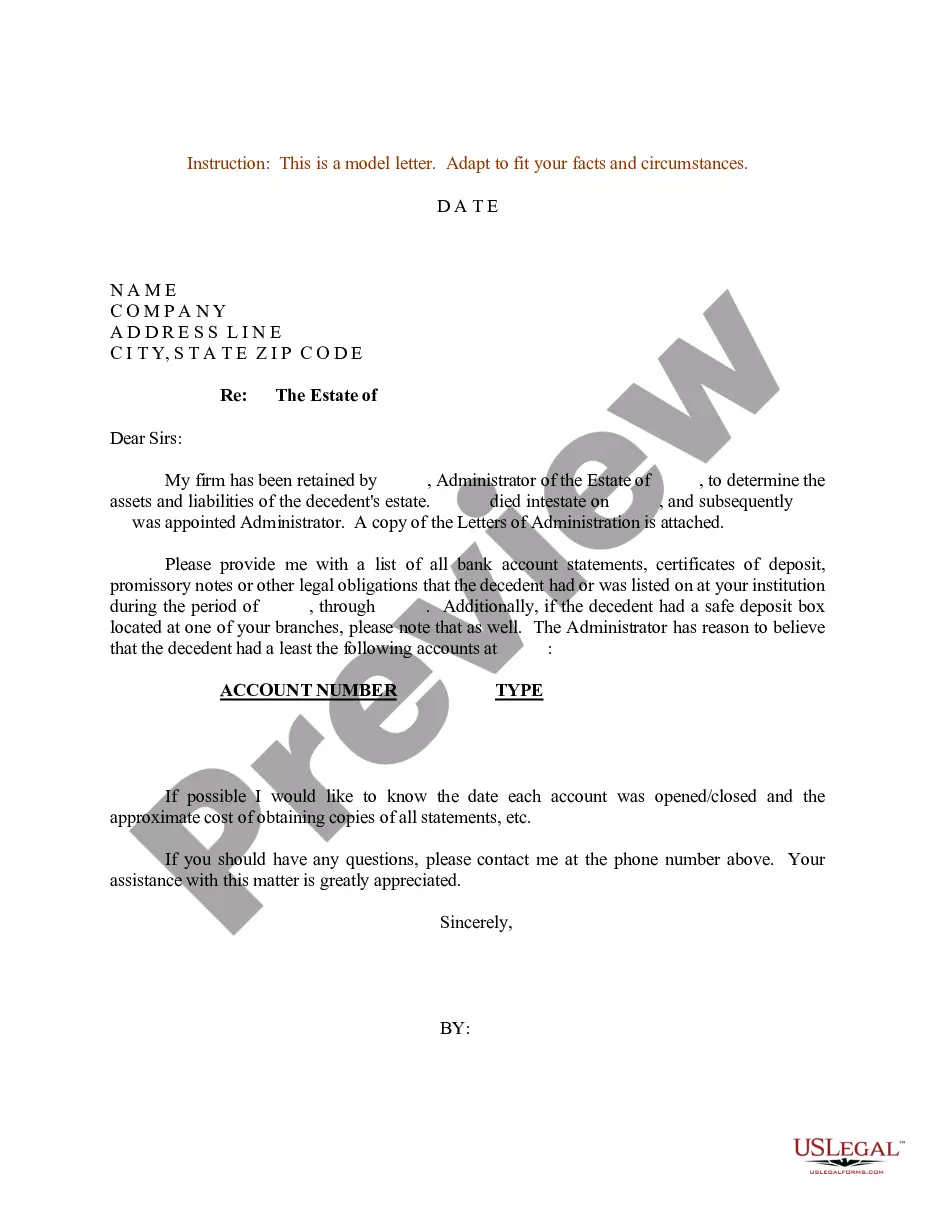

To transfer bank accounts into your living trust: Contact Your Bank: Inform your bank that you want to transfer your accounts into your living trust. They will provide the necessary forms and instructions. Provide Documentation: You must provide a Certification of Trust or a copy of the trust document.

This transfer doesn't usually lead to an immediate tax obligation, meaning no tax is levied for merely changing the ownership. However, the trust, which now owns the stock, may become liable for taxes on dividends and capital gains from the stock.

Only the trustee can close the trust account. Check the bank's requirements for closing accounts to see what documentation you need to bring with you, usually personal identification and any papers you received when you first set up the trust account.

To transfer bank accounts into your living trust: Contact Your Bank: Inform your bank that you want to transfer your accounts into your living trust. They will provide the necessary forms and instructions. Provide Documentation: You must provide a Certification of Trust or a copy of the trust document.