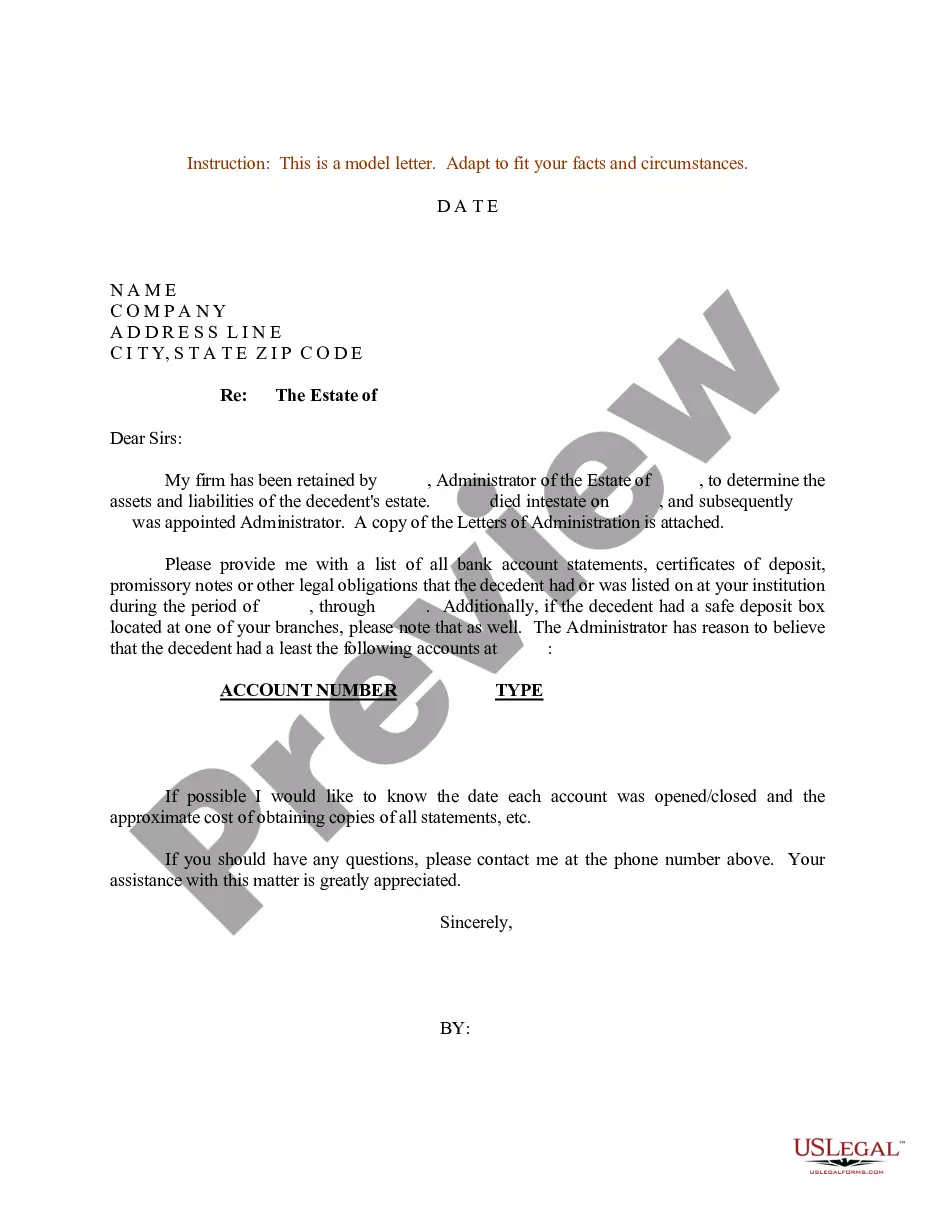

Decedent Account Bank For Union In Bexar

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Contact the bank in advance to ensure you arrive with the appropriate documents, but you'll likely need to bring a notarized or certified copy of the death certificate and proof of your identity, such as a driver's license or passport. You'll also need the decedent's legal name and Social Security number.

How do you get account access after someone dies in Texas? Four Steps: Talk with the bank. Tell the bank that the account holder died, tell the bank who you are, and ask them what documentation they need from you. Give the bank a death certificate. Contact a probate attorney. If it's a joint account or “P.O.D.” account…

Certain types of bank accounts (called payable on death or POD accounts) allow the account holder to designate one or more beneficiaries. This allows the funds to be transferred to the beneficiaries after death without court involvement.

Ans: - Depending on the amount of claim, the following documents need to be submitted. i) Photocopy of Death Certificate (original to be produced for verification by the bank). ii) Photographs and KYC documents of all the claimants/ legal heir(s), (Original documents to be produced for verification by the bank.)

Right of Survivorship It comes from property that is designated or titled as “joint tenant” property with rights of survivorship. This property passes automatically to the surviving named joint account owner on the death of the other owner.

DEATH OF AN ACCOUNT OWNER (12 C.F.R. § 330.3(j)) To ensure that families dealing with the death of a family member have adequate time to review and restructure their accounts if necessary, the FDIC will insure the deceased owner's accounts as if he or she were still alive for six months after his or her death.

For six months after John's death, the deposit insurance coverage is calculated as if John is alive and both deposits remain fully insured. The purpose of the six-month rule is to allow the surviving owner the opportunity to restructure a deposit if necessary to ensure that all funds remain fully insured.

The named beneficiary on an account with a TOD or POD designation will likely need to present a certified death certificate, valid identification, and a completed claim form. Some banks may also require additional documentation to establish the beneficiary's claim on the account.

When you've registered the death, you will be issued with a death certificate. This will act as formal notification for the bank to begin closing the account.

In these cases, simply visit the bank with a valid ID and a certified copy of the death certificate. You will then have access to the account, allowing you to withdraw the funds as needed.