Letters Legal Collections Without Prejudice In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

It depends. If prosecutors dismissed the case “without prejudice,” they can refile charges any time before the statute of limitations has expired – that is, they can reopen it if they are able to overcome whatever caused the dismissal in the first place.

The dismissal ``without prejudice'' does not mean that you won the issue regarding the debt. It just means that the creditor stopped fighting in court without conceding that you won. So the dismissal ``without prejudice'' does not necessarily help your argument to remove this from your credit report.

If the case is dismissed without prejudice, prosecutors will have another two years to refile before the statute of limitations expires. You can contact our California criminal defense lawyers for a case review. Eisner Gorin LLP has offices in Los Angeles, California.

Ignoring or avoiding the debt collector may cause the debt collector to use other methods to try to collect the debt, including a lawsuit against you. If you are unable to come to an agreement with a debt collector, you may want to contact an attorney who can provide you with legal advice about your situation.

The dismissal ``without prejudice'' does not mean that you won the issue regarding the debt. It just means that the creditor stopped fighting in court without conceding that you won. So the dismissal ``without prejudice'' does not necessarily help your argument to remove this from your credit report.

A judge may dismiss a case without prejudice in order to allow for errors in the case presented to be addressed before it is brought back to court. A judge will dismiss a case with prejudice if he or she finds reason why the case should not move forward and should be permanently closed.

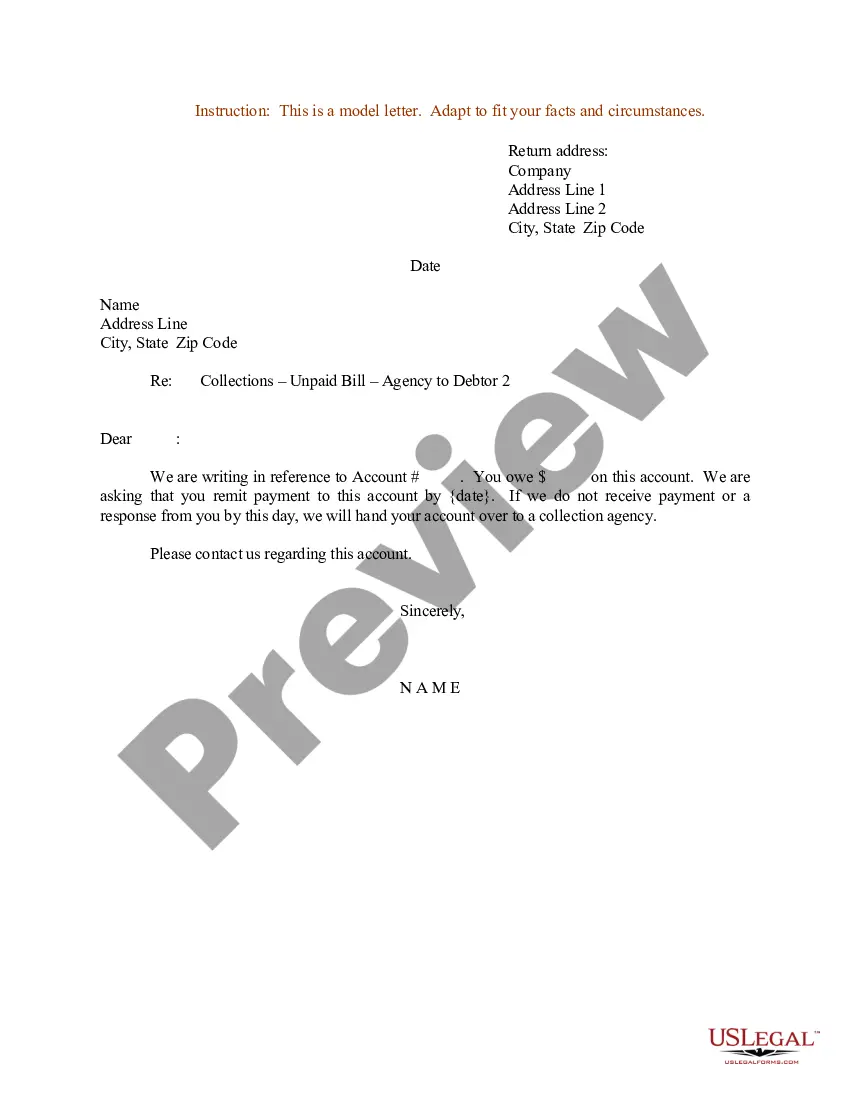

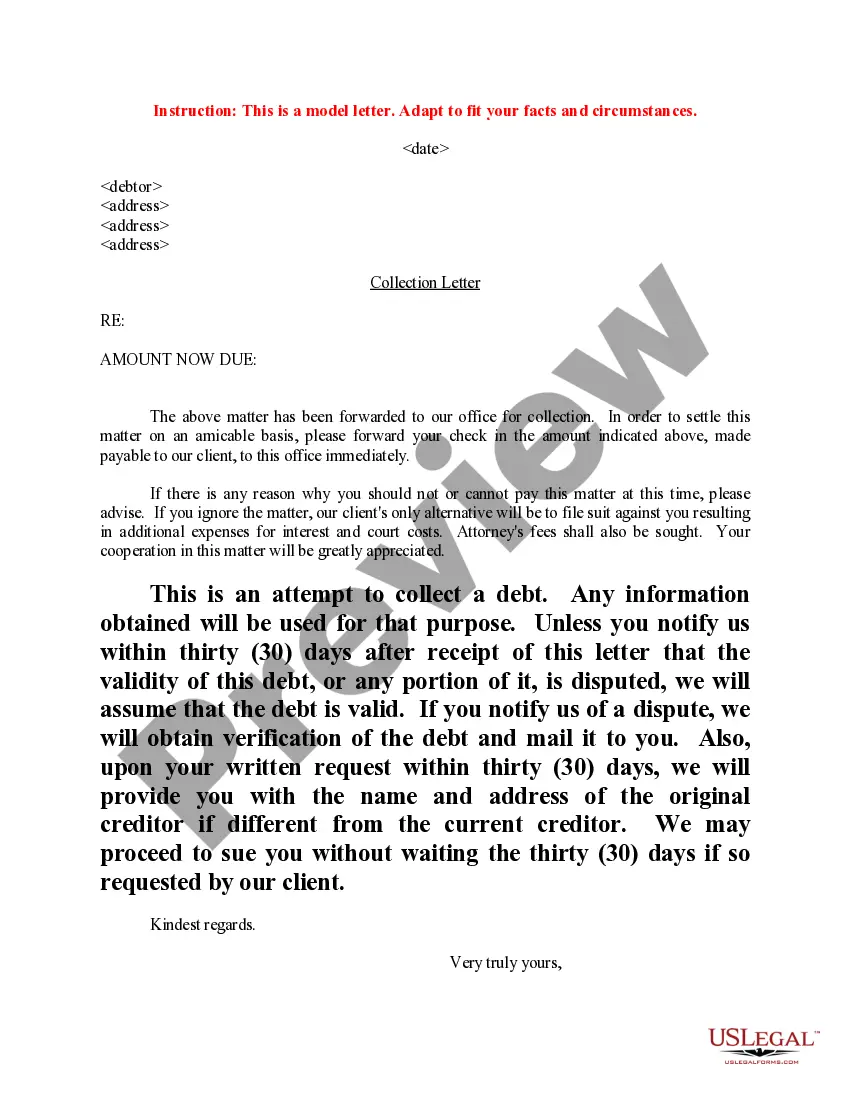

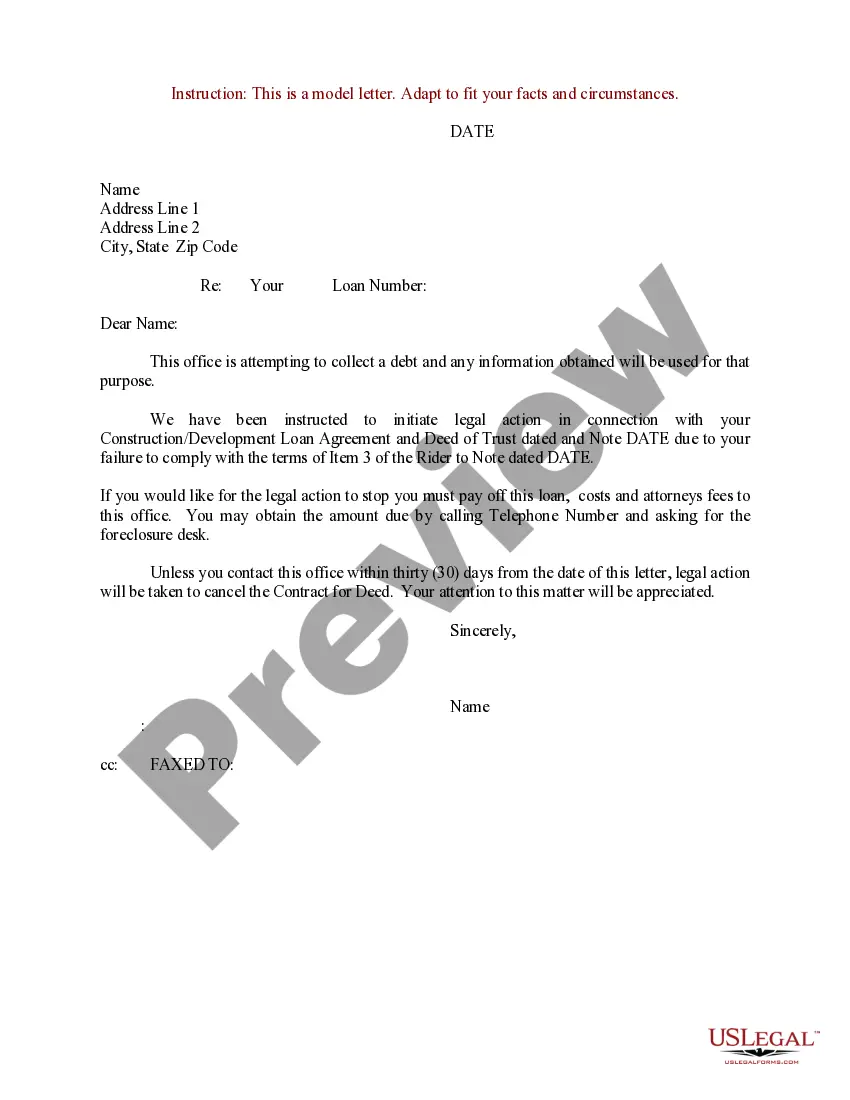

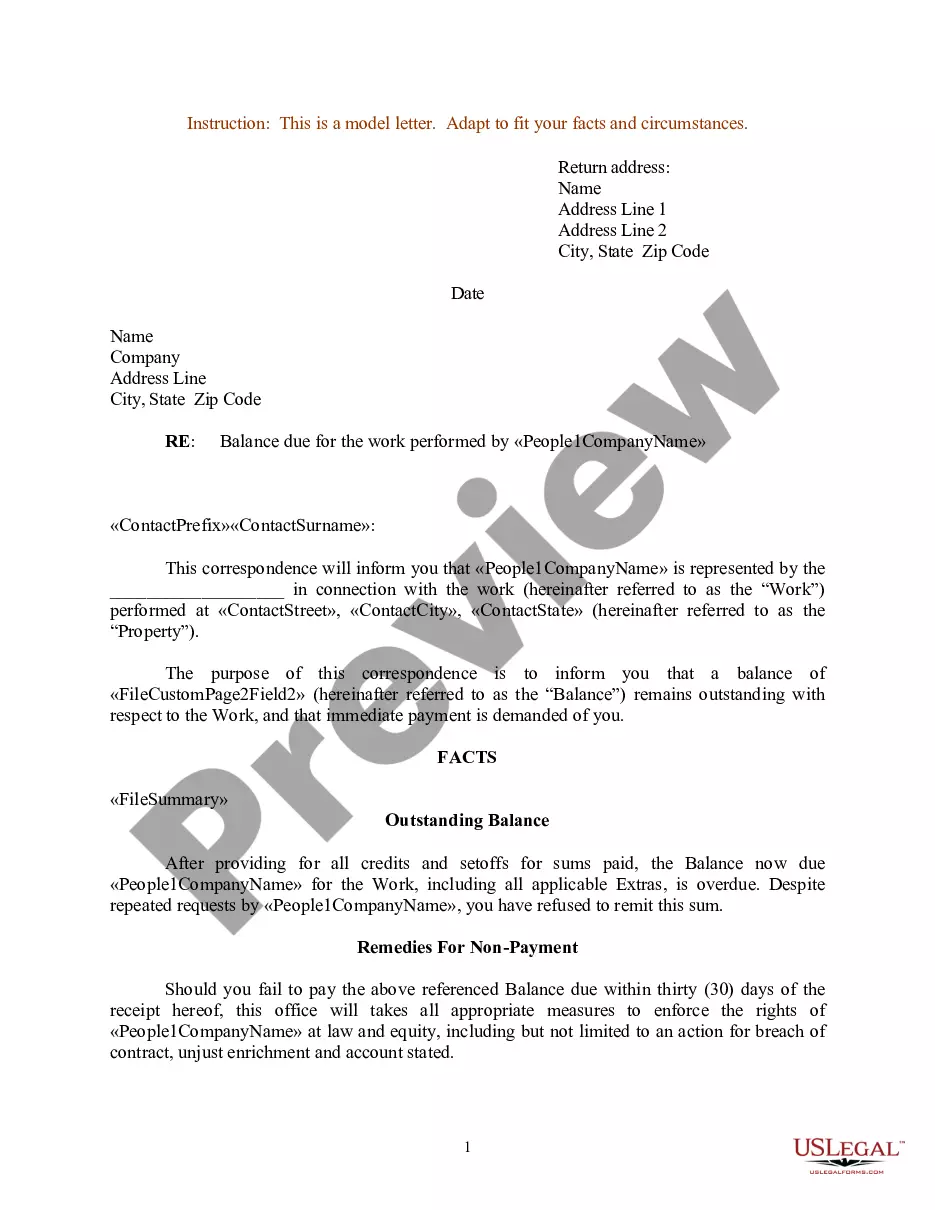

These letters often include details like the amount owed, the due date, and any applicable interest or late fees. It's important to note that debt collection letters should adhere to legal regulations and guidelines, such as those outlined by the Fair Debt Collection Practices Act (FDCPA) in the United States.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

Within five days after a debt collector first contacts you, it must send you a written notice, called a "validation notice," that tells you (1) the amount it thinks you owe, (2) the name of the creditor, and (3) how to dispute the debt in writing.

4) 623 credit dispute letter A business uses a 623 credit dispute letter when all other attempts to remove dispute information have failed.