Legal Letter For Collections In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

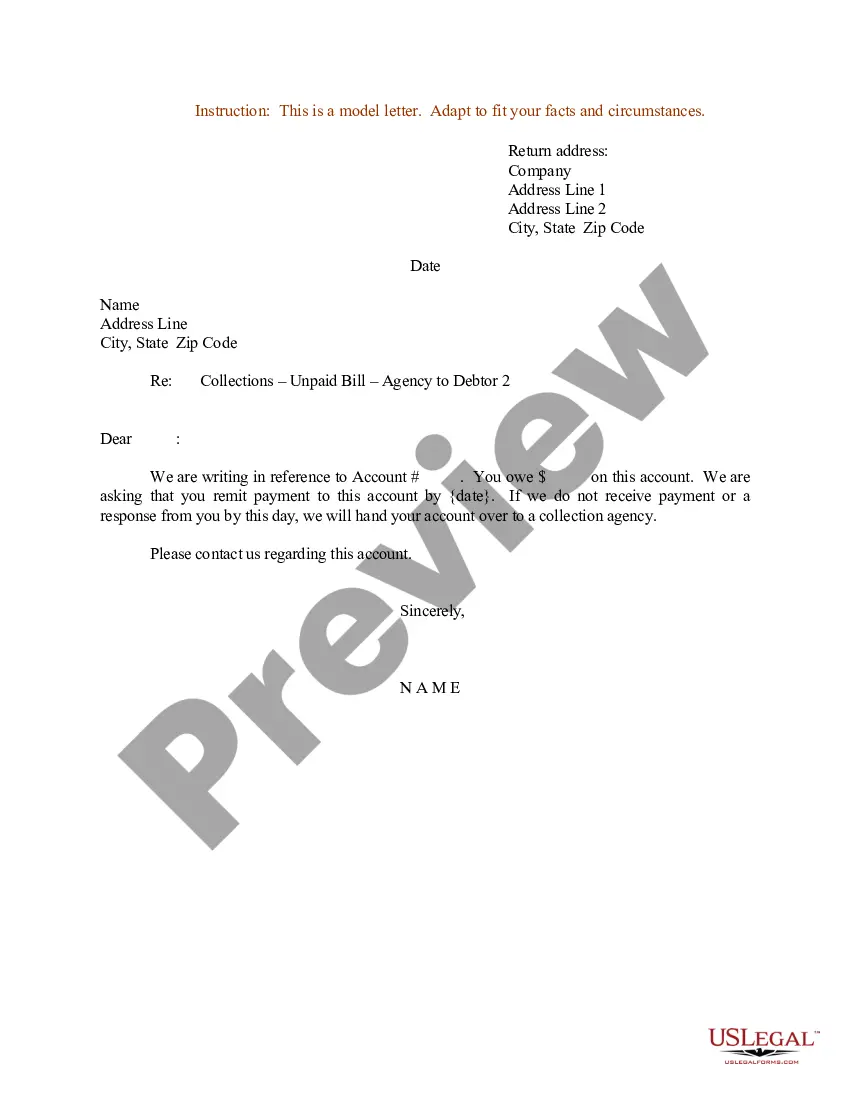

Whenever someone tries to collect a debt, ask for all of their company's information, including: The collector's full name. Company name. Company address. Company phone number. Company website address. Company email.

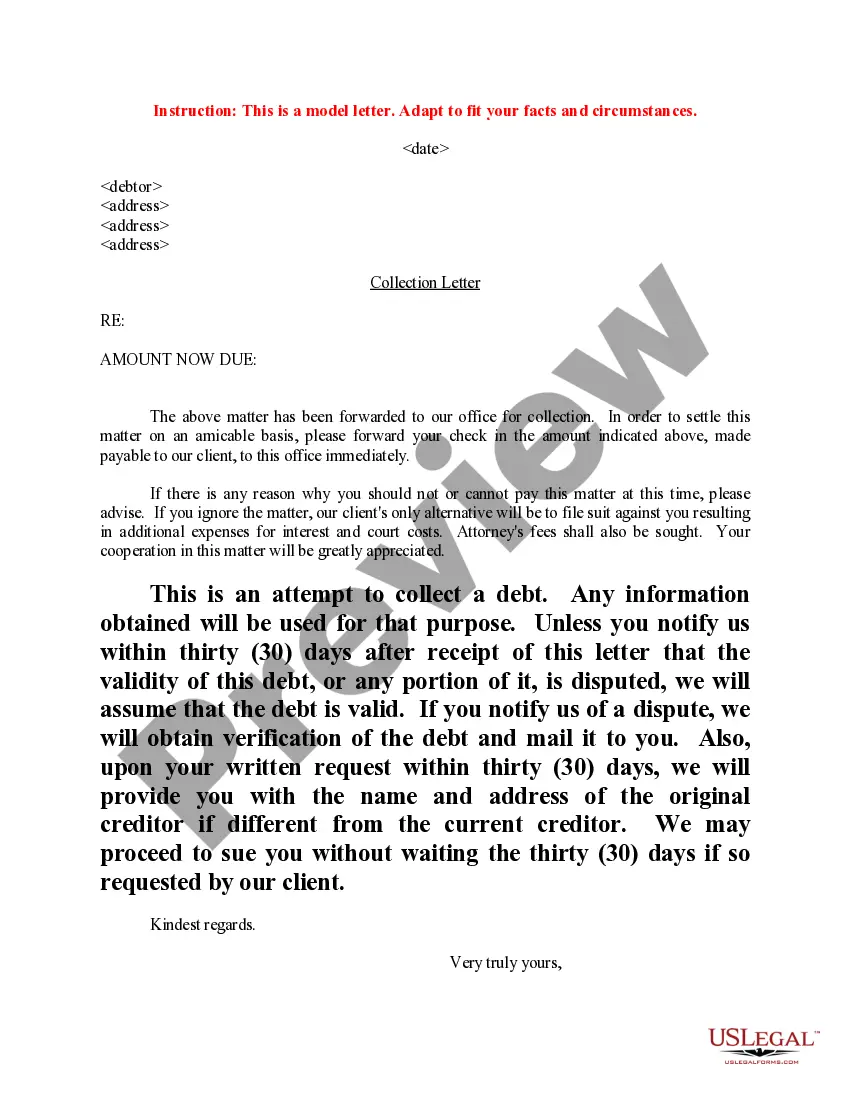

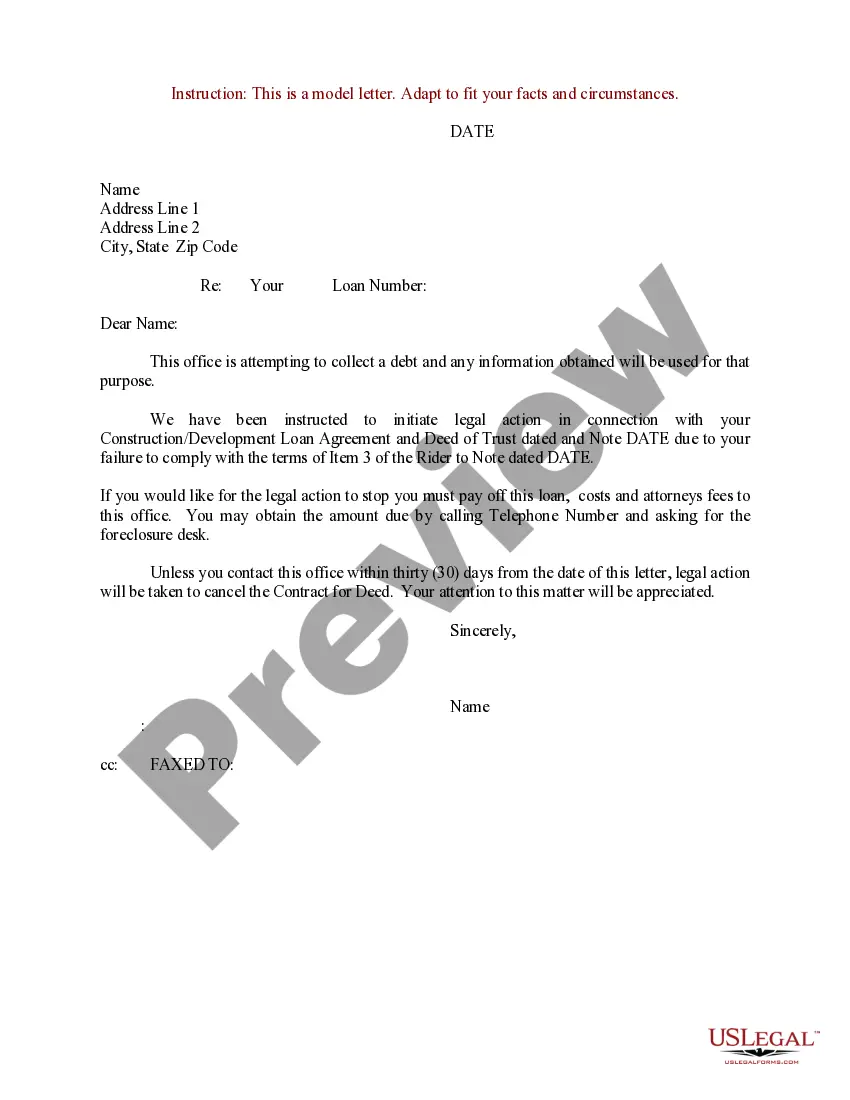

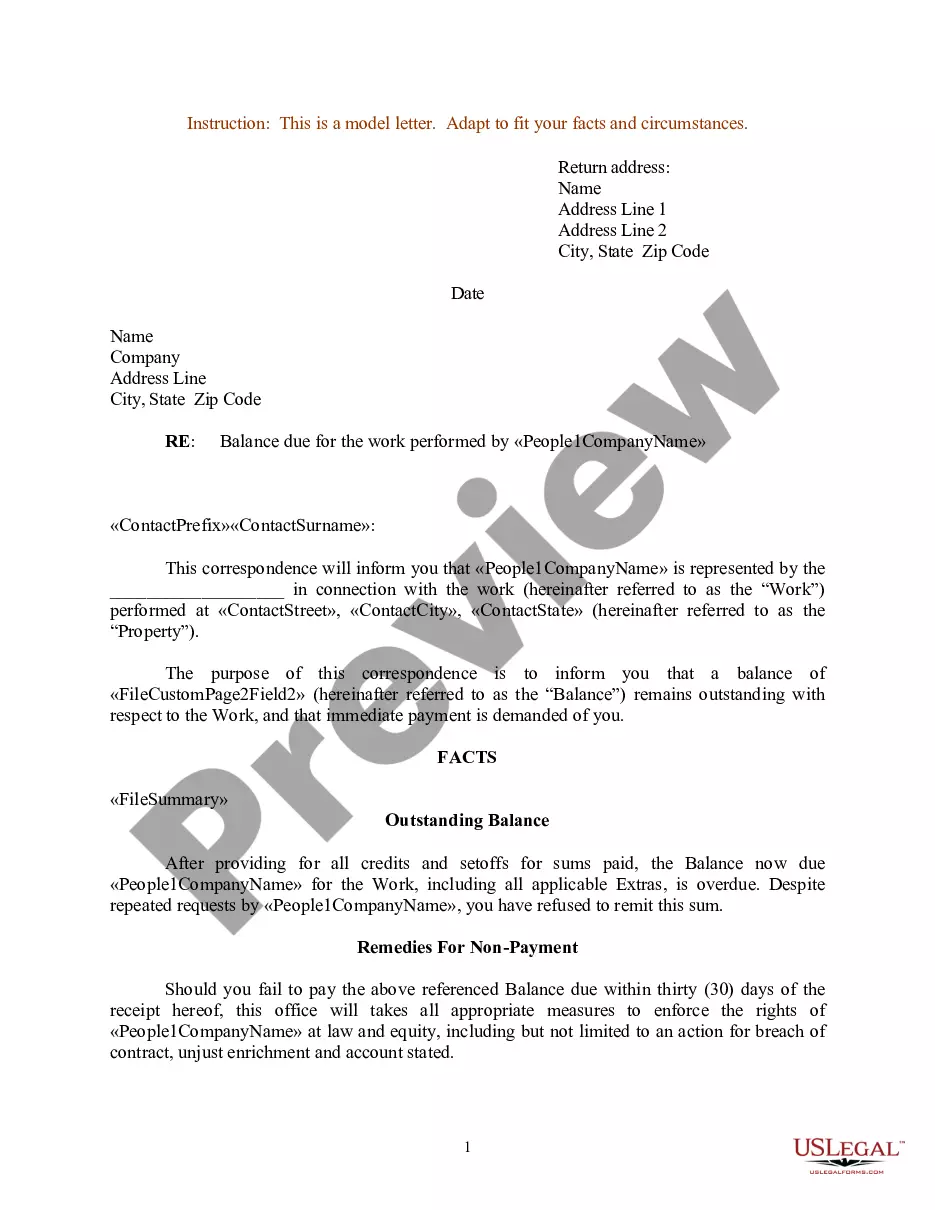

These letters often include details like the amount owed, the due date, and any applicable interest or late fees. It's important to note that debt collection letters should adhere to legal regulations and guidelines, such as those outlined by the Fair Debt Collection Practices Act (FDCPA) in the United States.

A copy of the original credit card agreement with your signature. Account statements showing the debt amount, including charges, payments and interest. Documentation showing the collector's right to pursue the debt. Records demonstrating the chain of ownership if the debt has been sold.

The 11-word phrase often cited to stop debt collectors is: ``I do not acknowledge this debt and request verification of it.'' This phrase requests that the debt collector provide verification of the debt, which they are legally obligated to do under the Fair Debt Collection Practices Act (FDCPA) in the United States.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

What things should be included in the Full and Final Settlement Letter? Settlement Amount: Clearly state the finalized amount to be settled. Settlement Cheque: Provide details regarding the issuance of the settlement cheque. Resignation/Termination Date: Specify the date on which the employee resigned or was terminated.

If you write a letter, instead of using the tear-off form, the debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request the debt not be reported to credit reporting agencies until the matter is resolved or ...

It depends on what you can afford. Your full and final settlement should offer equal amounts to each creditor. For example: Your lump sum is 75% of your total debt. You should offer each creditor 75% of what you owe them.