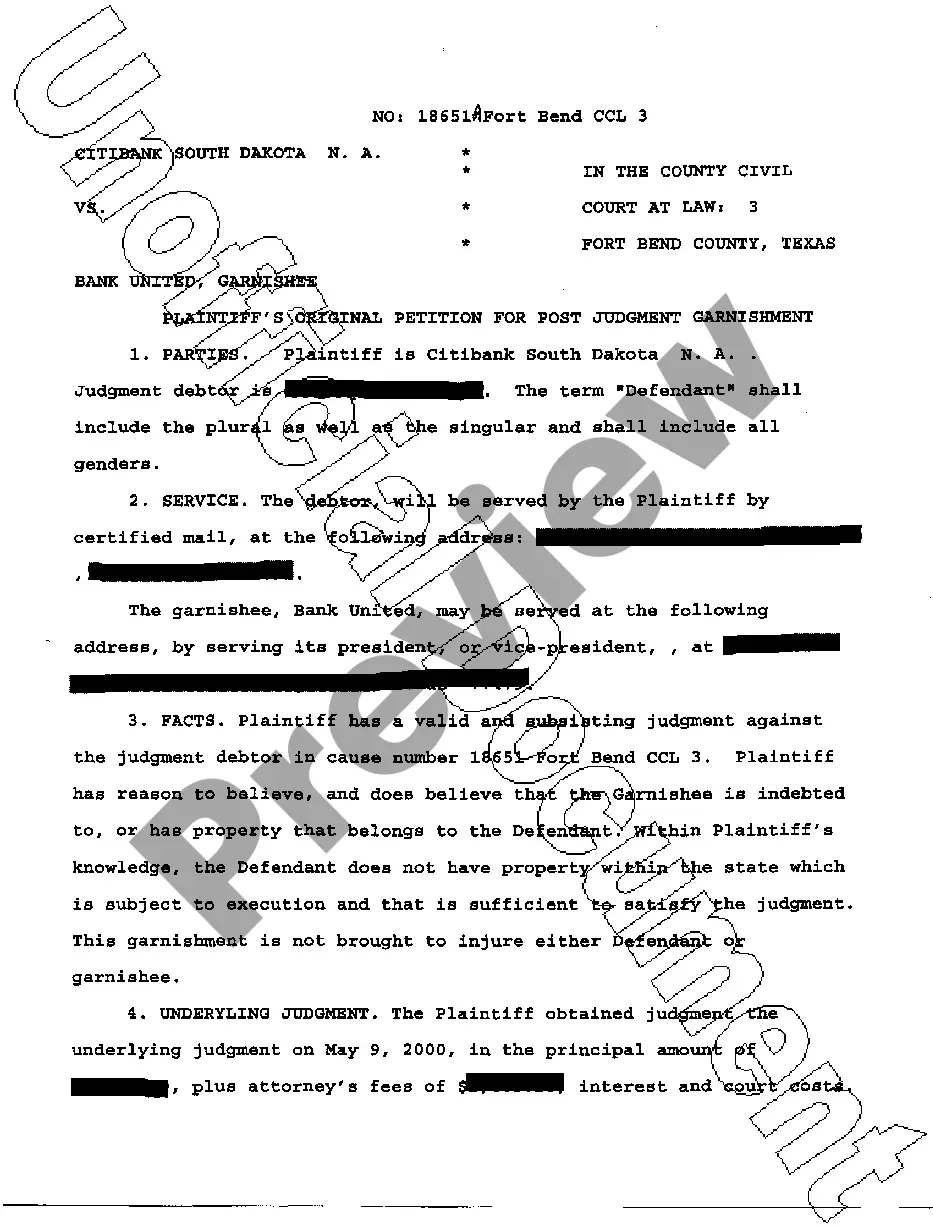

Erisa Retirement Plan In New York

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

In general, ERISA does not cover plans established or maintained by governmental entities, churches for their employees, or plans which are maintained solely to comply with applicable workers compensation, unemployment or disability laws.

ERISA may preempt the CCPA if a court were to find that the CCPA impermissibly interferes with the administration of ERISA plan benefits.

The Employee Retirement Income Security Act of 1974 (ERISA) is a federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry to provide protection for individuals in these plans.

Check Your Plan Documents: Review your Summary Plan Description (SPD) or other documents. ERISA plans must provide an SPD that clearly states they are an ERISA plan. Look at Employer Contributions: If your employer contributes to the plan or matches your contributions, it's likely an ERISA plan.

How does ERISA's original preemption clause affect state health policy? Several of ERISA's provisions preempt state law. ERISA's “preemption clause,” Section 514, makes void all state laws to the extent that they “relate to” employer-sponsored health plans.

In a nutshell, the New York State Secure Choice Savings Program is a state-mandated retirement savings plan for New York employees. Employee contributions are made using automatic payroll deductions, with all funds placed in a Roth individual retirement account, or Roth IRA.

ERISA's “preemption clause” makes void all state laws to the extent that they “relate to” employer-sponsored health plans. Who interprets and enforces ERISA? The U.S. Department of Labor is responsible for administering and enforcing the ERISA law and setting policy for the conduct of employee benefit plans.

Qualified plans include 401(k) plans, 403(b) plans, profit-sharing plans, and Keogh (HR-10) plans. Nonqualified plans include deferred-compensation plans, executive bonus plans, and split-dollar life insurance plans.

The Form 5500 Series is part of Employee Retirement Income Security Act's (ERISA) reporting and disclosure framework intended to ensure that employee benefits plans are operated and managed in ance with prescribed standards.

Basic ERISA compliance requires employers provide notice to participants about plan information, their rights under the plan, and how the plan is funded. This includes ensuring plans comply with ERISA's minimum standards, recordkeeping, annual filing and reporting, and fiduciary compliance.