Payoff Letter For Promissory Note In Fairfax

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

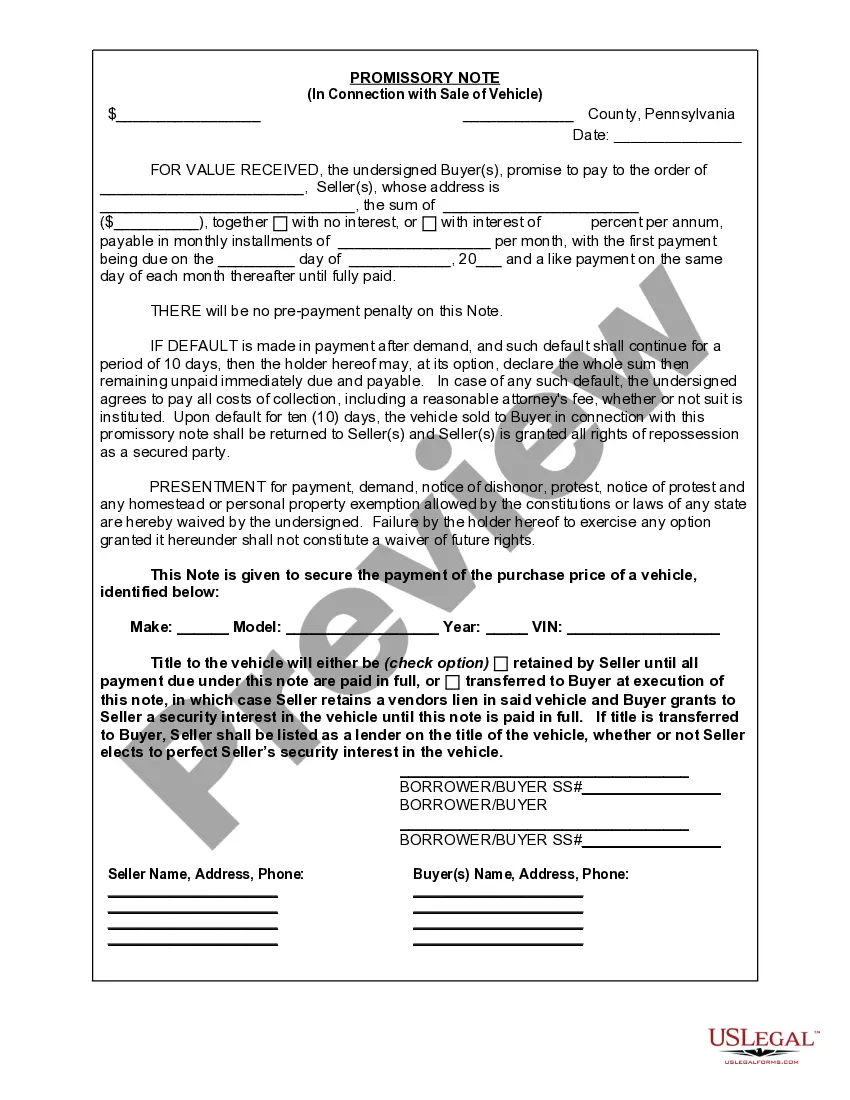

Yes, a properly executed promissory note is legally binding. As long as the note contains all necessary elements, is signed by the involved parties, and complies with applicable laws, it's enforceable in court if the borrower defaults or fails to meet their obligations.

What invalidates promissory notes? Incomplete signatures. Both parties must sign the promissory note. Missing payment amount or schedule. Missing interest rate. Lost original copy. Unclear clauses. Unreasonable terms. Past the statute of limitations. Changes made without a new agreement.

But what exactly do you need to write a promissory note? Include their full legal names, addresses, and contact numbers—include any co-signers if applicable. The terms of this note should specify the amount borrowed, repayment terms (including interest rate, if applicable), and the due date or schedule of payments.

A simple promissory note might be for a lump sum repayment on a certain date. For example, let's say you lend your friend $1,000 and he agrees to repay you by December 1st. The full amount is due on that date, and there is no payment schedule involved.

Cons of a promissory note Limited legal recourse: While a promissory note is a legal document, enforcing repayment can be challenging if the borrower defaults. Interest costs: If the promissory note includes interest terms, the borrower will incur additional costs.

The note must clearly mention only the promise of making the repayment and no other conditions. After issuance, a Promissory Note must be stamped ing to the regulations of the Indian Stamp Act.

Under the Code, the maker of a note can be discharged only by payment, cancellation,7 real defenses,8 or the running of the statute of limitations.

All parties to the original debt instrument normally execute a Payoff Letter before it becomes binding. The final version of the document often reflects specifics of the parties' negotiations. Payoff Letters provide detailed terms and procedures regarding the payoff process.

A payoff statement can be a binding agreement if the terms of the payoff are followed. If the lender later claims the payoff was not correct, our claims counsel can rely on the payoff statement to defend the company in a claim. If the payoff is not directly to your firm or title company then claims loses that defense.