Annual Meeting Shareholders With Employee In Washington

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

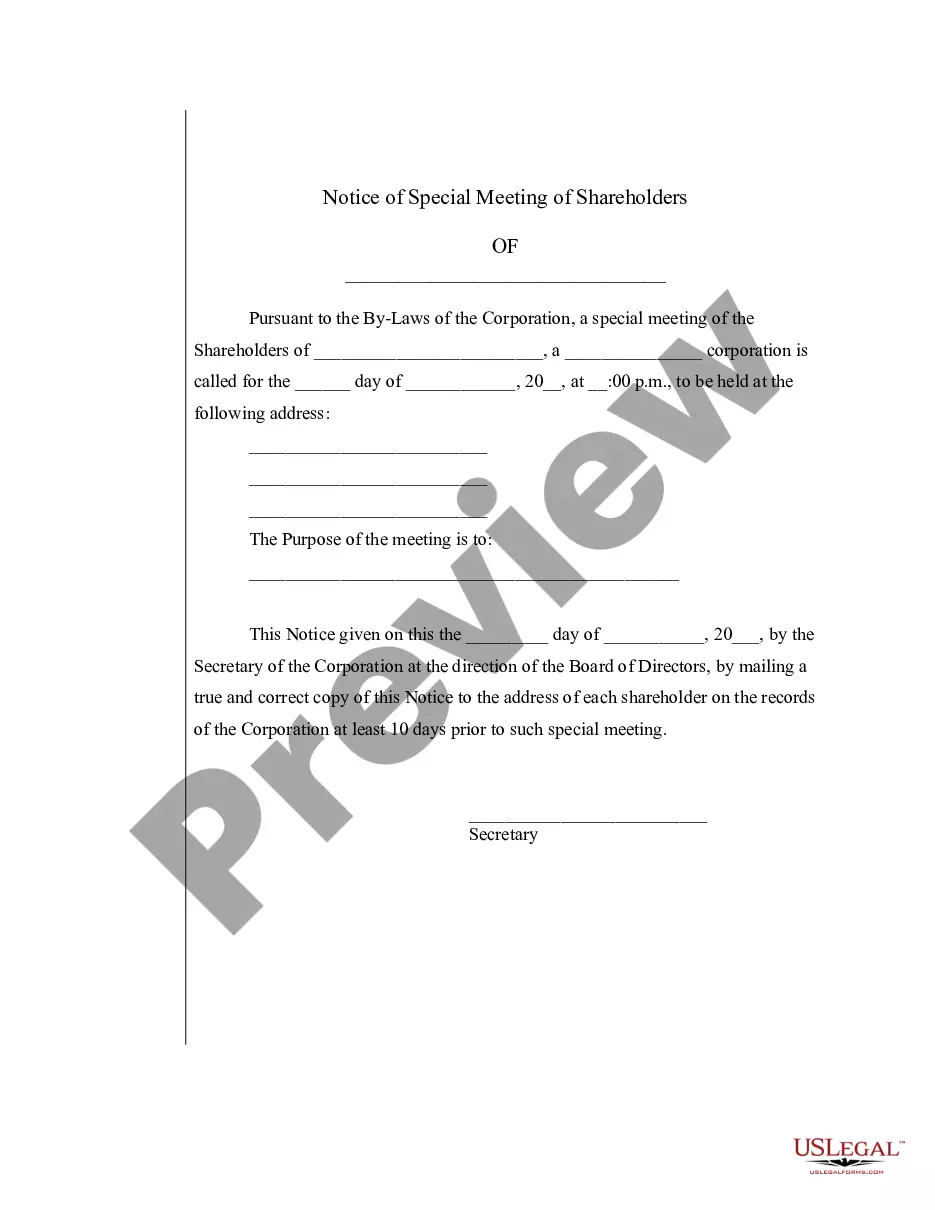

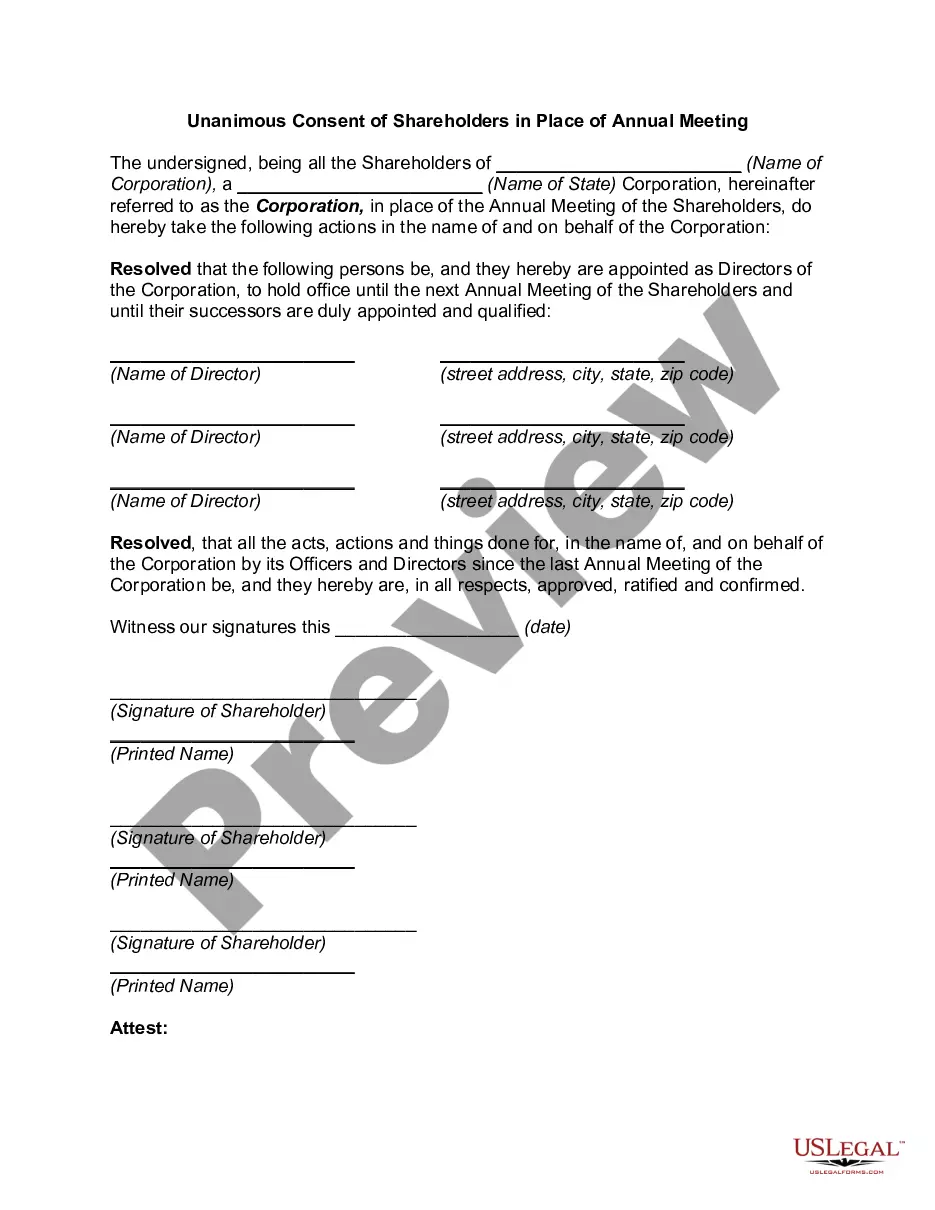

If your business is set up and registered as a Corporation, you're required by law to hold an annual shareholder meeting and to document the meeting with minutes.

Section 601 - Notice of shareholders' meeting or report (a) Whenever shareholders are required or permitted to take any action at a meeting a written notice of the meeting shall be given not less than 10 (or, if sent by third-class mail, 30) nor more than 60 days before the date of the meeting to each shareholder ...

Not complying with regulations regarding annual shareholder meetings can put your company, and its owners, at personal risk for liability.

A company other than OPC must conduct at least one Annual General Meeting (AGM) in a financial year. The first AGM of the company, i.e. a newly incorporated company, should be held within nine months from the closing of the first financial year.

A General Meeting is simply a meeting of shareholders and 21 days' notice must be given to shareholders, but this can be reduced to 14 days, or increased to 28 days, in certain situations.

When should I hold a shareholder meeting? An annual shareholder meeting is typically scheduled just after the end of the fiscal year. This allows for the previous year's financial performance to be fully assessed and discussed.

Scheduled meetings – Your business should hold at least one annual shareholders' meeting. You can have more than one per year, but one per year is often the required minimum. An annual board of directors meeting is often also held in conjunction with the shareholders' meeting as well.

All shareholders are legally obligated to receive an invitation to these meetings. The board of directors should also be represented. An auditor may also be present if the organization is subject to an audit requirement.

There will be specific questions relating to the financials, borrowing, future investment needs, impact of interest rate increases, operations and business of your company and the current market for your particular sector so make sure these are included in your Q&A document.