Debt Settlement Letter Sample With Bank In Pima

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

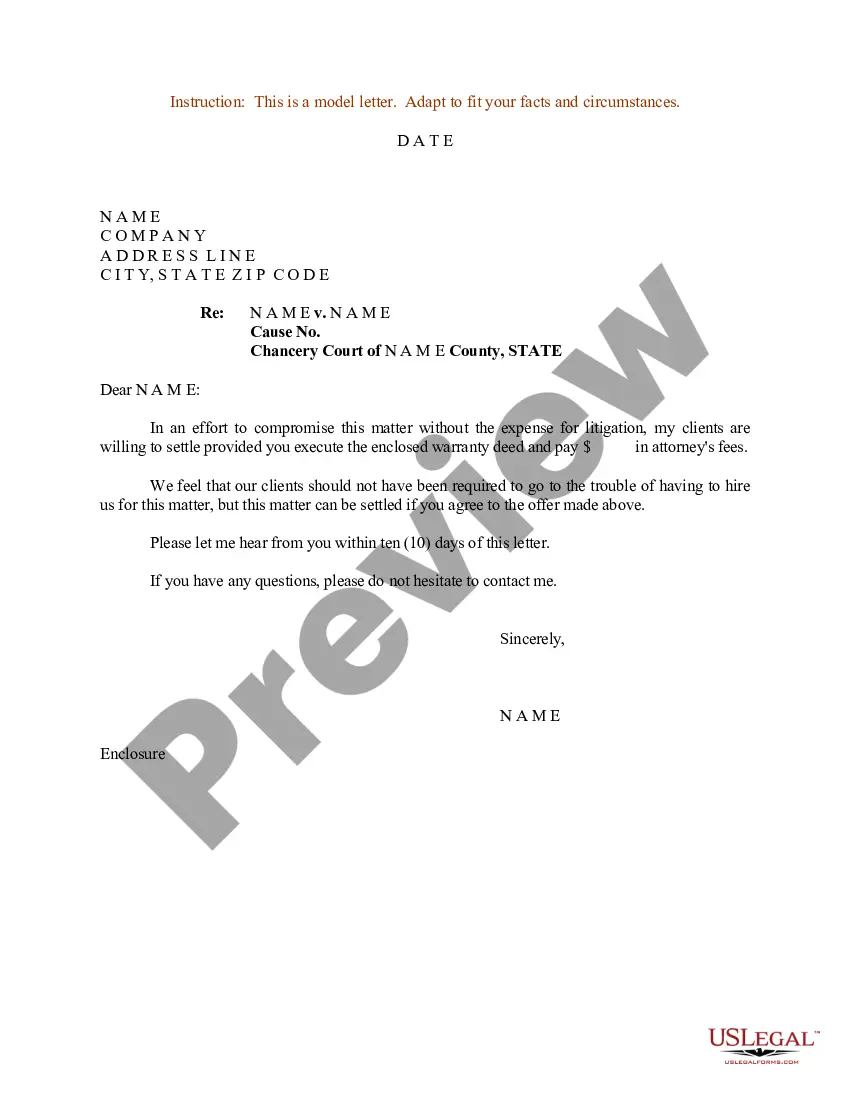

Settlement Letter - Confirms the amount to settle debt up to a specified date. Letter of Indebtedness - Confirms the amount owed to date as of the letter's date. Letter of Non-Indebtedness - Confirms no outstanding debt.

Average account settlement amount after company fees: 32% Each creditor is unique when it comes to their willingness to negotiate with the debt settlement company you've hired. In general, the average settlement offer is for about half of what you first owed.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

A good settlement offer is one that fully compensates you for all of the damages you've suffered due to an accident or injury caused by the wrongdoing of another. It should cover not only current medical expenses but also future costs, lost income, and other losses.

Explain your circumstances and propose a settlement amount. The lender might counteroffer, and the goal is to reach a mutually agreeable amount. 4. Get It in Writing: Once a settlement amount is agreed upon, ensure you receive a written agreement from the lender.

In some instances of serious financial hardship, your lender or credit card provider may be willing to settle your outstanding balance for less than what you owe — provided you can offer them a large lump-sum payment.

In some instances of serious financial hardship, your lender or credit card provider may be willing to settle your outstanding balance for less than what you owe — provided you can offer them a large lump-sum payment.

Talk to your bank to find out what your options are if you have debts with them. They may be able to: Separate any overdrafts from your existing account. Set up a new 'clean' basic bank account for you.

No, there's no way you can get the bank to forgive the debt.

Several factors influence the success of your debt settlement negotiations: Debt Amount. Larger debts often have more negotiation potential. Payment History. Credit Score. Economic Conditions. Bank's Policy. Contact Your Bank. Gather Financial Information. Be Prepared to Negotiate.