Debt Settlement Letter Sample With Payment In Montgomery

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Clearly define objectives before drafting the settlement offer. If monetary compensation is involved, the offer should specify the amount, payment schedule, and contingencies for non-payment. Non-monetary terms, such as confidentiality clauses, mutual releases, or other protective measures, should also be considered.

Settling out of court Make sure the process is perceived to be fair. Identify interests and tradeoffs. Insist on decision analysis. Reduce discovery costs.

Open with an introduction: Address the recipient respectfully and state the purpose of the letter—requesting a payment plan agreement. Provide context: Briefly explain the circumstances, such as financial constraints or unforeseen challenges, that necessitate the request.

These are the steps to follow: Work out what you can offer the people you owe. Send your offer to them in writing. Ask them to confirm they accept your offer in writing. Keep any letters your creditors send you about the settlement offer. Negotiate with your creditors if you need to.

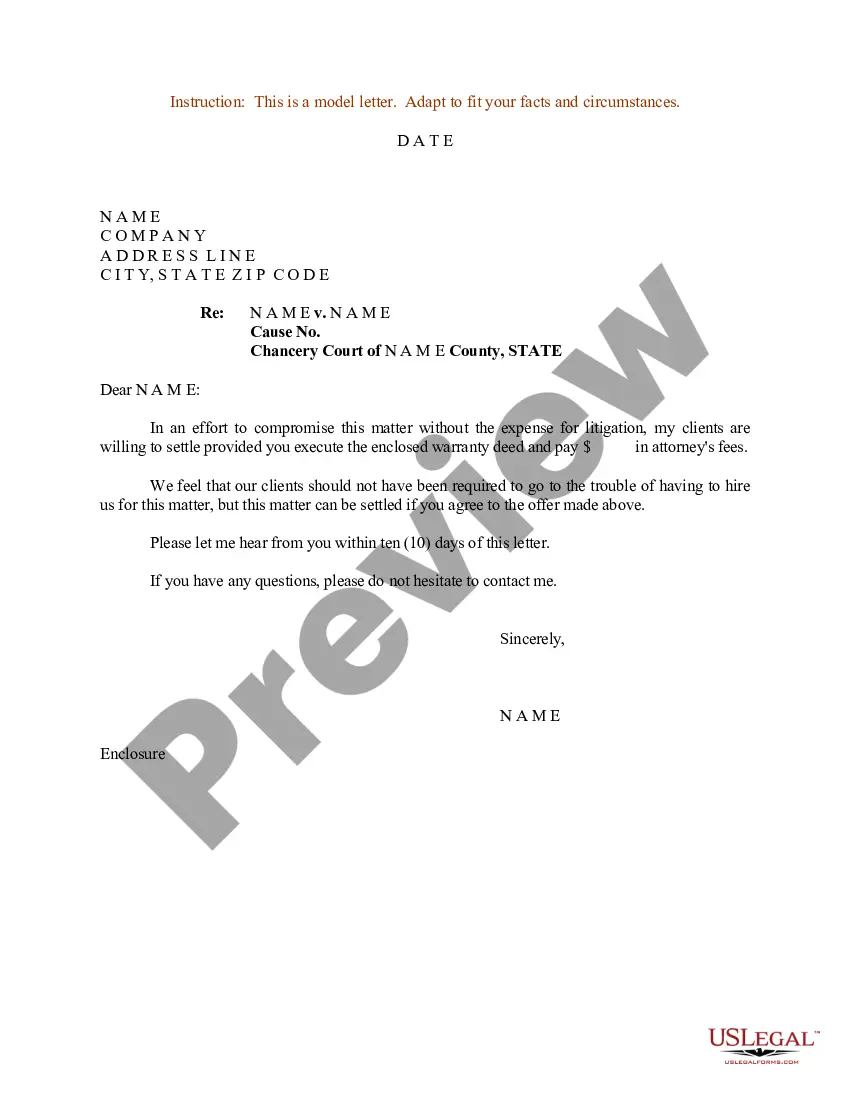

Most debt settlement letters include: The date, name, and address of the credit card company. A notation after the address that this is regarding a hardship letter. The credit card number and amount of the debt. A short statement of your financial situation, why you're in that situation, and why full payment is a hardship.

A comprehensive debt settlement agreement template should cover the following elements: Parties involved. Identify clearly the debtor and creditor, including their legal names and contact information. Debt details. Settlement amount. Payment terms. Release of claims. Confidentiality. Governing law. Signatures.

Sure. You can repay a debt in several installments. I have seen many debt collectors work with these sorts of arrangements.

You can try to negotiate a debt settlement on your own, but it's typically done through third parties like debt relief companies, which you hire to negotiate on your behalf. With this method, you will make payments to the debt settlement company rather than your creditors, along with any fees.

Unfortunately, my circumstances are unlikely to improve in the foreseeable future and I have no assets to sell to help clear my debt. I am therefore asking you to consider writing off my debt as I can see no way of ever repaying it. If you are unable to agree to this, please explain your reasons.

The debt settlement company calls the borrower's creditor and negotiates a lump-sum debt payment of $20,000 to satisfy the previously required monthly debt payments of $10,000. The creditor, having written off the borrower due to non-payments for three months, accepts the lump-sum payment of $20,000.