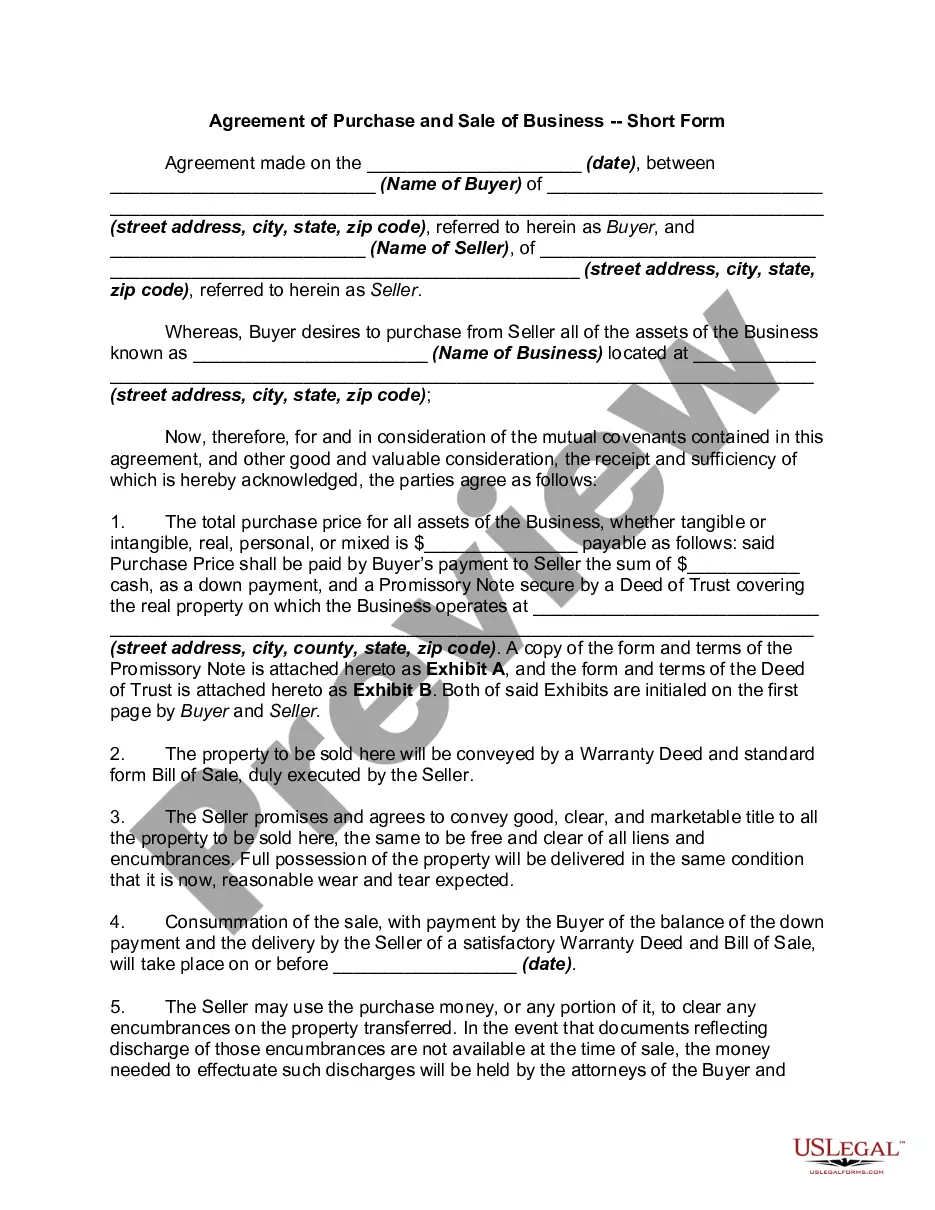

Master Sales Agreement With Seller Financing In Wake

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The buyer receives the property title after fulfilling the agreed terms. If the buyer defaults, the seller can repossess the property, as outlined in the finance agreement. This method benefits both parties by providing flexible terms and potentially faster transactions.

Your lender holds a lien on the property, not a mortgage, meaning they do not hold the deed itself. Understanding the difference between title and deed is crucial. Different types of deeds can affect your ownership rights.

And hit add or add remove. And you're going to get to another screen that on the left has all yourMoreAnd hit add or add remove. And you're going to get to another screen that on the left has all your search criteria in the mls. And you'll just type in propose. And you'll see proposed financing.

Most seller notes are characterized by a maturity term of around 3 to 7 years, with an interest rate ranging from 6% to 10%. Because of the fact that seller notes are unsecured debt instruments, the interest rate tends to be higher to reflect the greater risk.

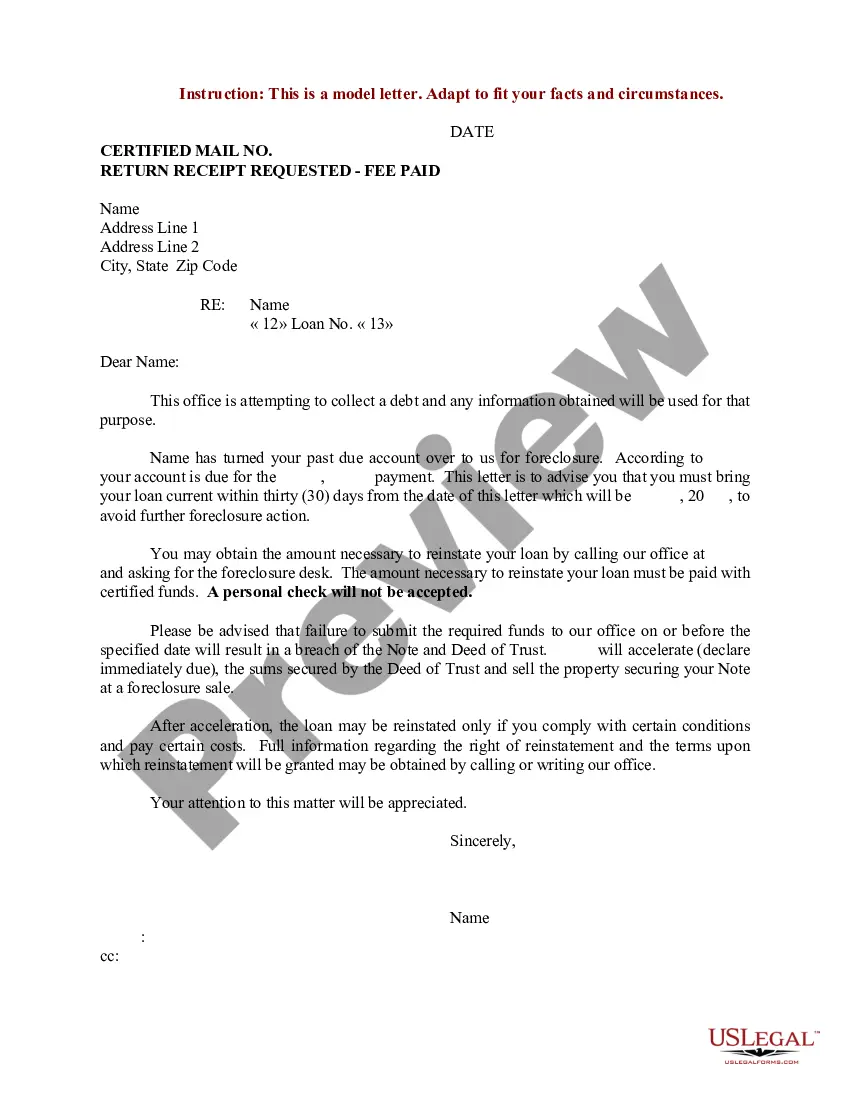

SELLER FINANCING UNDER DODD-FRANK This new rule also applies to sellers of residential dwellings to consumers in which the seller provides financing to the consumer secured by a mortgage on the dwelling, unless the seller is entitled to certain exclusions.

Given the potential speed and flexibility of the arrangement, seller financing may also help the owner attract more prospective buyers for their property. Sellers may skip making the kinds of repairs typically advised when preparing a property for sale.

I've seen seller finance deals at 5-6% - which is attracting buyers who would normally get approved for a traditional mortgage. The down is usually 20-30% - and some are even extending terms over 15 or even 30 years.

Negotiation: The negotiation process is where both parties can find common ground. Buyers should aim to secure an interest rate that is as low as possible, while sellers should seek a rate that ensures a reasonable return on their investment. A fair compromise often lies somewhere in between.